The U.S. personal insurance sector is positioned for improving underwriting performance in 2024.

According to Fitch’s latest U.S. Personal Lines Market Update, the change is predicted amid signs that the previous surge in claims severity from higher inflation and supply chain shortages has subsided, combined with rapid written premium growth from significant rate increases.

Personal lines insurance is the largest U.S. P/C insurance market sector, representing over 51 percent of 2023 industry net written premiums (NWP). The latest report from Fitch Ratings found the U.S. personal lines insurance sector endured a third consecutive year of underwriting losses in 2023, with the sector statutory combined ratio (CR) improving to 107 from 110 in 2022.

Auto

The personal auto line has seen a volatile four years in the wake of a 2020 pandemic-related 24 percent decline in auto liability reported claims, which contributed to a CR of 92.5—the best personal auto results in at least 25 years. Those numbers rapidly shifted to a 112 segment CR in 2022.

Substantial rate increases and underwriting actions in 2023 led to a considerably better ratio of 105. Sustained pricing momentum in 2024 and tapering claims trends will lead to break-even or better results for the year, though the pace of recovery will vary between insurers.

For the personal auto liability lines, higher claims severity is evidenced by an increase of about 42 percent in the paid loss for a claim closed with payment from 2019 to 2023. Insurers are also responding to higher claims costs in reserving practices as the average loss and loss adjustment expense reserve held per outstanding claim has risen by 44 percent from 2019-2023 to over $23,000.

As a result, personal auto premium rates have seen double-digit percentage rises for nearly two years. Favorable pricing is anticipated to continue for the rest of the year. Still, momentum could drop when a return to underwriting profits emerges due to competitive forces and policyholder and regulator resistance to cost increases.

As a result, personal auto premium rates have seen double-digit percentage rises for nearly two years. Favorable pricing is anticipated to continue for the rest of the year. Still, momentum could drop when a return to underwriting profits emerges due to competitive forces and policyholder and regulator resistance to cost increases.

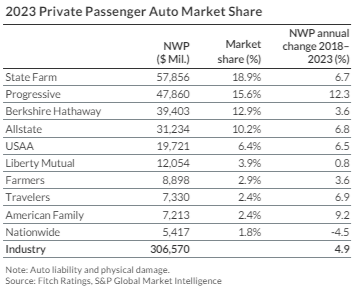

Underwriting performance varies widely among the 10 largest personal auto underwriters. Despite significantly weaker market conditions, the group’s four publicly held entities posted an average personal auto CR below 100 for 2019-2023. Progressive is the only one with an underwriting profit in each of the past five years, posting the best result with a 93 average CR for the period, followed by Berkshire (97), Travelers (98) and Allstate (100).

The six mutual and reciprocal insurers each posted underwriting losses in the past two years and a five-year average personal auto CR above 100. State Farm (110), Nationwide (106) and American Family (106) posted the highest CRs in the group for the period. While these companies continue to take significant underwriting actions, competitive forces and regulatory constraints may lead to reduced pricing momentum, inhibiting performance improvement.

Homeowners Results Deteriorate

The homeowners insurance segment has reported underwriting losses in six of the past seven years, including a poor 111 CR in 2023.

Despite no major hurricane-related losses, insured losses from inland convective storm events and rising building material and contract labor costs adversely affected results. Segment CR rose to 111 in 2023 from 104 a year earlier despite 11 percent growth in earned premium revenues. This result is the worst since an industry CR of 122 was reported in 2011.

Carriers in several states that have experienced heightened volatility in the homeowners line in recent years have emphasized aggregation management of property business. Over the past two years, large homeowners insurers have been increasingly curtailing the writing of new business and forgoing renewal of policyholders in more challenging states.

Homeowners pricing is rising significantly in most states. Segment information from quarterly filings of several publicly held insurers shows continued double-digit renewal rate increases over the past two years. The extent of pricing and underwriting activity is bound to improve segment results. However, a return to underwriting profits will hinge on annual catastrophe experience and further dampening loss severity patterns.

Homeowners pricing is rising significantly in most states. Segment information from quarterly filings of several publicly held insurers shows continued double-digit renewal rate increases over the past two years. The extent of pricing and underwriting activity is bound to improve segment results. However, a return to underwriting profits will hinge on annual catastrophe experience and further dampening loss severity patterns.

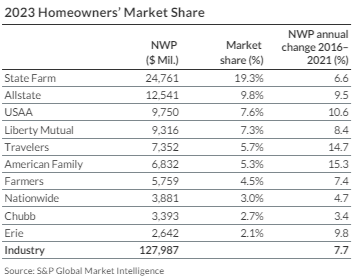

Market share in homeowners insurance is less concentrated than in personal auto, with the top 10 writers holding a combined 67 percent share in 2023. State Farm remains by far the largest homeowners writer, with a 19 percent share, followed by Allstate (10 percent) and USAA (8 percent). State Farm’s commanding lead has slightly narrowed in the past five years. Companies that have added market share over the period include Allstate, USAA, Travelers and American Family.

Similar to auto, the best performers are publicly held insurers. Despite a 105 homeowners CR in 2023, Allstate has the best five-year average segment CR at 96. Chubb and Travelers are the only other top 10 writers to post an average CR of below 100 for the period.

Among leading writers that are mutual or reciprocal insurers, Erie Insurance and Nationwide reported that the average CRs in homeowners from 2019-2023 was above 110. Market leader State Farm has experienced wide swings in homeowners results in recent years and has a five-year average CR of 102.

The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Supply Chain Insurance Is ‘Must-Have’ Cover During Geopolitical Tensions: GlobalData

Supply Chain Insurance Is ‘Must-Have’ Cover During Geopolitical Tensions: GlobalData  Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment