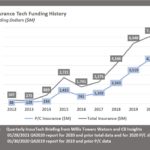

While the aggregate InsurTech funding level for the first-half of 2021 soared past the amount raised for InsurTech businesses for the entire year 2020, InsurTechs continued to quietly shut their doors with much less fanfare.

When Willis Towers Watson reported a surge in InsurTech funding to $7.4 billion in the first-half of 2021 last week, just one paragraph of the firm’s Quarter InsurTech Briefing referred to the fact that more than 450 InsurTechs have failed over the past decade. But it’s an important update, the study’s author, Andrew Johnston told Carrier Management in an interview two weeks before the report’s release, noting that he’s been collecting failure data for the last 14 months.