Severe convective storms (SCS) have become the costliest insured peril of the 21st century, according to an Aon report published in January.

This phenomenon is reshaping the property/casualty insurance landscape. And one reinsurance provider is taking an innovative, parametric approach aimed primarily at protecting insurance companies’ earnings and surpluses.

As insurers grow into new exposure footprints, Mike Anderson, chief executive officer of Demex, said that some are realizing they haven’t properly considered attritional SCS risk, leading them to also realize they haven’t assessed their data in a way that helps them make better growth decisions.

“Whether you’re a big national [insurer] with a data science team or a small Midwest Mutual, it’s a complicated problem if you don’t know what you’re looking for,” he said. Now, he said, insurers are “becoming aware of the fact that this is having a huge impact on their balance sheet and that there’s probably more volatility in the death by a thousand cuts than they originally intuited.”

Demex sells secondary weather peril reinsurance. Launched in 2023, the risk analytics and intelligence company offers a parametric SCS product that it says is the “first modeled-loss reinsurance solution for non-catastrophic weather losses.”

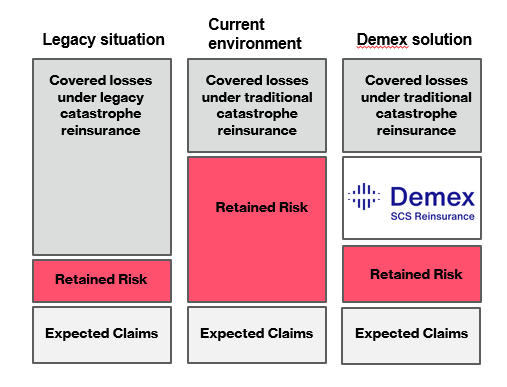

![]() Unlike other parametric insurance solutions that pay out when certain recordable weather conditions are met, Demex’s SCS reinsurance coverage triggers when the model loss accumulation reaches the threshold agreed in the policy. Anderson explained that Demex policies recover once the modeled loss threshold/attach point is breached.

Unlike other parametric insurance solutions that pay out when certain recordable weather conditions are met, Demex’s SCS reinsurance coverage triggers when the model loss accumulation reaches the threshold agreed in the policy. Anderson explained that Demex policies recover once the modeled loss threshold/attach point is breached.

The product settles quarterly, he said, and for avoidance of doubt, if the modeled loss threshold is exceeded as of March 31, for example, the amount over the attach point will be paid to the insurer within 45 days of the end of the quarter.

The company initially focused on offering coverage to Midwest mutuals to address their attritional SCS risk. Anderson explained that most of that region’s mutuals’ CAT treaties are built around SCS risk, not hurricane risk or other primary perils.

Demex recognized this and saw it as “the place where we can really fit,” Anderson said. “And we were able to look at and attack increased retentions and products where, on the aggregate side, they were priced so expensively that we figured we could make a dent.”

He said one reason that Demex’s pricing is typically “considerably more competitive” than indemnity aggregate products is because the modeled loss is built using actual ground-up claims data from the cedent. When correlated with the sophisticated use of detailed weather data, the model loss closely tracks actual indemnity loss, Anderson said.

Another reason is that the payouts are not impacted by the volatility of socio-economic costs, such as adjusting fees and reconstruction payments. An agreed-upon figure for these costs is built into the model, Anderson added.

Demex has since expanded the SCS product from just the Midwest to across North America, and it also created a cold weather product for one client this winter. (Anderson said that cold weather product will be released widely in 2026.)

When Anderson was appointed CEO in December, Insurance Journal reported that the move, alongside other C-suite changes, marked Demex’s transition from product innovation to commercial expansion, with “hundreds of millions of dollars in capacity committed” for the 2026 renewal season, and leading ratings agencies indicating they may give credit to cedents for the SCS reinsurance coverage.

“Typically, the way we like to build is we like to find a use case, and we like to focus our energy on building a bespoke solution around the use case,” Anderson explained. “And then, when we see the signal that the product is performing well and ready for general consumption, we release it.”

He continued: “That’s a lot of how we’re going to continue to grow. Because we know there’s other secondary peril and other weather-related reinsurance covers from a structuring side and a weather side that we can use this approach [with] to good effect.”

The company positions its SCS offering not as a replacement to indemnity products but instead as complementary to them. Anderson said Demex examines existing reinsurance structures and analyzes underwriting changes and cedent loss data, as well as growth areas and growth rates, to tailor its model to “basically fit a product perfectly to what your exposure footprint as a customer is going to be for the year in which you’re buying the policy.”

In total, the company has $37 billion of anonymized claims data from the various SCS models that Demex has built for its clients and prospects. Anderson said that because the data is sourced from ground-up claims, it encapsulates all SCS claims, rather than only those above a particular threshold—unlike common industry models, which Demex has calculated miss between 15 and 50 percent of SCS claims.

Anderson said Demex has found a way to use that data for individual customers, but company leaders have a sense that “there’s something more that we’re going to be able to do for the market with that $37 billion of anonymized claims,” he said. “It’s a lot of training data.”‘

Anderson shared that the company’s demand has increased in 2026. While many carriers, especially small mutual companies, are pocketing savings as the property reinsurance market softens, bigger companies and regional carriers are funneling those extra dollars into protecting against weather-related losses, he said.

“To see the adoption of our product in a soft market … as a CEO, you sit back and you say, ‘This is awesome,'” Anderson said. “This is a product for all times. Hard, soft [or] somewhere in between—this product has value for our customers, and that, as a startup CEO, is phenomenally exciting.”

Montgomery v. Caribe Increases Litigation Activity, Not Shipper Exposure

Montgomery v. Caribe Increases Litigation Activity, Not Shipper Exposure  NY Man Sentenced for Fencing Organized Crime Ring’s $4.4M Jewelry Theft

NY Man Sentenced for Fencing Organized Crime Ring’s $4.4M Jewelry Theft  AI Saves Time, But Most Companies Waste the Gain, Study Shows

AI Saves Time, But Most Companies Waste the Gain, Study Shows  The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention