Alternative investment managers are pouring unprecedented sums of money into the market for property cover, and reshaping a 180-year-old reinsurance model in the process.

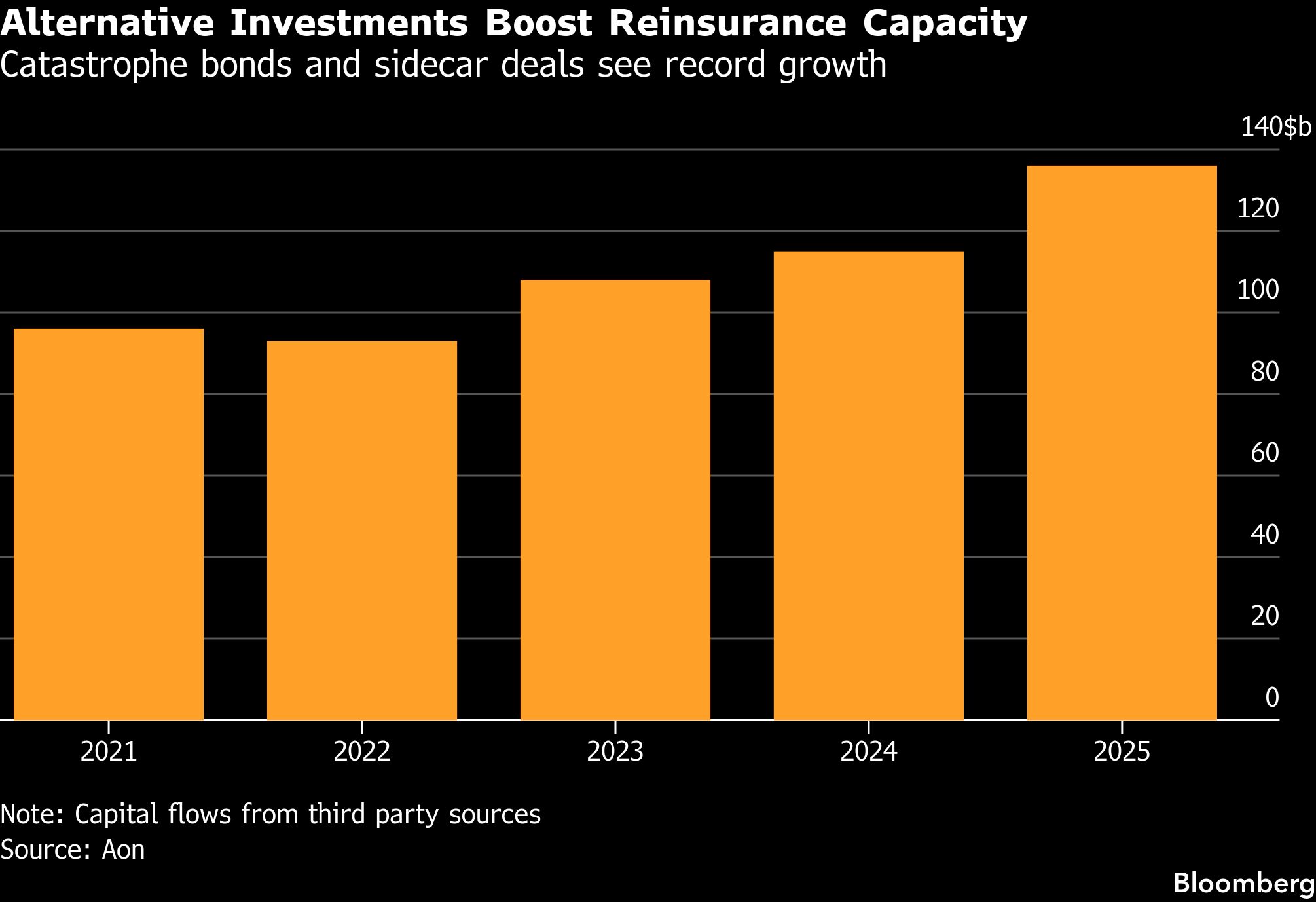

Allocations to catastrophe bonds and other insurance-linked securities popular among hedge funds and institutional investors rose 18% to reach a record $136 billion last year, according to data provided by broker Aon Plc. That rise in alternative capital and “its influence in the broader reinsurance market is growing because of the record growth in catastrophe bonds,” Aon told Bloomberg.

