In states such as Florida, Texas and Louisiana that have experienced numerous weather-related challenges and heavy claims activity in the last decade, newly established reciprocal insurance exchanges have stepped in to provide capacity.

The reciprocals have entered the picture as some established insurers have pulled back, aggressively raised rates or simply ceased writing certain risks.

Reciprocal insurance exchanges represent a unique and collaborative structure within the insurance industry whereby members are “subscribers” and take on a dual role as the insured and the insurer. Reciprocal exchanges historically have been present in segments such as personal auto, but escalating natural catastrophe losses and mounting reinsurance costs have led to an influx of reciprocals focused on the homeowners insurance market. Additionally, legislative reforms have facilitated an improvement in operating conditions, producing a conducive environment for reciprocals to operate in.

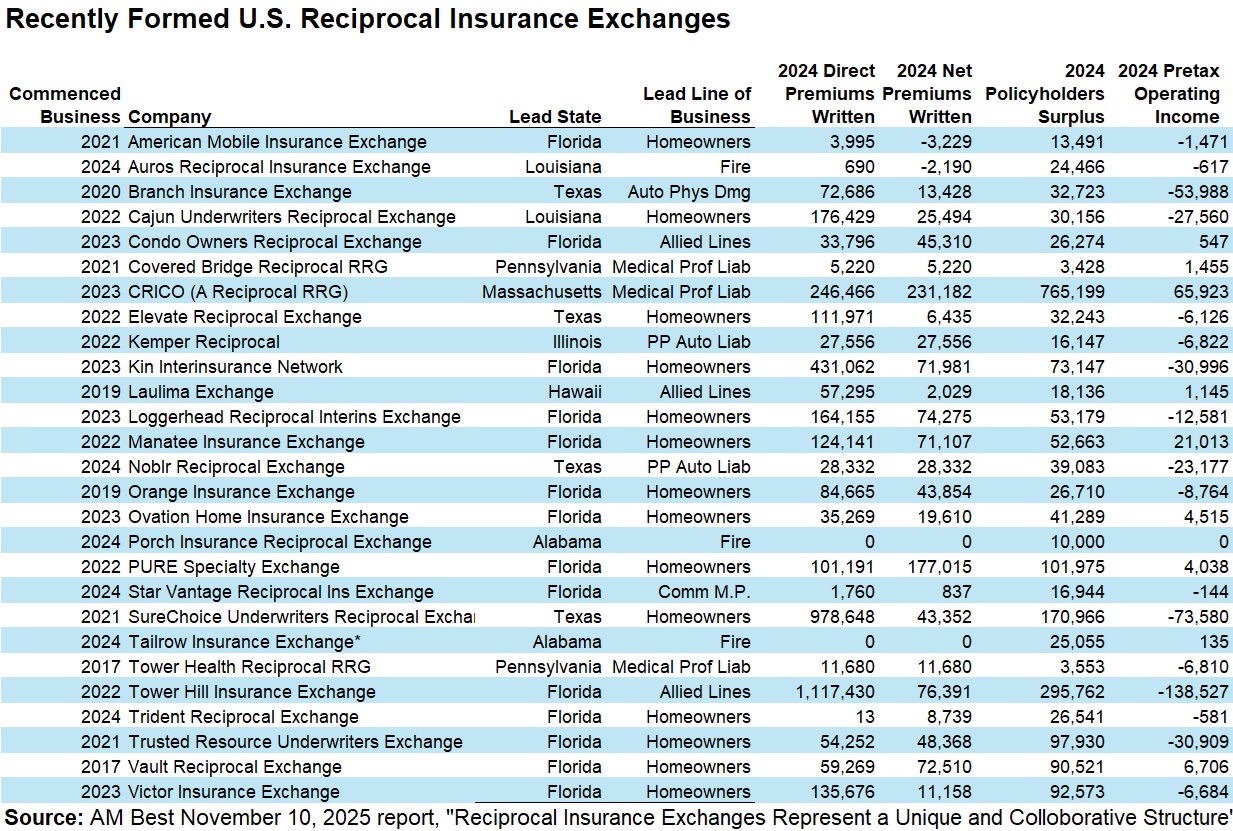

Of the 27 reciprocals formed in 2017-2024, 14 are in Florida, followed by four in Texas and two in Louisiana. From 2022 through 2024, the direct premium volume of these 27 reciprocals increased by 83 percent, and of the 14 companies mainly writing Florida business, the lead line of business for 11 of them is homeowners multiperil.

Editor’s Note: In a separate report, ALIRT Research counts 36 newly formed reciprocals from 2017 through the first nine months of 2025. ALIRT’s list does not include three RRGs, which are on AM Best’s list, but does include 10 other companies launched in late 2024 or 2025, two RIEs identified as having been converted from stock companies. ALIRT’s report, “Overview of Reciprocal Insurance Exchanges and Recent Market Trends.” Some other takeaways from the ALIRT report are included in the related Carrier Management article, “Why Reciprocal Insurance Exchanges Are Back in Fashion.”

Operating as technically unincorporated associations, these entities are distinguished by the critical function of an attorney-in-fact (AIF), a managing third party responsible for all operational aspects, including handling claims, underwriting new policies and managing investments. Members, whether individuals or businesses, collectively contribute premiums, which are used to cover operating expenses and claims payouts.

A key advantage of the reciprocal exchange model is the increased control subscribers exert over aspects like rates and strategy, directly aligning the interests of the insurer and the insured since they are the same party. The term “reciprocal exchange” captures this principle of mutual exchange of insurance contracts and obligations among its members.

Surplus remaining after covering expenses and claims is typically redistributed among members; however, significant deficits might necessitate additional capital contributions.

The financial accountability of members is defined by the policy type: assessable or nonassessable. With an assessable policy, subscribers face potential liability for additional payments if the exchange experiences unexpectedly costly claims or financial difficulties, requiring them to contribute more capital up to a predefined cap. However, most modern-day reciprocals offer nonassessable policies, meaning excess losses will not require additional charges.

The capital structure of many reciprocal exchanges distinctively relies on surplus notes for initial funding and long-term viability, a significant departure from the capital structure of traditional insurers. Unlike stock companies that raise capital by issuing shares to investors or mutual companies that build surplus through accumulated retained earnings over time, reciprocals cannot issue stock because they are unincorporated associations.

Surplus notes, essentially a form of debt, are treated as policyholder surplus or equity under statutory accounting principles, providing the necessary capital to meet regulatory solvency requirements and commence operations. This approach bridges the gap created by a lack of historical retained earnings, as policyholder-owned entities prioritize member benefit over external shareholder profit, with capital growth derived primarily from underwriting profits and investment income.

This unique capital structure inherently links policyholders, or subscribers, to the reciprocal’s financial health as contributors and potential recipients of surplus. Beyond their premium payments, policyholders may directly contribute to the exchange’s surplus through specific charges, often termed “subscriber surplus contributions.” These policyholder contributions are made in addition to premiums paid, initially, and over the first few years. Conversely, any surplus generated by the reciprocal ultimately belongs to its policyholders, and it can be distributed back to the members in various ways.

In terms of years in operation, 22 of the 27 recently formed reciprocals commenced business between 2022-2024. Considering the underwriting and operating expenses incurred to get these businesses started, in addition to the accounting rules pertinent to initial reinsurance agreements in many cases, pretax and net operating income for most of these newer reciprocals remained negative at the end of 2024. Going forward, the operating results should be more reflective of the success, or lack thereof, of these reciprocals rather than primarily being reflective of initial startup costs and operational expenses.

The rapid proliferation of these newer, often less-seasoned reciprocals also underscores the critical importance of execution risk and leads rating analysts to meticulously monitor actual results against initial projections and thoroughly scrutinizing business plans, initial capitalization strategies (especially the use of surplus notes) and the robustness of reinsurance programs. Furthermore, the strength and experience of their AIF and associated management partners are closely evaluated, along with the reciprocal’s governance and underwriting discipline.

AM Best rates more than two dozen reciprocals, with most having a balance sheet strength assessment of very strong. Most newer formations have started on the lower end of the very strong assessment given their substantial dependence on surplus notes, though often offset by robust reinsurance programs. Ultimately, as these exchanges mature organically and rely less on surplus notes, there is potential for these companies to improve to the higher end of the very strong balance sheet strength assessment.

While prospective market conditions suggest a continued vital role for reciprocals in providing capacity for segments affected by market dislocation, particularly concerning coastal property, their sustained success hinges on effectively managing severe catastrophe events, appropriately managing expenses (including fees to the AIF) and maintaining strong financial health under this heightened oversight. The market dislocation will typically stem from the diminished insurer risk appetites where prevailing risks or market conditions yield unfavorable results. At the same time, reciprocals offer a compelling option in the face of these market challenges due to their unique member-owned structure, which inherently focuses on providing “at-cost” coverage. This model promises potential for lower administrative overhead and fosters a strong alignment of interests between the policyholder and the insurer.

A longer version of this article was published by AM Best in a report titled “Reciprocal Insurance Exchanges Represent a Unique and Collaborative Structure.“

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  Berry Producer Driscoll’s Sued Over Alleged Use of Forever Chemicals

Berry Producer Driscoll’s Sued Over Alleged Use of Forever Chemicals  AI Pushes Underwriting Beyond Risk Selection to Prevention

AI Pushes Underwriting Beyond Risk Selection to Prevention