Telematics has been on personal insurers’ radar for many years, and it has recently reached a tipping point. Nowadays, it is recognized as a necessary capability for the future success of any auto insurer in the U.S. market.

Executive Summary

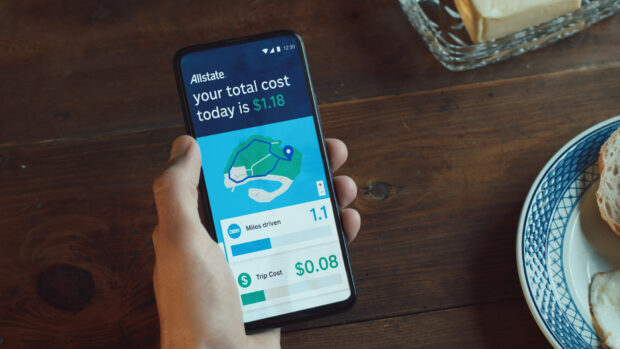

Allstate's David MacInnis and the IoT Insurance Observatory's Matteo Carbone wrote an article for the third-most popular feature published on Carrier Management last year—The Journey to Build the Auto Insurer of the Future—detailing features like active customer engagement, service offerings and incentives to promote safer driving that are built into Allstate's Drivewise and Milewise telematics programs. Still, some insurance professionals are skeptical that telematics is gaining traction. Here, MacInnis and Carbone follow up with hard evidence on take-up rates and double down on their efforts to explain the benefits of telematics for society and for insurers as well. Photos from AllstateLast year we analyzed Allstate’s journey toward developing this capability in our article “The Journey to Build the Auto Insurer of the Future.” That piece analyzed how Allstate has continued for a decade to sharpen its mastery of telematics data by innovating across multiple use cases. We explored Allstate usage of telematics data for:

Changing behaviors by identifying behaviors that are predictive of crashes and the ability to explain desired behavior changes to the customer. Generating positive externalities to the society due to the promotion of safer driving behaviors. Offering positive and engaging experiences to the policyholders. Providing useful services, such as crash detection, for the policyholders. Better matching rate to risks through continuous underwriting. Addressing changing risks.These contents have been extremely well received and have generated an interesting debate around the necessary capabilities for auto insurers of the future.

However, the sector must deliver results each quarter. It is not unusual to hear questions about the real impact generated by the usage of telematics data or reference to “not-yet-so-relevant” levels of UBI adoption in discussions between insurance executives. This is one of the reasons that have motivated us to write this second essay. Our direct experience provides some answers to these concerns, and we want to reinforce further our call to action for a better and informed usage of telematics data in the insurance sector.