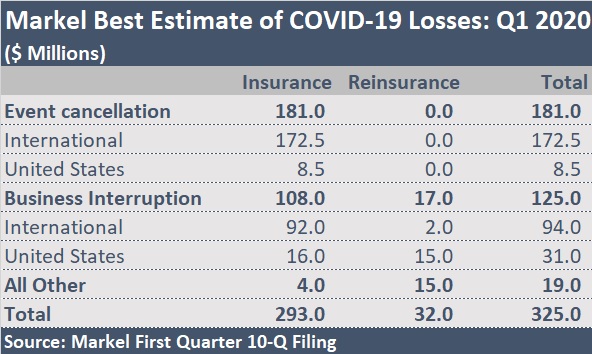

Diverging from strategies of some competitors, Markel Corp. established a big reserve for a chunk of its potential COVID-19 exposure for the entire year—putting up $325 million for direct potential losses.

The holding company for specialty insurance and reinsurance, ILS and venture businesses announced the insurance loss reserve Wednesday, mainly for incurred-but-not-reported claims related to COVID-19 on U.K. business interruption and worldwide event cancellation coverages. The underwriting charge and investment losses of $1.7 billion contributed to a bottom-line net loss of $1.4 billion for the quarter compared to $576 million of profit recorded for first-quarter 2019.

Going over the underwriting numbers during an earnings conference call, Markel Chief Financial Officer Jeremy Noble noted that the $325 million pretax reserve provision accounted for 24 points of the combined ratio, which came in at 118 for first-quarter 2020, up from a combined ratio of 95 for first-quarter 2019. Minus the COVID-19 loss provision, the combined ratios for both years would have been roughly the same.

Richie Whitt, co-CEO, described the COVID loss provision as Markel’s best estimate of “ultimate direct COVID-19 insurance losses.”

“That is our best estimate of business interruption losses and event cancellation losses through the remainder of the year,” Whitt said, when an analyst asked if he should expect Markel to record provisions of a similar magnitude in subsequent quarters. Whitt also noted, however, that many assumptions are “baked into that” best estimate. “For example, our event cancellation book goes from wedding cancellation to the Olympics and Wimbledon. It runs the gamut. We have tried to look out for the rest of the year in terms of what we think the potential exposure could be, and we’ve tried to book that in the first quarter,” he said.

Markel’s 10-Q filing with the Securities and Exchange Commission details the types of assumptions needed to arrive at best estimates for business interruption and event cancellation, and describes the inherent uncertainty that creates a potentially wide range of variability. These include: assumptions with respect to scope of coverage, which Markel views at broader under its international policies currently: assumptions about potential reinsurance recoveries; assumptions about the ability of insureds to mitigate losses (by holding virtual events rather than cancelling them, for example); assumptions about the expected duration of the disruption caused by the COVID-19 pandemic.

Commenting on duration of disruption, Markel has assumed it “will extend, in varying degrees, beyond the government directives currently in place and may impact certain covered events through the end of the year,” the 10-Q says, outlining a strategy that seems consistent with a historical approach to reserving described by Whitt during the earnings conference call.

“Inherent in our reserving practices is the desire to establish loss reserves that are more likely redundant than deficient,” he said. He added, however, that while the same tack applies for setting COVID-19 loss reserves, there’s no certainty that things will pan out that way. “There are simply too many unknowns at this time given the unprecedented and ongoing nature of the event,” he said.

Whitt went on to note that other insurers reporting first-quarter results have taken “a variety of approaches,” and that some are “planning to more fully reflect their COVID-19 exposures in the second quarter.”

While Whitt didn’t share any examples, during a recent earnings report, Chubb included a much smaller loss provision in its first-quarter earnings—$13 million—noting in a press release that “the company anticipates that this global catastrophe event will have a meaningful impact on revenue as well as net and core operating income in the second quarter and potentially future quarters as a result of an increase in insurance claims due to both the pandemic and recessionary economic conditions”

“With regards to claims, we expect an increase in claims relating to various property and casualty lines,” Chubb added in its 10-Q filing published yesterday.

For Markel, beyond variability in the assumptions used to determine its best estimate, Whitt distinguished between “direct” losses and “indirect” secondary losses to lines like directors and officer liability that will arise from disruption to the economy and financial markets over time.

“The thing that is not represented here in this [$325 million] number is the secondary losses or the indirect losses. That’s things like the potential for D&O around bankruptcies or E&O for brokers. That we’re going to be dealing with, just like after 2008, over the next several quarters,” he said, referring to the longer term emergence of such losses in the aftermath of the global financial crisis.

Belt and Suspenders

During the call, Whitt also provided details of some of the coverage assumptions related to business interruption claims based policy-level reviews of its U.S. and international books of business.

