While soaring first-quarter underwriting profits and significant investment losses may not have surprised investors in Markel Corporation, continued favorable insurance market conditions aren’t quite lining up with what one executive would have predicted last year.

“Rate increases continue to gradually moderate but have held up better than we would’ve predicted a quarter or two ago,” Co-Chief Executive Officer Richie Whitt said during an earnings conference call yesterday.

“I believe that uncertainty around inflation, both economic and social, financial market volatility, including interest-rate increases, recession concerns and the Russian-Ukraine conflict have all played some role in supporting continued underwriting discipline in the market,” he said, providing market commentary after reviewing the specifics of Markel’s first-quarter insurance profits.

Earlier this year, speaking during a February conference call about 2021 results and looking ahead to 2022, Whitt told analysts, “There is no doubt that after three years, and in some cases four years, of rate increases, it’s going to be difficult to continue to average double-digit growth in rates across our portfolio like we did in 2021.”

On Wednesday, he said that while the rate of increases is decelerating to high single digits, Markel underwriters are seeing “a very gradual, gentle glide on the rates” that contrasts the more abrupt softening he would have predicted a few quarters ago.

While that view of the broader market was somewhat unexpected, both Whitt and co-CEO Tom Gayner suggested there was nothing surprising about Markel’s results in the first quarter for any of its three operating engines: insurance operations, investment operations and Markel Ventures (a unit that invests in businesses outside of the insurance industry).

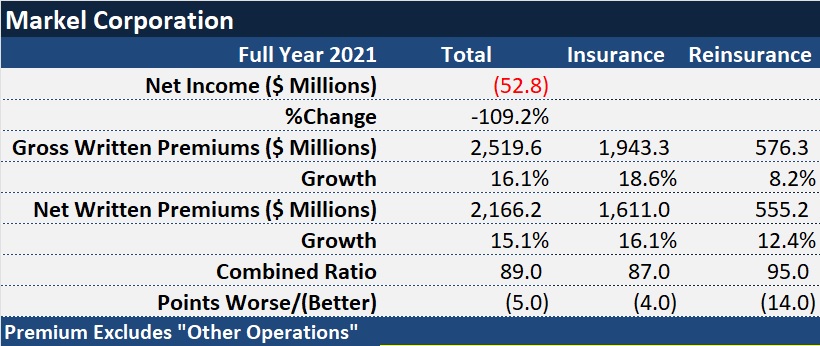

First-quarter pretax underwriting profits more than doubled to $197 million for Markel Corporation, and Markel Ventures pretax operating income held steady at roughly $50 million. But $358.4 million in investment losses (compared to $526.8 million of net investment gains in first-quarter 2021) put red ink on Markel’s bottom line.

The bottom-line net loss of $52.8 million for first-quarter 2022 compared to net income of $573.7 million for the same quarter last year.

Net investment losses in 2022 reflected a decrease in the fair value of Markel’s equity portfolio driven by unfavorable market value movements, the company said in a media statement.

“I think you as investors would agree that we are likely to regularly experience the most reported volatility within our investment engine as compared to the others,” Gayner said in his opening remarks to analysts and investors listening in on the conference call. “Given that reality, longer-term measurements matter way more than those of any given quarter,” he said, going on to detail favorable five-year movements in the size of Markel’s equity portfolio, levels of unrealized gains and the share price of Markel.

“While we necessarily report quarterly financial results as a publicly traded company, we think about and manage Markel over much longer time frames,” he said, noting that executive compensation, for one thing, is tied to five-year rolling results. “And in reality, we think in even longer time frames, such as decades and generations as we run this business,” he said.

Gayner preceded those remarks with an introduction to the forthcoming summaries of improved insurance results that would be delivered by Whitt and Chief Financial Officer Jeremy Noble—reporting on double-digit jumps in insurance and program services premiums, combined ratios drops related to the absence of catastrophe events and COVID losses, in addition to rate increases still tracking above inflation trends. (Programs services and fronting business is nearly 100 percent ceded.)

