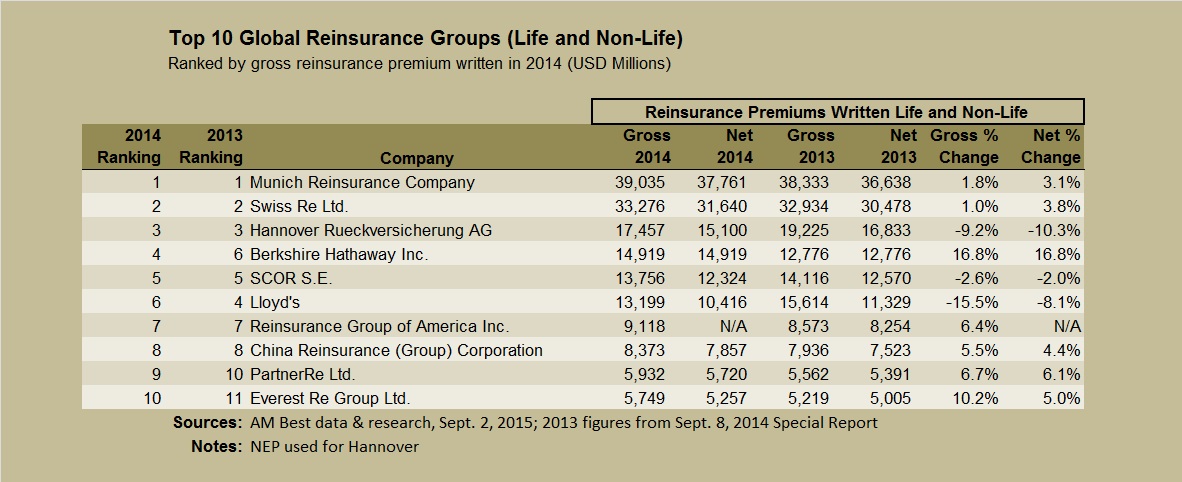

“The top 10 will probably continue to be the top 10” a decade from now, A.M. Best Vice President Robert DeRose predicted during a Sept. 9 webinar, referring to the top 10 global reinsurers (non-life and life) based on gross reinsurance premiums. DeRose made the long-range forecast after he and other analysts discussed how the landscape will shake out as a result of the recent wave of merger and acquisition activity and the impact of alternative capital.

Addressing the second trend, DeRose said, “There will be the traditional aspect of the business always,” suggesting that relationships and unique products cement a place for traditional reinsurers. But “reinsurers also will have greater transformer/capital markets operations—being able to access capital and match risk to the capital,” he added. And here, as they broaden their business to embrace these nontraditional areas, having scale in terms of product and in terms of geographic [reach] are going to be key. The capital markets are going to want to play with the big players because they are going to see that that’s where the opportunity to access the business truly lies,” DeRose said.

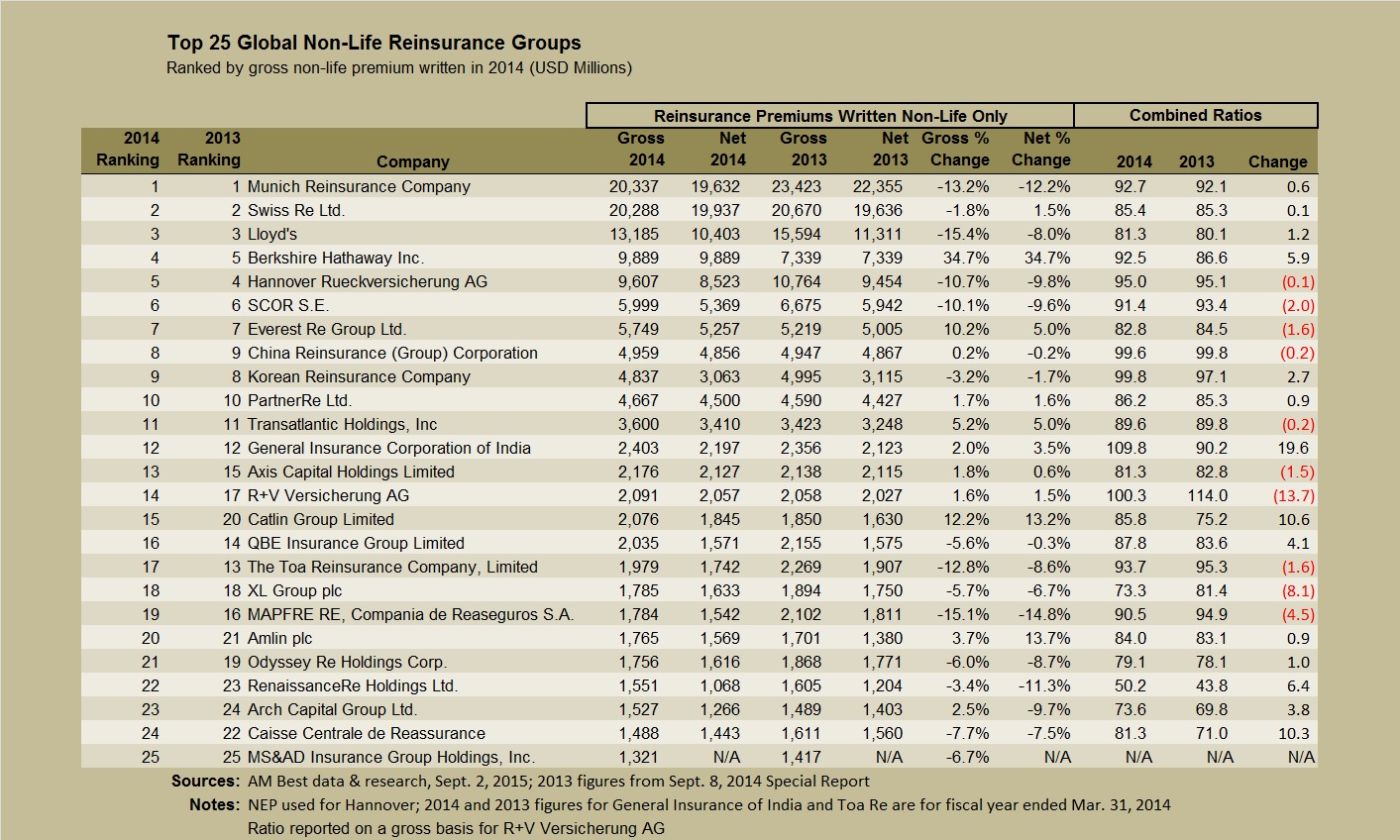

Extracting just the non-life gross premiums for 2014 and comparing those to 2013 non-life gross premiums presented in a prior A.M. Best report (published Sept. 8, 2014) reveals Catlin’s repositioning from a 20th place ranking for the prior year to 15th place, with a 12.2 percent jump in gross written reinsurance premiums to over $2.1 billion.

While the combination with XL did not figure into the rankings because they are based on 2014 premiums and the deal closed in May 2015, adding premiums for 18th-ranked XL and Catlin together would land XL Catlin in 11th place with $3.9 billion in gross non-life reinsurance premiums—just ahead of Transatlantic Holdings.

Similarly, the merger of Endurance Specialty Holdings and Montpelier Re Holdings, expected to close in the third quarter of this year, could propel Endurance into the top 20 non-life reinsurers. Based on 2014 gross non-life reinsurance premiums of $1.9 billion, the Endurance-Montpelier combination would rank ahead of Toa Reinsurance Co. for 2014.

The FX Effect

Toa Re was one of a half-dozen companies among the top 25 non-life reinsurers to record a double-digit drop in gross non-life premiums in 2014 based on A.M. Best’s numbers. But as A.M. Best explains in the report, some of the other declines—for non-U.S. reinsurers—are magnified by currency translations.

For the purpose of the rankings, A.M. Best used the foreign exchange rate that coincided with the date of the financial statements (usually Dec. 31 for 2014 and 2013). The comparative analysis of one year to the next is therefore complicated by the significant devaluation of global currencies against the U.S. dollar.

For example, although premiums are shown dropping 15.5 percent in the table above, the drop is only about 10 percent when both 2014 and 2013 figures are stated in the original currency, Best notes.

SCOR SE, which shows a 10.1 percent decline in non-life premiums, actually grew 2.2 percent on the non-life side in the original currency.

In addition, Korean Reinsurance Co. dropped from No. 9 and No. 11 as a result of the foreign exchange effect. Premiums for Korean Re actually grew 1.3 percent in original currency from 2013 to 2014 rather than dropping 2.9 percent—the change indicated when premiums for both years are converted to U.S. dollars.

Among the top 10 reinsurers reporting double-digit jumps in reinsurance premiums were Berkshire Hathaway and Everest Re. The A.M. Best report attributes Berkshire Hathaway’s climb, in part, to a retroactive reinsurance contract that Berkshire’s National Indemnity sold to Liberty Mutual Co. in 2014 covering asbestos, environmental and workers compensation liabilities. For Everest, growth came largely from new business opportunities related to catastrophe-exposed risks and to new quota shares in the company’s international book, Best reports.

“Looking forward, the top 50 landscape will likely look somewhat different next year and for years to come as M&A is expected to continue given the challenges in the market of increased competition, higher commissions, lower prices and higher retentions,” the A.M. Best report concludes. “Aside from the top five to eight companies that are expected to remain intact for the most part due to their size, the rest will likely look very different over the next few years.

“The question is who will merge with the right partner and who will merge out of desperation. There will be winners and there will be sinners,” the report says.

Rising Pro Boxer Killed While Riding Bicycle in Bizarre Texas Crash

Rising Pro Boxer Killed While Riding Bicycle in Bizarre Texas Crash  This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis

This Year’s SCS Loss Totals Will Fall Below Average: KCC Analysis  Deep Dive: Understanding Data Center Perils

Deep Dive: Understanding Data Center Perils  Secondary Perils Responsible for Virtually All 2025 Nat-Cat Insured Losses in North America: Swiss Re

Secondary Perils Responsible for Virtually All 2025 Nat-Cat Insured Losses in North America: Swiss Re