The shift promises to alter the face of a market whose basic role is to provide stable property cover during periods of sustained losses. It also raises questions as to whether reinsurers will gradually play a smaller role as the ultimate backstop for covering catastrophe risk.

Reinsurers may end up becoming more like risk managers, “shifting the risk to the capital markets which have trillions of dollars to invest,” Brian Schneider, senior director of insurance at Fitch Ratings, said in an interview. And if “more and more of this business gets shifted to the capital markets, then maybe the traditional companies become less and less relevant.”

Reinsurers covered just over 10% of total insured catastrophe losses in 2024, well below the historical average of 20%, according to S&P Global Ratings. The industry’s biggest firms have more than halved their exposure to insured disaster losses in recent years, S&P also said.

Reinsurers are themselves the driving force behind the shift. That’s as urbanization, higher inflation and climate change combine in ways that mean natural catastrophes are both more frequent and more devastating when they hit. The industry’s response has been to look for ways to offload risk to capital markets.

They mainly do this by issuing cat bonds, an asset class that saw “breathtaking” growth in issuance last year, according to John Seo, managing director and co-founder of Fermat Capital Management, the biggest hedge fund investor specialized in such securities. Speaking in a February interview, Seo said he thinks “the issuance surge we’re seeing is far from over.”

Reinsurers are also attracting record levels of private capital into so-called sidecars. Such vehicles give third-party investors access to premiums, in exchange for which they must accept a slice of the risk associated with natural disasters. It’s a market that’s nearly tripled in size since 2023, reaching as much as $18 billion today, with much of the growth coming from property catastrophe coverage, according to AM Best, a rating agency that tracks the insurance industry.

Germany’s Hannover Re recently set up a Bermuda-based insurance agent to create bespoke catastrophe-related portfolios for hedge funds, pensions and other professional money managers.

“As part of the overall ILS activities that we have, we felt this was the missing piece,” said Michael Eberhardt, chief executive of the new venture, Hannover Re Capital Partners. “It allows us to leverage our own underwriting expertise and partner with third-party capital investors.”

Fitch notes that investors in sidecars can face potentially bigger losses than holders of cat bonds, should a natural disaster result in a trigger event. That’s because sidecars tend to be exposed to losses from more common secondary perils such as hailstorms, wildfires and floods.

“There’s concern that maybe some naive capital is coming in,” and that “investors don’t really think they’re going to get hit by a lot of these secondary perils,” Schneider said.

Reinsurers, meanwhile, face an erosion of their pricing power as private capital moves into the market.

“Market conditions are now a little less favorable” as the supply of capital exceeds demand, said Ed Hochberg, head of global risk solutions at Guy Carpenter, a broker.

Twelve Securis, which invests in both cat bonds and private ILS, says that competing in today’s market comes with new uncertainties. “If hazards, exposures or correlations are poorly understood, the apparent premium may reflect mispriced or uncompensated risk,” it said in a recent report.

The influx of private capital is also impacting life and casualty reinsurance. Blackstone Inc.-backed funds last year agreed to back a roughly $1 billion reinsurance vehicle that will assume risk from F&G Annuities & Life’s annuity business. Blackstone also teamed up with The Fidelis Partnership on a new Lloyd’s of London syndicate launch, while Oaktree Capital Management and Germany’s Allianz SE launched a reinsurance syndicate at Lloyd’s.

The European Insurance and Occupational Pensions Authority, without naming individual firms, has struck a cautionary note. In a report published in February, it said that PE investors can have a short-term investment horizon, as well as a desire to unlock the value of their investment and an exit strategy that may be “misaligned with the undertaking’s long-term commitment to policyholders.”

And the Bank of England has warned that PE firms’ growing footprint in the insurance sector exacerbates the risk of “fire sales” that disrupt the functioning of financial markets.

Ultimately, says Fitch, the concern is that private credit can increasingly take control of “capital and investment decisions” instead of leaving it in the hands of traditional, risk-averse reinsurers.

Study Finds Long-Term Substance Use Among Workers Rising

Study Finds Long-Term Substance Use Among Workers Rising  Florida Conducting Annual Slow Down Campaign to Target Speeders

Florida Conducting Annual Slow Down Campaign to Target Speeders  NY AG Suing 3M, Other Chemical Companies Over PFAS Pollution

NY AG Suing 3M, Other Chemical Companies Over PFAS Pollution  California Bill to Let Insurers Use Driver Telematics Mulled by Legislature

California Bill to Let Insurers Use Driver Telematics Mulled by Legislature