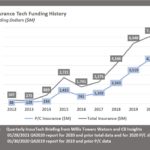

InsurTech funding saw the largest number of deals and the highest amount of funding since data recording into InsurTech began, with $2.5 billion raised by InsurTech firms across 104 deals during the third quarter, according to a report published by Willis Towers Watson.

This represents an increase of 63 percent in funding and a 41 percent increase in deal count–over figures reported in the second quarter, said WTW’s latest Quarterly InsurTech Briefing.

Q3 deals included two $500 million rounds, but the mid-tier funding gap–for firms seeking investments in the $20 million to $50 million range–has widened, according to the report.

Six mega-rounds of $100 million or more accounted for more than two-thirds of total funding, including Bright Health, Ki, Next Insurance, Waterdrop, Hippo, and PolicyBazaar. Early-stage deal share grew to 57 percent, up 15 points to pre-COVID-19 levels, bolstered specifically by P&C start-ups, said the report.

More than half of InsurTechs with a Q3 Series A round were raising capital for the first time and raised on average $10.9 million. However, InsurTech companies seeking mid-tier Series B and C investments saw deal share shrink by almost 9 percentage points, said the WTW report. Non-industry investors, such as venture capital and private equity, predominated in the smaller rounds, while re/insurers were focused in the larger end.

“With everyone working from home, never has the true value of technology been more real and manifest in our industry. But most re/insurers are looking either to accelerate, conclude, or temporarily slow down their ancillary technological endeavors and focus instead on ensuring their core business functions operate efficiently in the new digital, remote environment,” commented Dr. Andrew Johnston, global head of InsurTech at Willis Re.

“Consequently, their appetite to support well-established InsurTechs is much greater than for those who still have things to prove. That means the lifeblood of budding InsurTechs who rely on Series B and Series C rounds to scale up has, relatively speaking, disappeared.”

P&C sector investments predominated, but the share of life/health (L&H) sector investments rose, up 3 points in Q3 2020 to 30 percent. This was driven by a disproportionate amount of L&H funding in the mega-rounds receiving true “growth” capital, with L&H accounting for three of the six deals, and 49 percent of total Q3 mega-round funding.

Source: Willis Towers Watson

*This story ran previously in our sister publication Insurance Journal.

AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry