The people specifically charged with moving innovation forward at property/casualty insurance companies are more optimistic about reaching their goals and garnering organizational support for their efforts than they have been in past years, a new survey reveals.

In 2017, they feel “the wind in their sails,” said Michael Fitzgerald, a senior analyst in Celent’s Insurance practice, reporting on results of a survey of 29 innovation practitioners at financial services firms, including 11 P/C insurers and nine life insurers.

“The people that are actually out there doing this very difficult transformation work are feeling more supported than they have in the past,” Fitzgerald said, commenting on findings in a new Celent report published in April, titled “Innovation Outlook 2017: Making Progress,” which found that more than half of the 29 respondents expect it will be easier to accomplish their goals in 2017.

“Obviously, we asked the question, and they said they’d like more [support]. But at least it’s not quite like it has been in past years; it’s much more optimistic,” he said.

Among other survey findings:

- Innovation programs for survey respondents are between two and three years old; they focus on incremental innovation; and innovation is budgeted for as part of technology spending.

- Innovation areas earmarked for the greatest investments are “technologies enabling innovation” and spending on external and internal staff. Venture investments and investments in standalone startup companies separate from core businesses are lower priorities, although greenfield efforts are rising compared to past years.

The report is one of several on innovation that Celent published this year, but this one is distinguished by its exclusive focus on people that Celent “identified as working full time on innovation,” Fitzgerald said, noting that some carry the title chief innovation officer, while others are chief digital officers or transformation leaders. The much smaller sample size allowed for a more qualitatively focused report, he noted, later sharing some insights on responses to open-ended questions.

An earlier report titled “Innovation in Financial Services Survey 2017: Leaders Emerge,” published in January, presented survey responses from 194 financial services professionals to give a sense of what the general population of financial services professionals believes is happening on the innovation front. Despite the broader participant profile, survey responses also moved in a positive direction compared to past surveys of a similar group conducted in 2013 and 2015. Indeed, for the first time, more than half of the participants in the broader survey identified innovation as “critical to executing business strategy.” That’s up from just 26 percent in 2013.

“I characterize the market as being motivated this year by fear––fear of being left behind, fear of not knowing, more fear than before about what might happen.”

“I characterize the market as being motivated this year by fear––fear of being left behind, fear of not knowing, more fear than before about what might happen.”

Mike Fitzgerald, Celent

Fear Motivates Action

Both reports, however, reveal a focus on incremental innovation rather than disruptive innovation, with half of the innovation practitioners in the latest report spending 90 percent or more of their time on incremental change.

What’s the difference?

Providing references from outside the insurance industry, Fitzgerald said discount carrier Southwest Airlines in its early days and iTunes are classic examples of disruptive innovation. “It addresses a new market or an underserved market.”

Innovation that’s incremental is still significant, he said. “It’s not just an improvement. An incremental innovation means that you basically ‘break a tradeoff,'” he said, offering cost-time or quality-cost tradeoffs to explain the phrase. “So, for example, you can settle a claim five-times faster. That’s got great value, [but] if you’re settling a standard claim in a standard market, it’s not really disruptive. It just means that you can jump higher and run faster than your competitors.”

Summing up the distinction, he said: “Are you making a new market? Are you doing it with a new product? Or are you doing something that’s serving an existing market and an existing customer but you’re doing it in a way that breaks a cost-time or quality-cost type tradeoff that most of the market is dealing with?”

Insurers overwhelmingly self-report that they work on innovative changes to existing markets, he said.

Despite the optimism about meeting innovation goals this year, there’s room for more innovation in the insurance industry, Fitzgerald suggested, noting that an outside disrupter could push industry innovation efforts further. Drawing an analogy to a natural catastrophe that changes the direction of a soft property insurance market, he said, “That really is where P/C innovation is right now. We really do need a good threat.”

Banks and other financial institutions involved in payments and loans, which indicated a preference for disruptive innovation, have already faced a number of different threats, he said, pointing to the likes of PayPal and Lending Club. And wealth managers face threats from robo-advisers, he added.

“What property/casualty insurance really needs is one of these new models that are out there testing to be very, very successful in order to spur this along,” he said. “You’ve seen a little bit of that. The market overall on innovation has been one [that went] from curiosity to one [in which] I sense that a number of companies are starting to feel a bit threatened.

“I characterize the market as being motivated this year by fear––fear of being left behind, fear of not knowing, more fear than before about what might happen. But we really do need somebody to come in and rock the market with a great innovative approach which will cause people to evaluate these against the usual day-to-day business.”

In fact, a telling result of the innovation practitioners survey is that more than three-quarters expect outside disruption to increase in 2017.

Asked whether he sees any candidates emerging to become the PayPal of insurance, Fitzgerald pointed to Slice Labs as a potential disrupter. “But it’s way too early to tell you that,” he added quickly.

Fitzgerald recently published a new report titled “Slice Labs: A Case Study of Insurance Disruption,” describing the company’s new product for the underserved market emerging from the sharing economy—combining personal and commercial coverages in a single homesharing insurance contract, with coverage delivered on a per-use basis through a digital automation platform.

P/C Insurers Further Along

In spite of the lack of disruptive innovation, Fitzgerald believes that P/C insurers have made more investment in innovation than counterparts on the life/health side. He also agreed with the idea that reinsurers have been particularly active in efforts to drive innovation forward, pointing to business model threat as the probable reason.

“There’s tons of reinsurance capacity out there, so they have to figure out a way to grow,” he said, explaining why some are backing direct propositions they otherwise might not have considered in the past.

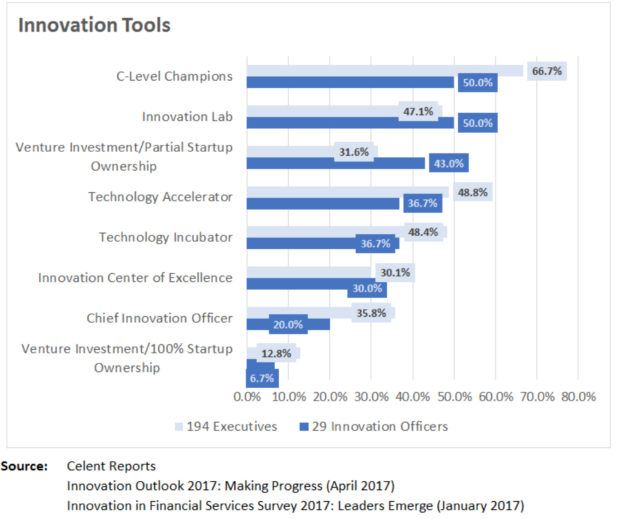

Celent’s two surveys also provide insights about the tools respondents say their companies are using to drive innovation, including setting up Innovation Labs and participating in technology accelerators.

Additional information in the reports includes insights on customer expectations, comparisons to other industries, innovation barriers, as well as satisfaction levels of respondents with innovation programs and with executive buy-in. To analyze executive support, Celent presents a Net Promoter Score methodology to identify which categories of top executives the respondents view as promoters of innovation and which are detractors. The reports also include Celent’s detailed recommendations outlining best practice approaches to innovation.

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act

As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act  Global Wildfire Surge Hits U.S, Propelled by Rising Temperatures

Global Wildfire Surge Hits U.S, Propelled by Rising Temperatures