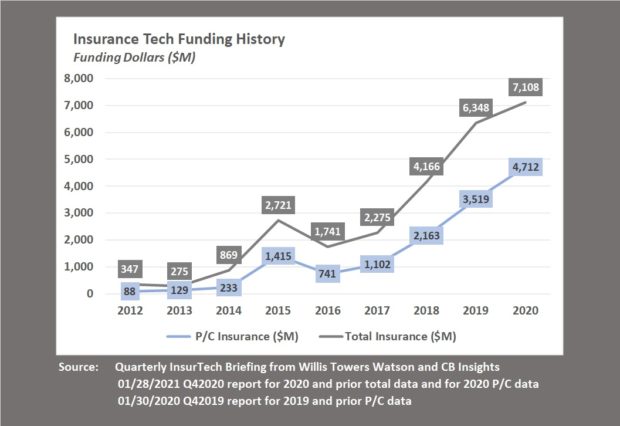

After a slow start in 2020, InsurTech funding reached a record level of $7.1 billion for the year, with $4.7 billion earmarked for property/casualty startups, according to a quarterly tracker of InsurTech funding volume.

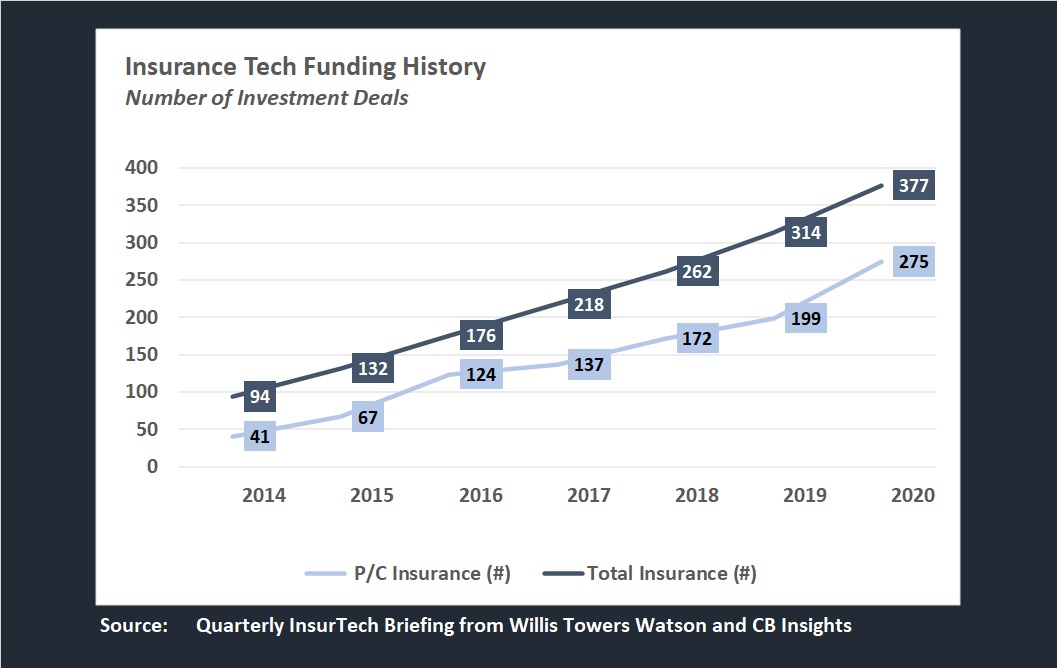

According to the latest Quarterly InsurTech Briefing from Willis Towers Watson and CB Insights, the year’s 377 deal count also marked a record level, with the third- and fourth-quarter dollar volumes and deal counts more than making up for depressed levels of funding in the first and second quarters last year.

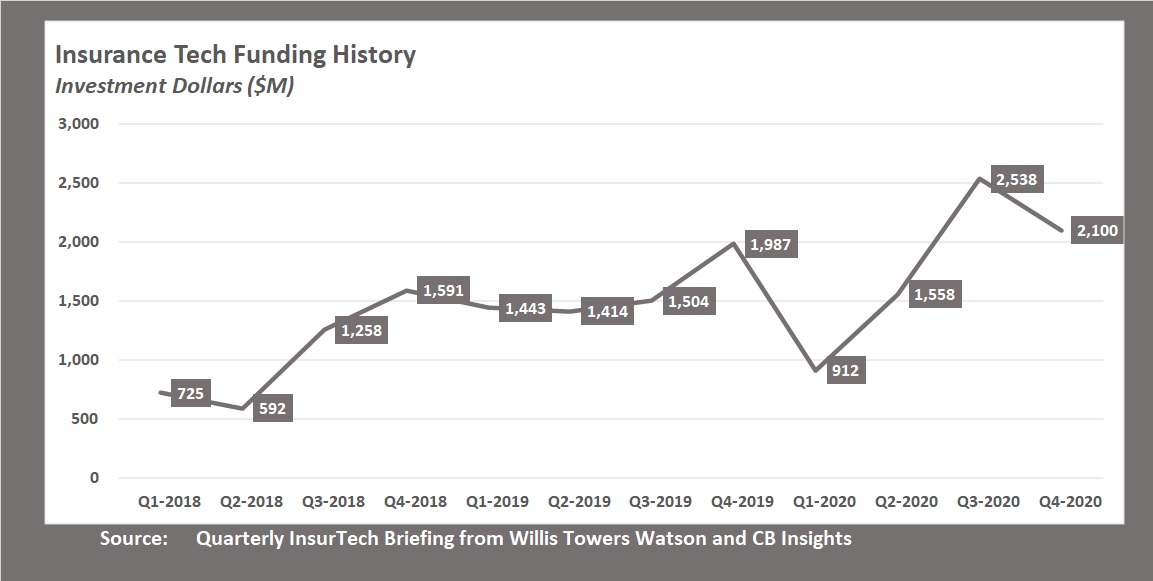

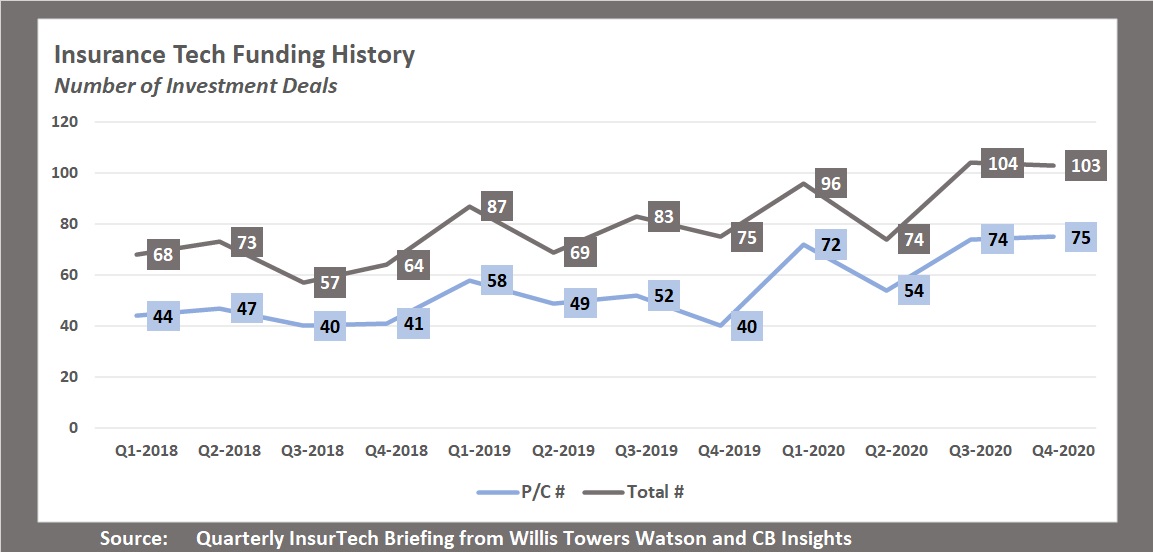

InsurTechs raised $2.5 billion across 104 deals in the third quarter and $2.1 billion across 103 deals in the fourth quarter. In contrast, the sector saw less than $1 billion of funding in the first quarter.

In fact, the $912 million that was invested in InsurTechs during first-quarter 2020, was the lowest quarterly level since second-quarter 2018 and roughly half of what had been invested the prior quarter (fourth-quarter 2019). “This bucked a trend of big raises throughout all of 2019,” Dr. Andrew Johnston, global head of InsurTech at Willis Re, wrote in the forward to the report, noting that the drop in first-quarter activity was most pronounced at the higher investment rounds—where corporate venture capital firms typically invest—suggesting that insurers and reinsurers were preoccupied with COVID-19 early last year.

“While COVID-19 has created a platform for InsurTechs to shine, it has also created a temporary environment that has made access to funding difficult. COVID-19 has made the ability to run in-person proof of concepts difficult. And perhaps most important, COVID-19 has made the issue of vendor-client trust a very problematic hurdle to overcome,” he wrote.

Still, Johnston added: “While our industry is facing extreme issues relating to COVID-19, we also have an unprecedented level of access to technology and technologists who can help it prevail during these times of instability. Many InsurTechs probably feel vindicated that the insurance industry has been forced to realize the value of technology. The issue for InsurTechs now is to survive months, possibly years, of market uncertainty.”

Providing funding highlights for the third-quarter’s bounce back, the report noted that six megadeals accounted for 70 percent of the total dollar volume raised in that quarter.

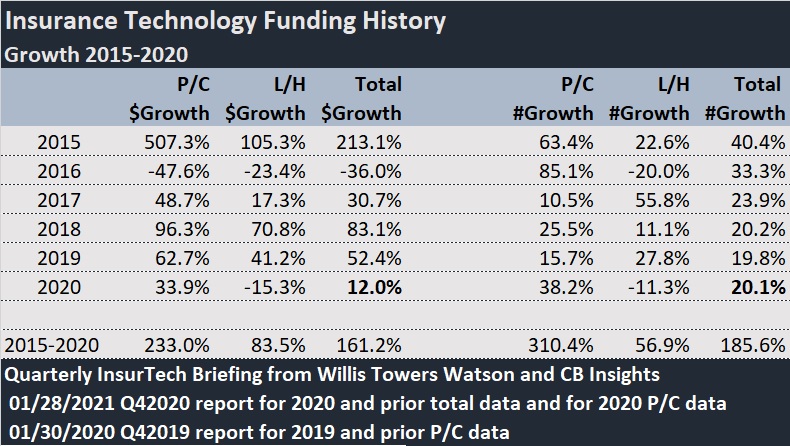

In the fourth quarter, property/casualty InsurTechs continued to outpace life/health InsurTechs in both dollars of funding and deal counts, attracting 67 percent of the $2.1 billion total and 73 percent of the 103 deals.

Home InsurTechs, in particular, continued to attract investment, CB Insights noted in an analysis of the numbers on its website. Hippo, a direct-to-consumer home insurance players, raised the quarter’s largest round—a $350M Series F, and Paris-based Luko, which also provides sensor-based D2C home insurance, raised a sizable $60M Series B.

Further analyzing funding further by stage of investment, the report notes:

- The share of early-stage deals declined to 47 percent compared with 57 percent in third-quarter 2020.

- Mid-stage deals saw a significant uptick, with 29 percent of deals at the Series B or C stage. This was a notable contrast to the scarcity of relative investment activity in these rounds, particularly Series C, noted in the third-quarter 2020 report from WIllis Towers Watson and CB Insights.

- Hippo, Unqork, Waterdrop, Oscar Health, Bind Benefits and Newfront Insurance—all later-stage InsurTechs–each received in excess of the $100-million-dollar “mega-round” funding mark, creating six mega-rounds for the quarter. Added together, these six rounds combined totaled $1.1 billion in funding.

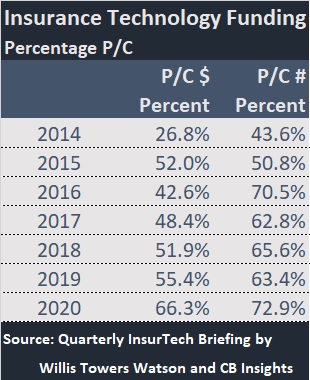

Willis Towers Watson and CB Insights note that P/C deals represented the majority of investment—accounting for 73 percent of the total deal count and 67 percent of the total funding.

While the percentage of deals and dollars was higher in 2020 than any prior year, the report noted that over the last two quarters, life/health InsurTechs represented 50 percent of later-stage mega-round ($100 million-plus) deals, the report said.

Charts below, compiled by Carrier Management using data from the fourth-quarter 2020 Quarterly Briefing report, and historical data for P/C and L/H from the fourth-quarter 2019 Quarterly Briefing report, show the growth in deals and deal values since 2015 and the percentage in the P/C sector.

More to Come

Looking ahead to 2021, Johnston said Willis Towers Watson professionals anticipate there will be another cluster of IPOs from firms looking to make the most of the public market’s appetite to invest in new technology firms, following several IPOs in 2020. “Though some may be overvalued, others may yet deliver on their promise,” he said on a video introduction to the report on the Willis Towers Watson website.

The report noted the high values of 2020’s IPOs, putting Lemonade’s entry valuation at more than 40-times its book value and stating that Metromile is set to float publicly at 120-times its book value.

Johnston said more big industry partnerships are anticipated on the horizon as well, also predicting that “big tech firms will continue to see our industry as an important opportunity.” AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act

As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?