Machines can take over a chunk of the activities of nearly every one of 750 occupations studied by researchers from McKinsey Global Institute recently—including chief executive officers and several occupations related to the insurance industry.

The Dec. 14, 2015 HBR article, “How Many of Your Daily Tasks Could be Automated?” is available on the Harvard Business Review website.

Another 13 percent could be automated if “technologies that process and ‘understand’ natural language were to reach a median level of human performance,” the researchers say.

Bottom line: For 60 percent of U.S. jobs, 30 percent or more of the activities can be automated with available or announced technologies.

While the paper also reveals that only 5 percent of jobs can be fully handled by machines, what isn’t instantly revealed from the paper or the article is exactly which occupations fall in that category—and which are only partially vulnerable to automation. Embedded in the report, however, is a link to an interactive analysis allowing readers to find out where their particular jobs stand—and how much of their tasks can be automated.

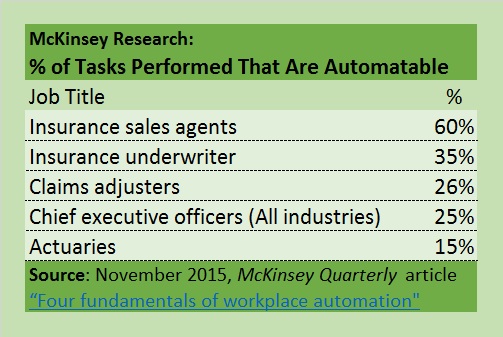

What does it show for insurance industry jobs?

Without revealing all the details available to McKinsey Quarterly readers, we highlight some of the insurance-related job information extracted from the interactive analysis:

- Insurance sales agents and insurance underwriters fall within the 60 percent of U.S. jobs for which 30 percent or more of job tasks can be automated.

- Insurance sales agents are at the high end of that range—with machines capable of performing more than half (65 percent) of their tasks; insurance underwriters are closer to the low-end threshold (35 percent of their work activities are automatable).

- Claims adjusters, CEOs and actuaries are also vulnerable, but much less so. Actuaries are the least vulnerable. In other words, a greater percentage of CEO tasks can be automated than actuarial tasks. (Chart below.)

Readers clicking through McKinsey’s interactive analysis can also view the number of estimated workers in each profession analyzed, their average hourly wages and lists of activities the researchers believe are among those likely to be a part of each of the 750 jobs. It turns out that the researchers only list about a half-dozen tasks for insurance underwriters and actuaries, while claims examiners have four times as many activities on their to-do lists.

The researchers also don’t list as many possible tasks for agents (less than 20) as they do for claims professionals and CEOs (for whom nearly 50 potential tasks are listed). Agent responsibilities include activities like attending events to develop professional knowledge, identfying customers, developing professional relationships and networks, processing sales, and preparing contracts.

While the interactive graphic does not reveal which of these tasks McKinsey has identified for potential mechanization through “currently demonstratable technologies,” the paper does give some clues in a discussion of sales work generally. “Sales organizations could use automation to generate leads and identify more likely opportunities for cross-sell and upselling, increasing the time front-line salespeople have for interacting with customers and improving the quality of offers.”

That summary echoes a key point of the paper for all the partially automatable executive officers in the U.S. to consider as they perform one of their many tasks: evaluating organizational activities. “When you’re bringing in automation you need to think about two kinds of payoff: returns you get by using machines rather than labor for activities…plus the value derived from activities that employees carry out in the time…formerly used for work that is now automated,” the McKinsey researchers write in the HBR article.

In the McKinsey Quarterly paper, they expand on this. “When we modeled the potential of automation to transform business processes across several industries, we found that the benefits (ranging from increased output to higher quality and improved reliability, as well as the potential to perform some tasks at superhuman levels) typically are between three- and ten-times the cost,” they write.

Underwriters and Agents

Among the 750 occupations analyzed by McKinsey, all the insurance professionals and CEOs fall somewhere between home health aides, massage therapists and clergy—professions for which none of the activities can be automated—and the fully automatable activities of sewing machine operators and package-filling machine operators.

Among the 750 occupations analyzed by McKinsey, all the insurance professionals and CEOs fall somewhere between home health aides, massage therapists and clergy—professions for which none of the activities can be automated—and the fully automatable activities of sewing machine operators and package-filling machine operators.

Even though McKinsey shows underwriters faring much better than agents, other views on the matter have surfaced in alternative reports. In fact, CareerCast.com—the Internet site that repeatedly ranks insurance actuaries among the top careers—recently listed insurance underwriter among the “most endangered jobs of 2015.”

Insurance underwriter was listed No. 9 of 10 endangered jobs. The one-sentence reason given for the distinction did not directly mention automation or technology—the culprits that CareerCast clearly says are putting mail carriers and meter readers at the most peril. Here’s how CareerCast explained the underwriter listing: “Streamlined processes allow agents to take on the work previously handled by underwriters.”