Said Gayner: “If I put myself in your shoes as an owner of Markel,…what I would expect over time [is that] there should be no surprises to you in our insurance operations when we report the results of any one quarter. You, as observers of the world, can know through regularly reported news whether major loss events like natural catastrophes, pandemics, wars, wildfires, tsunamis, hurricanes, earthquakes, or other big events took place or not,” he said, noting that thoughtful owners with a general awareness of news events could have predicted the excellent insurance engine results.

Reporting on the impacts of events on Markel’s insurance results, Noble said that the first-quarter 2022 combined ratio of 89 included the impact of $35.0 million of net losses and loss adjustment expenses related to the Russia-Ukraine conflict, which added 2 points to the combined ratio, as well as $12.3 million of ceded reinstatement premiums (additional reinsurance costs) attributed to the conflict. Markel’s 10-Q filing with the Securities and Exchange Commission reveals that the losses are primarily attributed to business written within the international insurance and reinsurance operations—war and terrorism coverages in the marine and energy product lines, as well as trade credit and surety product lines.

The 94 combined ratio for first-quarter 2021 included $64.3 million, or 4 combined ratio points, of net losses and loss adjustment expenses attributed to Winter Storm Uri, and $19 million, or 1 point, related to a change in Markel’s estimate of COVID losses last year.

In addition to the executives’ reports of results for insurance operations, Markel Ventures and investment activities, Whitt and Noble reported results of insurance-related activities that aren’t included in the premium and combined ratios figures summarized above: the ILS operations and program services operations.

In the Nephila insurance-linked securities operation, Markel disclosed two divestures in the quarter: the February sale of most of Markel’s controlling interest in a managing general agent operation known as Velocity for $181.3 million, and a March agreement to sell a controlling interest in another MGA, Volante, for $155 million.

“Both of these transactions unlock significant value from our Nephila acquisition in 2018 and also allow Nephila to devote full attention to the opportunities we see in the cat arena right now,” Whitt said.

During the Q&A, Whitt addressed questions about inflation and about Markel’s exposure to the Russia-Ukraine conflict.

Asked to comment on how much of current loss cost movement relates to economic inflation and how much relates to social inflation, Whitt told analysts that Markel cannot give specific insights from Markel data yet. “When we talk to our claims folks, they’re really not seeing a whole lot of claims inflation showing up in our numbers yet. However, we know of all the things that are going on out in the environment,” he said, referring to CPI inflation, litigation finance activity and the erosion of tort reform over the years. “We know that claims inflation is running higher than it historically has. I can’t give you a precise number, [and] we write…on the order of a hundred different lines of business. So, it would be different in each of those lines of business… But I still believe when you look at the rate increases that we’re still achieving,” in the high single digits, “there’s a margin that versus what claims inflation is running at right now.”

As to the question of whether Markel might see more exposure to the Russia-Ukraine war than the $35 million on the books, Whitt said, “To just be blunt, we have very little information at this point coming out the conflict.” With the war ongoing, “it’s not like you’re able to send adjusters in and see what the status is on the ground.” That said, Markel has “tried to make a good faith estimate of what could potentially be [its] exposure.”

“I would tell you that what we’ve put up is 100 percent IBNR at this point,” also thinking about what net retentions could be and how reinsurance kicks in, he said, describing the figure as Markel’s best estimate of what could happen.

“Obviously, the longer it goes on, both from a humanitarian standpoint and just economic damages standpoint, things get worse. But we do not write that much business in Ukraine or in Russia for that matter,” he said, characterizing the amount as “tiny in respects to our overall book of business.”

“When you start adding up policy limits, you can get to some big numbers, but we really don’t believe it is a material issue to Markel Corporation,” he said.

Executives on the Move at SiriusPoint, Canopius Group, Badger Mutual

Executives on the Move at SiriusPoint, Canopius Group, Badger Mutual  U.S. P/C Industry Books Best Result in a Decade, but Not All Lines Enjoy Success

U.S. P/C Industry Books Best Result in a Decade, but Not All Lines Enjoy Success  Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?  Default Speed Limit in Iowa Changes from 55 to 60MPH

Default Speed Limit in Iowa Changes from 55 to 60MPH