“Our U.S. property policies are not expected to respond to COVID-19-related business interruption losses, although we will be investigating each claim on its own merit,” he said, describing a “belt and suspenders” approach to underwriting the coverage.

“All of our U.S. property policies require a physical damage to occur before business interruption coverage is triggered,” he said, referring to this as the “belt” at several points during the call. “And almost all of those policies also include a communicable disease or virus exclusion,” he said, referring to “the suspenders” which further support the lack of coverage.

“That is not something new, by the way. Those exclusions have been going on those policies since 2007. So that’s over a decade that that has been in those policies,” he said, also asserting that “COVID-19 is not physical damage.”

The $16 million provision for business interruption losses in the U.S. relates to some policies that do have an affirmative coverage grant, often sublimited at $25 million, Whitt said, noting estimates are also included for another subset of U.S. policies with affirmative coverage and no sublimits, often in thin hospitality industry.

Explaining the $92 million provision for business interruption outside the U.S., Whitt said that while UK policies also require physical damage to trigger coverage, virus or exclusions have historically not been prevalent.

“We just simply expect, given the size of the economic damage, the political backdrop, the emotion involved [that] there’s going to be more litigation. And so we are preparing for that.”

Richie Whitt, Markel

“Where appropriate, we are taking steps to mitigate future exposure to pandemic losses by raising prices and adding policy terms and conditions, including additional exclusions,” he said.

He also noted that Markel is prepared for elevated litigation expenses related to business interruption claims in both the U.S. and abroad. Asked whether that meant the IBNR included a provision for such expenses, Whitt said, “It’s more implicit than explicit in terms of the numbers that we have put up.”

“Here’s the reality: The economics that are at stake, the economic damages that have been done by this situation are just so large [that] people have incentive to attempt to recover that even if their coverage was not granted. So, we just simply expect, given the size of the economic damage, the political backdrop, the emotion involved [that] there’s going to be more litigation. And so we are preparing for that. That is implicit to the numbers. As we go forward, it’ll probably be more explicit to the numbers.”

Whitt also said there isn’t much in the $325 million related to workers comp losses at this point. “I don’t know that we had any claims in yet as we were establishing the number, but we would expect claims as we go forward in workers comp.”

He noted that the nature of the event makes it difficult to quantify comp losses. “Usually, you have a hurricane or something and it’s over and you start adding up your exposure. But this one is ongoing. So there are people who will get sick, who have not gotten sick yet who will claim for workers comp.”

He did note, however, that Markel’s workers comp book is not weighted towards first responders, although other essential workers—involved in restaurants and retail—are included. “So we would expect to see claims,” he said, also stating that workers comp claims tend to rise with unemployment.

The Million Dollar Question

“In summary, while it is early and there are many unknowns, we believe the impact of COVID-19 to our insurance businesses is meaningful but also are manageable,” Whitt said, wrapping up his opening remarks by noting Markel’s diverse insurance business portfolio, solid liquidity and capital position.

During the call, co-CEO Tom Gaynor discussed investment losses and changes in Markel’s equity security holdings. According to Gaynor, at the start of the year, equity securities represented about 69 percent of equity capital, but by the end of the quarter, that fell to 58 percent “from a combination of modest sales as well as the overall market decline.”

During the quarter of 2020, the value of overall investment portfolio declined 7 percent while the equity portfolio declined 22.4 percent—the biggest quarterly decline since 2008-09.

While investment losses pulled overall operating revenues down, insurance premiums rose during the quarter. Gross written premiums were $1.9 billion, 13 percent higher than the $1.7 billion recorded in first-quarter 2019, with the insurance segment driving the increase. Insurance gross written premiums grew 19 percent to $1.4 billion, while reinsurance premiums were flat at $513 million.

What will the top-line look like going forward? Will positive rate momentum and narrower underwriting appetites in the admitted market outweigh the impacts of economic contraction to the benefit of E&S insurers like Markel?

“That’s the million-dollar question,” said Whitt, noting that Markel did indeed see E&S business pick up in April, perhaps because of changing appetites resulting from all the disruption. “We’ve got certain areas of our book where rates are up substantially and our writings are up substantially. In April, that did offset the decreases we saw in small business and places that you would expect to be hit hard by COVID-19.

“I’ve got to believe we haven’t seen all of the impact from COVID-19 yet,” however, he added.

“On the reinsurance side, it’s a hard market. Appetite is down, demand is up, and you’re going to see more people looking for coverage and pricing going up accordingly,” he asserted.

Another analyst expressed similar hopes related to the ILS market later in the call, suggesting that pensions funds unable to achieve desired yields given the level of Treasury bond rates and stock market volatility would turn to insurance-linked securities.

“That’s our view exactly,” Whitt said. “We recognize in the short-to-medium term, everything about the situation is negative on so many levels. But this just again proves why the ILS investment is valuable: It has very, very low correlation to the rest of the market,” he said.

Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America

Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America