Hat tip to John Najarian, Life/Health chief underwriter for GenRe, who considered the CareerCast ranking in a Dec. 13, 2015 GenRe blog item titled “Is Automation Going to Put an End to the Underwriting Profession?”

“To be clear, this is not a debate of the projection. The U.S. Bureau of Labor Statistics projected that between 2012 and 2022, the number of underwriting jobs across all industries will shrink from 106,300 down to 99,800, a drop of 6 percent,” he wrote.

Najarian talks about demographics (aging underwriters), outsourcing and finally automation as factors driving the decline of the profession on the life/health side.

“We underwriters need to embrace—indeed promote—the progress toward automation. It improves the intrinsic job quality by eliminating the time and energy needed for mundane cases, and it improves the overall business outcome. One benefit among many is that automation helps to improve consistency of underwriting decisions.

“And let’s not forget underwriters are still needed to design, monitor and revise the rules running automation. That is one reason why the job reduction drops 6 percent and not 60 percent or even higher.”

Others are less optimistic about the underwriting profession. For example, BBC.com offers an interactive graphic—”Will a robot take your job?”—published on Sept. 11, 2015. Typing in the job “insurance underwriter” returns the following verdict: “Likelihood of automation? It’s fairly likely (66%).”

The BBC.com site lists Michael Osborne and Carl Frey from Oxford University’s Martin School and their 2013 report, “The Future of Employment: How Susceptible Are Jobs to Computerization,”as a source of information for the graphic. That report actually listed insurance underwriting as the fifth most susceptible to automation—coming in at No. 698 of 702 occupations studied, where high numbers indicate vulnerability. Insurance agents fared better in that analysis—ranked at No. 565. (Wells Media Editor Denise Johnson reported the opinions of industry analysts on the Oxford ranking earlier this year. See related article, “Will Artificial Intelligence Replace Industry Jobs?“)

Another Economist’s View

McKinsey’s work suggests that “a significant percentage of activities performed even by the highest-paid occupations”—like CEOs—”can be automated by adapting current technology.” Indeed, their paper notes that activities consuming more than 20 percent of a CEO’s working time—analyzing reports and data to make operational decisions and reviewing status reports, for example—don’t necessarily need humans to accomplish them. On the other end of the pay scale, for home health aides, landscapers and maintenance workers, McKinsey says that only a very small percentage of the activities involved in doing these jobs could be automated with current technology.

But like McKinsey, Haldane also carved out health workers and social workers from that analysis, adding certain skilled artisans—like hairdressers—to his examination of professions less likely to be handled by machines. “No one anytime soon is I think going to choose a robot to cut their hair…Nor are they likely to choose a robot to look after their young children or elderly parents.”

Haldane and the McKinsey consultants aren’t exactly in sync on hairdressers, with Haldane citing the BBC.com calculator putting the job’s automation prospect at 33 percent, while McKinsey’s tool suggests that 65 percent of a hairdresser’s activities can be done by machine. Haldane actually used hairdressers and accountants to weave his way through the centuries, giving a historical perspective of emerging technologies in the 18th, 19th, 20th centuries, explaining how each Industrial Revolution reshaped the labor force. “Often, it has led to a so-called “hollowing out” of midskilled workers and a widening wage gap across the economy,” he said, at one point.

Still, Haldane also noted that “as machines displaced man in conducting manual tasks, man has kept one step ahead of the machine by continuously skilling-up to meet the new demands,” illustrating the demise of farmers and the rise of professions like accounting over time.

On the downside, he noted that while each phase of technological advancement “has eventually resulted in a growing tree of rising skills, wages and productivity,” each has also been associated with a further “hollowing out” of midskilled workers. And he admits that the latest technology wave may be different. “Why? Because 20th century machines have substituted not just for manual human tasks but cognitive ones too. The set of human skills machines could reproduce, at lower cost, has both widened and deepened.”

“For an accountant, the probability of vocational extinction is a whopping 95 percent,” he said, referring to the BBC figure. (Editor’s Note: McKinsey’s interactive graphic shows that the actitivies of accountants and auditors are 12 percent automatable.)

Still, Haldane offers a glimmer of hope for human workers in a section of the speech where he contrasts the problem-solving skills of humans with the algorithmic learning processes of machines, which need to sift through long strings of big data to solve problems and learn.

“These different approaches…are important when defining where humans may have the edge. This appears to be in tasks requiring high-level reasoning—large logical leaps of imagination rather than production and perception. And it is activities where EQ trumps IQ, where social capital is scored as or more highly than financial capital,” he said, defining EQ as “emotional intelligence quotient.”

(Additional Reporting: Andrew G. Simpson, Chief Content Officer, Wells Media)

The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums