There was a time not so long ago when Hartford, Conn., was widely known as the “Insurance Capital of the World.”

These days, Hartford has work to do to reclaim that title.

But with insurance technology companies opting to start up in U.S. cities like Silicon Valley, New York and Chicago, and in places like London, Singapore and Shanghai outside the United States, can any one city lay claim to the title “InsurTech Capital of the World” today?

It depends on the counting method being used. An analysis provided exclusively to Carrier Management by Venture Scanner (venturescanner.com), an analyst and technology-powered research firm, highlights the point. Venture Scanner’s data reveals that the cities of London, New York and San Francisco rank highest by a simple count of the number of InsurTechs in each city. Looking at concentrations of funding dollars instead, London sinks to 12th place, with Palo Alto and San Francisco, Calif., commanding the two top spots—each with over $2 billion.

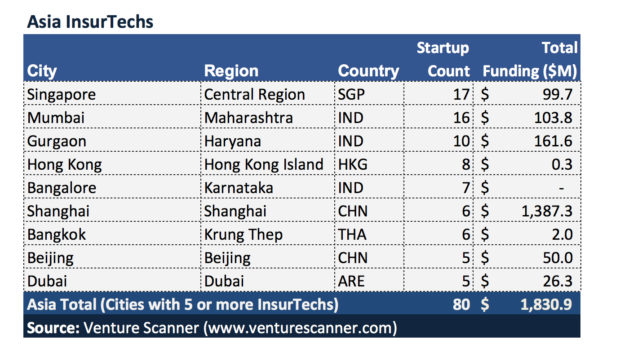

New York City’s 61 InsurTechs still puts it in the top three in a ranking of cities by InsurTech funding dollars, but the city that never sleeps comes in neck-and-neck with its sleepless Asian counterpart, Shanghai, China—each with nearly $1.4 billion raised by InsurTechs.

The leaderboard also depends importantly how “InsurTech” is defined.

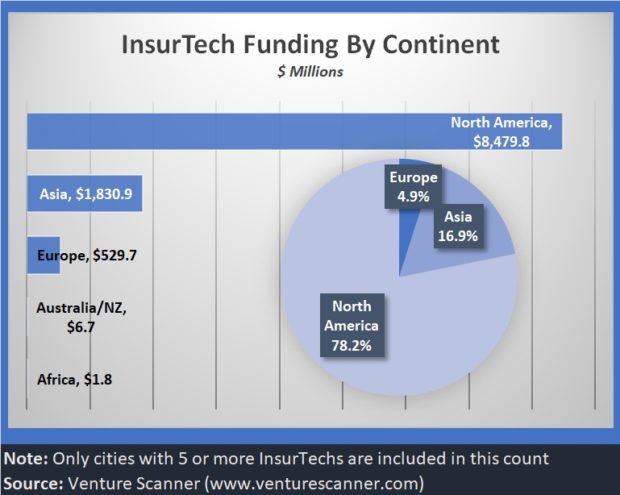

Venture Scanner defines InsurTechs as companies falling in one or more of these 14 categories: Automotive; Employee Benefits; Enterprise/Commercial; Health/Travel; Data/Intelligence; Consumer Management; Comparison/Marketplace; Education/Resources; Infrastructure/Backend; User Acquisition; Life, Home, P/C Insurers; P2P Insurance; Product; Reinsurance. At the date of this writing in early February, the firm had counted 1,458 InsurTechs in 61 countries with total funding of $20.8 billion.

Venture Scanner captures all publicly known funding events, including all sources (VCs, corporates, PE, etc.) and rounds (early stage, late stage, post IPO equity, etc.), according to Nathan Pacer, Venture Scanner’s co-founder and chief research officer. The vast majority of those funding events (more than 95 percent) occur from 2011 onward, he noted.

Cities are determined by Venture Scanner using each company’s “self-described location,” Pacer said, noting that this generally correlates to their operational headquarters.

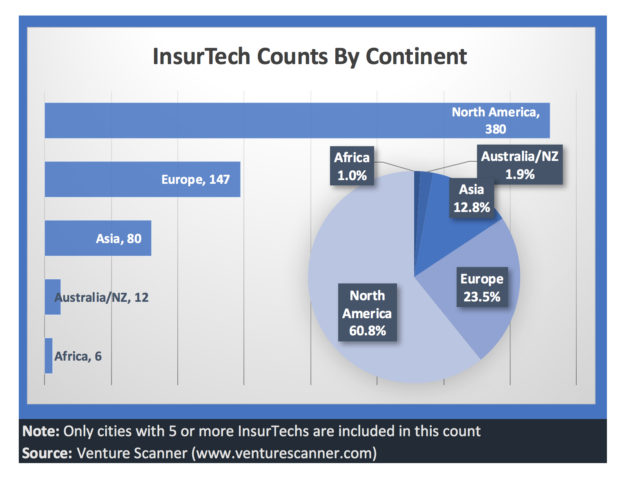

In January, when the city ranking data was compiled for Carrier Management, Venture Scanner counted 1,438 InsurTechs with $19 billion of funding, with 625 of them located in cities that had five or more InsurTechs (CM chart totals). That means that more than 800 others are scattered in cities with four InsurTechs or less, underscoring the fact that insurance technology startups are a worldwide phenomenon.

The P/C Capitals: London and Palo Alto Still Reign

Analyzing some of the underlying data for the 196 individual InsurTechs ranked in the top three cities on both lists, Carrier Management editors set out to examine several questions: Why do cities with small numbers of startups—like Shanghai and Palo Alto—have such large total funding amounts? Why does London have a low funding level compared to New York and San Francisco, with similarly high startup counts? And which of these cities is the capital of property/casualty InsurTechs?

A handful of outliers stood out, with large funding amounts for Palo Alto and Shanghai and a predominance of early funding rounds in London. London also has a higher percentage of P/C InsurTechs than either New York or San Francisco, making the home of Lloyd’s the P/C InsurTech Capital of the World by sheer number of startups.

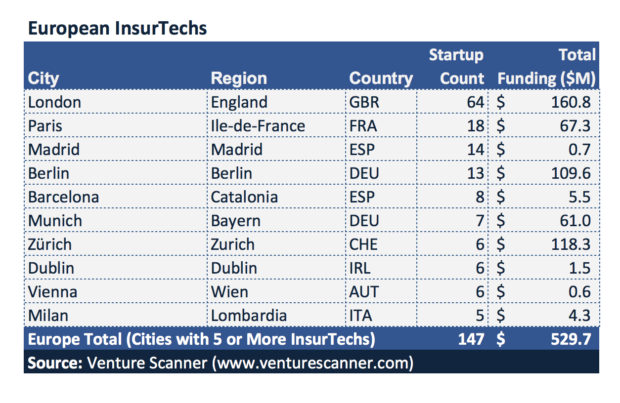

London: London tops the European InsurTechs in Venture Scanner’s analysis, with 64 startup counts, but those attracted only $160.8 million in overall funding. Unlike New York and San Francisco, for which Venture Scanner lists some startups involved in Series B, C or D funding rounds (several with $100 million-plus funding amounts on their own), there are no London InsurTechs described in the database as having progressed past Series A. (Venture Scanner identified the latest round funding type for 31 of 64 London InsurTechs. Among these, 10 are seed or angel funding and 13 are Series A. Eight others are simply identified as venture or PE.)

Fifty-six London startups—more than 85 percent of the total counted by Venture Scanner—have some ties to P/C insurance based on Carrier Management’s reading of descriptions on the individual company websites. For all locations, including London, however, determining the type of insurance that each technology firm serves turned out to be a challenge. Particularly, for companies delivering infrastructure and back-end services, user acquisition technology, or data and artificial intelligence, many websites fail to make any reference to insurance type—an indication perhaps that InsurTech executives see little need for line of business or even life vs. non-life policy distinctions.

Fifty-six London startups—more than 85 percent of the total counted by Venture Scanner—have some ties to P/C insurance based on Carrier Management’s reading of descriptions on the individual company websites. For all locations, including London, however, determining the type of insurance that each technology firm serves turned out to be a challenge. Particularly, for companies delivering infrastructure and back-end services, user acquisition technology, or data and artificial intelligence, many websites fail to make any reference to insurance type—an indication perhaps that InsurTech executives see little need for line of business or even life vs. non-life policy distinctions.

Palo Alto: With over $2.1 billion from private investors captured in Venture Scanner’s report to Carrier Management, data mining giant Palantir dominates the funding totals, putting its Palo Alto location at the top of the worldwide funding list. But while Palantir is clearly a technology company, it might not make every list of insurance technology companies given its broad mission across industries and government entities.

According to Palantir’s website, “Palantir is a mission-focused company…dedicated to working for the common good and doing what’s right, in addition to being deeply passionate about building great software and a successful company.” While Palantir does not focus on insurance technology as its main specialty, data projects involved with monitoring risks like cyber crime, terror and natural disasters are among those recounted on the website and in popular media. (See, for example, Forbes, “Palantir Connects the Dots with Big Data.“)

Separately, Zurich Insurance disclosed its collaboration with Palantir on “seven pilots leveraging key competencies of both companies” during a May 2015 Investor Day meeting, listing Palantir’s competencies in cyber, infrastructure scalability and advanced data correlation on a presentation slide.

Other familiar names with ties to P/C insurance in Palo Alto include the likes of NAUTO (providing advanced computer vision, AI for safe driving), Next Insurance (small commercial) and Cape Analytics (geospatial imagery). Ladder Life is the only life insurance enterprise among the seven names.

Shanghai: Zhong An, the Shanghai digital insurer, backed by founding partners Ping An, Tencent and Alibaba in 2013, has the second-largest single funding amount of any company located in one of the five cities for which Carrier Management reviewed company details. Venture Scanner’s data includes a $936.9 million total for funds raised prior to a $1.5 billion IPO in September 2017.

Absent Zhong An and some other funding totals captured by Venture Scanner primarily on the life insurance side, the funding for Shanghai InsurTechs would not even make the top 20 cities, nor would any other city in Asia.

New York City vs. San Francisco: On opposite coasts of the United States, New York City and San Francisco are among the top three cities worldwide in both startup counts and funding totals on Venture Scanner’s list of InsurTechs. But in both cities, InsurTechs devoted to health insurance and benefits rather than P/C insurance contributed significant amounts to total funding.

In the Big Apple, where Venture Scanner counts 64 InsurTechs with nearly $1.4 billion in total funding, Oscar Health’s $727.5 million in funding is half of the total. Eliminating more than two dozen InsurTechs without ties to P/C insurance, New York City’s startup count drops to 40 with funding of $562.7 million.

Similarly, in San Francisco, where the $583.6 million funding level of Zenefits and Clover Health’s $425.0 million together contribute $1 billion to the $2.3 billion city total, there are 23 InsurTechs unrelated to P/C insurance. Excluding these organizations, San Francisco still ranks below New York City in startup counts (35 for San Francisco vs. 40 for NYC) and ahead of the East Coast metropolis in funding dollars ($812.7 million vs. $562.7 million.)

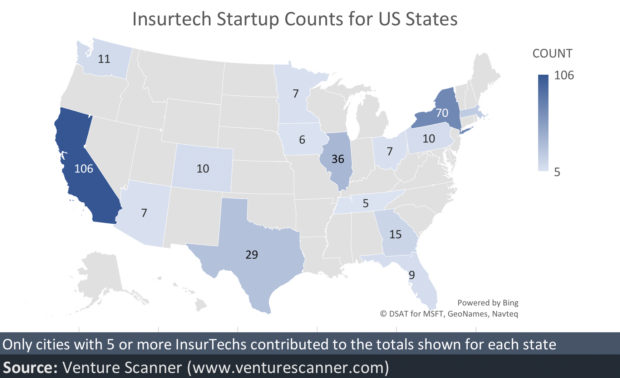

Considering all types of InsurTechs—related to life, health, benefits and non-life—the only other city in New York state with five or more InsurTechs is Brooklyn. In California, InsurTechs located in San Diego, Los Angeles, San Mateo and Mountain View, combined with San Francisco and Palo Alto, bring the Golden State total over 100.

Hartford on the Move

The city rankings that Venture Scanner provided to Carrier Management only include cities with five or more InsurTechs. While Hartford, Conn., didn’t make the cut, the city is working hard to get back on the world map of insurance capitals.

As Insurance Journal’s East Coast Editor Elizabeth Blosfield reported in December last year, Hartford InsurTech Hub selected 11 startups to take part in an InsurTech Accelerator program. Hartford InsurTech Hub, an initiative established by Hartford-based insurance carriers, the city of Hartford and CTNext, is part of Startupbootcamp, a global network of industry-focused accelerator programs. Carrier program partners include Cigna, The Hartford, Travelers, USAA and White Mountains. Recently Atlanta-based claims manager Crawford & Company signed on as a partner as well.

The initial cohort of 11 InsurTechs, selected from more than 4,000 startups from 96 different countries and 850 cities, relocated to Hartford and started working at Upward Hartford, a co-working space, private office and conference facility, in early January for a three-month period.

While Hartford may have arrived late to the InsurTech party, the historical significance of the city—and the state of Connecticut—in the insurance industry is well documented. In November 2017, PwC and the Connecticut Insurance & Financial Services initiative (CT IFS) published an 88-page report (“2017 Connecticut Insurance Market Brief: Ready Set Innovate“) describing a history of innovation in the state along some figures that answer the question “Why Hartford?” for startup consideration. Using information sourced from the Connecticut Economic Research Center, Moody’s Analytics, the Department of Labor and the Connecticut Insurance Department, the report noted, for example, that:

- Connecticut ranked third in the U.S. in direct written premiums in 2016, with 1,449 domestic and nondomestic insurance companies licensed to do business there.

- Connecticut ranks first nationally in insurance carrier employment as a percentage of total employment (2.6 percent) and in insurance payroll as a percentage of total payroll (5.1 percent).

- With 850 actuaries employed in the state and earning an annual mean wage of $118,510, Connecticut has the highest concentration of actuaries in the U.S.

“The insurance revolution is happening in Hartford. World-class companies and determined employees are driving change,” executives from CT IFS wrote on the opening page of the report.

InsurTech Boom in the Startup Nation

In a different part of the world, an InsurTech revolution not revealed by the Venture Scanner data has already happened, according to Donald Light, a research director in the insurance practice at Celent.

Light, who authored a report titled “InsurTech in Israel: Global Implications,” points to characteristics unique to Israel to explain why InsurTech activity in the “Startup Nation” is booming. Referring to the title of a 2009 bestselling book, “Startup Nation: The Story of Israel’s Economic Miracle,” Light noted that the small country is a global leader in technology and VC-fueled startups.

Focusing on InsurTechs specifically, Light wrote that capabilities in cybersecurity, cyber warfare, fraud mitigation, machine vision, and the application of AI and machine learning to huge datasets used for national intelligence all are byproducts of “geostrategic necessity.” Outstanding technical and scientific education and an Israeli army that exploits technological advantages are further contributors to a startup ecosystem, he wrote, noting that mobility has also emerged as an InsurTech theme in Israel.

“A proof point is that over 80 InsurTech startups competed in [an] ‘InsurTech Israel Competition'” in early 2017, said Light’s report, which also highlights the activities of carriers like AXA and AIG in support of insurance technology companies in Israel and describes some notable Israeli InsurTechs, including Click-Ins and Mobileye.

Click-Ins, the developer of the getmeins platform designed to combat insurance fraud based on military-grade intelligence, is one of two InsurTechs included in the Venture Scanner database for the city of Netanya in Israel. Venture Scanner confirmed that no city in Israel shows up with five or more InsurTechs in its database, which partially explains why Netanya, Tel Aviv and Ramat Gan aren’t visible on the rankings developed for this article.

It doesn’t explain the absence of Mobileye, a developer of advanced driver assistance systems and autonomous driving technology, highlighted in Light’s report as another proof point of Israel’s InsurTech boom, underscored by the fact that Intel paid more than $15 billion to acquire the company in March 2017.

“Mobileye’s global headquarters are in Jerusalem. However, the company also has a main office in New York City, as well as representatives in major cities around the world,” a Mobileye representative told Carrier Management, going on to highlight the company’s ties to the insurance industry, including a partnership with Munich Re announced in September 2017 designed to protect commercial fleets and other Munich Re clients.

(Venture Scanner actually has Mobileye based in Amstelveen Netherlands in its database. The Netherlands appears as a “jurisdiction of incorporation” for Mobileye N.V. on past SEC filings that Carrier Management discovered through an online search.)

Contacted by Carrier Management about the Israeli InsurTech landscape, Light also pointed us in the direction of an online database of Israeli startups of all types at startupnationcentral.org. Searching that database using the tag “insurtech,” Light and Carrier Management both uncovered more than 60, including established insurance technology firms like Earnix and Bolt Solutions as well as newbies such as cyberwrite and Lemonade.

Responding to a request to understand what locations are used to compile the data, representatives of startupnationcentral.org replied: “According to our methodology, [a] company counts as an Israeli company if its co-founders or R&D [are] based in Israel.”

While Venture Scanner captured Earnix and cyberwrite as Israeli companies, Venture Scanner’s database lists both Bolt and Lemonade as New York companies.

Lemonade’s ties to Israel became clearer in January, when Lemonade Co-founder Shai Wininger called out Amazon for poaching the Israeli employees of his insurance carrier powered by artificial intelligence and behavioral economics in several social media posts. While Lemonade’s LinkedIn page indicates that the company’s location is New York, Wininger’s personal LinkedIn page puts him in Israel. According to a communications office at Lemonade, the company is headquartered in New York and its R&D teams are based in an office in Tel Aviv.

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act

As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?