Global insurer QBE Group is not building a specialty book in North America by sweeping up business shed by some of its big commercial lines competitors in the region, QBE’s leader said Wednesday.

Instead, QBE North America is “being careful” as it continues to build out specialty according to a prior plan, said QBE Group Chief Executive Officer John Neal.

“We have not jumped on AIG’s or Zurich’s decisions to correct their books of business. Our strategy for the specialty lines business is completely unchanged from what it was three years ago,” he said. “We had a trajectory where we felt we could build a $1 billion specialty business over five years, and that’s continuing to be the case.”

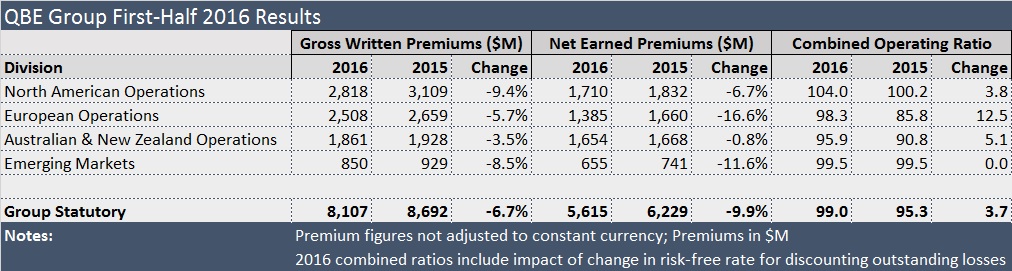

The comment came at the end of a half-year 2016 conference with analysts, in response to a question about growth targets around the world. For the first half, QBE Group’s global gross written premiums of $8.1 billion were essentially flat on a constant currency basis, and bottom-line net profit sank more than 40 percent to $265 million. In spite of those results, Neal and Group CFO Pat Regan revealed throughout the conference that strategic plans set out prior to 2016, as well as key financial targets delivered to the market in May, all contemplated the headwinds of reduced insurance pricing and low interest rates that impacted the first-half numbers. That means much of business is moving according to plan, they said.

Indeed, Neal affirmed a full-year combined ratio target of 94-95 for the group. During the first six months of 2016, the reported combined ratio was 99, but the first-half 2016 result included 5 points attributable to the change in the risk-free interest rate used to discount outstanding claims (a $283 million charge in dollar terms). Excluding that impact, the first-half result hit the 94 combined ratio target.

The executives noted that expense savings are on track as well, with $124 million of $150 million of targeted savings for 2016 already achieved.

As Neal and Regan reviewed the first-half financial ratios and results in detail, they said that only full-year premium targets were in need of a slight downward adjustment from a prior plan—now contemplating full-year gross written premiums dropping 5-7 percent below last year to a range of $13.7-$14.1 billion for the group—including impacts of continued tough market conditions and foreign exchange. (A prior estimate released in May had each end of the range roughly $0.5 billion higher—at $14.2-14.6 billion).

Australia Market a Spoiler

As for loss ratios, with QBE releasing reserves related to prior accident years for the fourth consecutive half-year period—this time around in the amount of $218 million—and with reinsurance protecting the group from catastrophe loss issues that dented results of competitors, Neal flagged only one region’s results as problematic: the home market of Australia and New Zealand.

Noting that QBE Group’s attritional (non-cat) loss ratio deteriorated roughly 3 points from first-half 2015 (excluding U.S. Mortgage and Lender Services business sold in 2015 and improving U.S. multiperil crop business from the comparison), Neal attributed 80 percent of the deterioration to trends in two books of Australia and New Zealand business: increased accident frequency and average claims costs for New South Wales compulsory third-party (auto) business, and premium pricing pressure and higher-than-normal claims inflation on the short-tail portfolios. (The long-tail portfolio performed well, making the overall Australia/New Zealand region combined ratio result show up comparatively better than other regions on the chart above.)

“The movement in our attritional claims ratio…is both disappointing and unacceptable,” he said, noting, however, that the situation is correctible and that fixes are already underway—with a series of rate increases and government reforms expected to repair the CTP book. “A combination of premium increases, tightened terms and conditions, and improved risk selection will drive the remediation required on Australian short-tail lines,” he said.

In addition to these decisive actions, QBE announced that Regan will take responsibility for the Australian and New Zealand business while the group searches for a permanent CEO for the division to replace Tim Plant, who will be leaving QBE effective immediately.

North America on Track

Photographer: Ian Waldie/Bloomberg

Noting improvements in reinsurance and standard lines areas of the North America operations as well, Neal said, “We now have a recognizable commercial and specialty business in North America, established regionally and with a solid suite of specialty and standard lines products.”

Expanding on recently added specialty lines, “we are launching an E&S business to complement our admitted capability, as well as broadening our product set in the personal lines area,” he added.

During the first half, North America specialty lines gross written premiums jumped up 51 percent, even as the level of gross written premium fell 9 percent for the North America operations overall. The 9 percent decline largely reflected the sale of mortgage and lender service business (completed on Oct. 1, 2015). Excluding the impact of M&LS business, the half-on-half drop was only 1 percent.

Neal said he was encouraged by trends in the North America claims ratio, with the shift to a specialty book moving the ratio up within reasonable bounds. As was the case for the group overall, the claims and combined ratios for North America were impacted by lower risk-free rates used to discount claims liabilities (3.5 points or $60 million). In contrast to the rest of the world, North America also had a small prior-year reserve boost—$34 million added primarily for commercial auto classes.

Commercial auto has “been a bit of a thorn in the side of the whole industry,” said Regan during the earnings update, referring to increased numbers of trucks on the road as a driver of frequency and new trucks and distracted driving as possible contributors to severity trends showing up in the claims triangles of all commercial auto insurers. Neal also noted that the commercial auto book in North America is only a $200 million book today—half the size it was a few years back.

No Market Respite in Sight

While North America and some other regions around the globe experienced weather losses, “the structure of our reinsurance has quite literally weathered us from the spate activity recorded by our global peers in the second quarter,” Neal said at one point during the conference.

An analyst, noting the excess frequency of large losses globally that have impacted other insurers and the strategic issues that Zurich and other carriers are trying to tackle, asked if either trend added up to an impending change in market conditions. “Can you give us some sense of when there might be a market turn in terms of market pricing?” the analyst asked.

Neal, referring to outlooks and targets presented by QBE executives during an Investor Update in May, recalled, “We said our forward plans assumed a backdrop that wouldn’t help us—assuming no free kick from interest rates [or] price. Both of those remarks turned out to be more prophetic than we thought,” he said. In the months since, interest rates have gone down and a pricing-turn catalyst is nowhere in sight, he noted.

“I can’t see any obvious factor that will move price in the short term,” he said.

“My sense is you’re going in the right direction. It won’t be a major cat. I think there is enough capital in the world in insurance to reload after a big cat,” he said.

“It’s going to be a spate of attritional cat activity or unexpected loss,” he said, suggesting that “if we keep seeing terrorist-related losses that we’re seeing, maybe that might be something that would trigger price.”

“But no, I can’t see an obvious factor that will move price quickly,” he concluded.

Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums