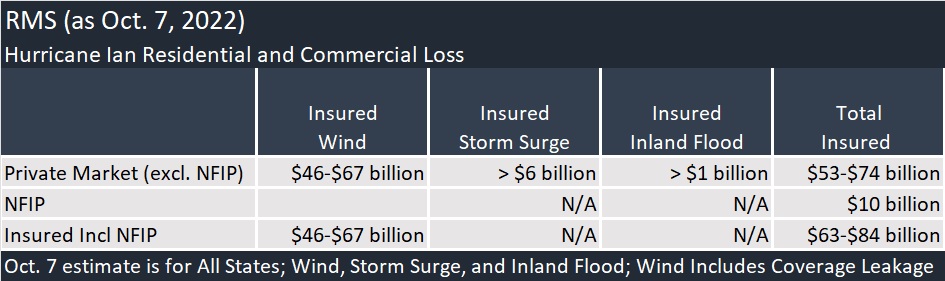

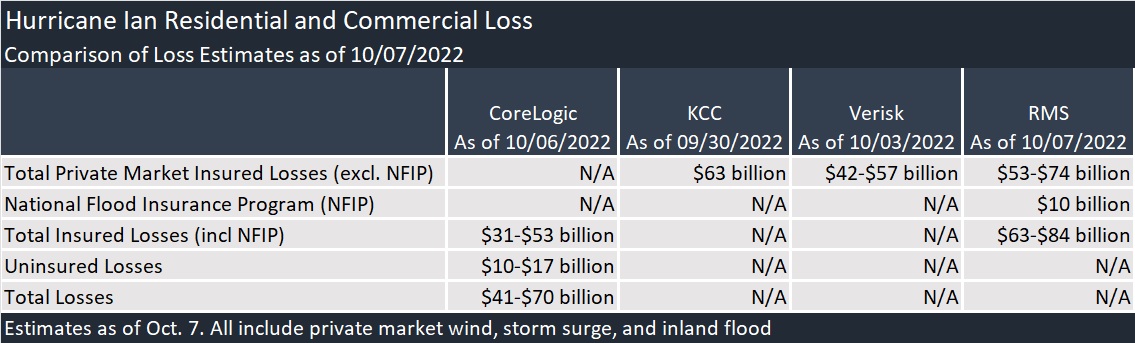

On Friday, Oct. 7, RMS published a $53-$74 billion estimate of the range of losses coming to private market insurers from Hurricane Ian.

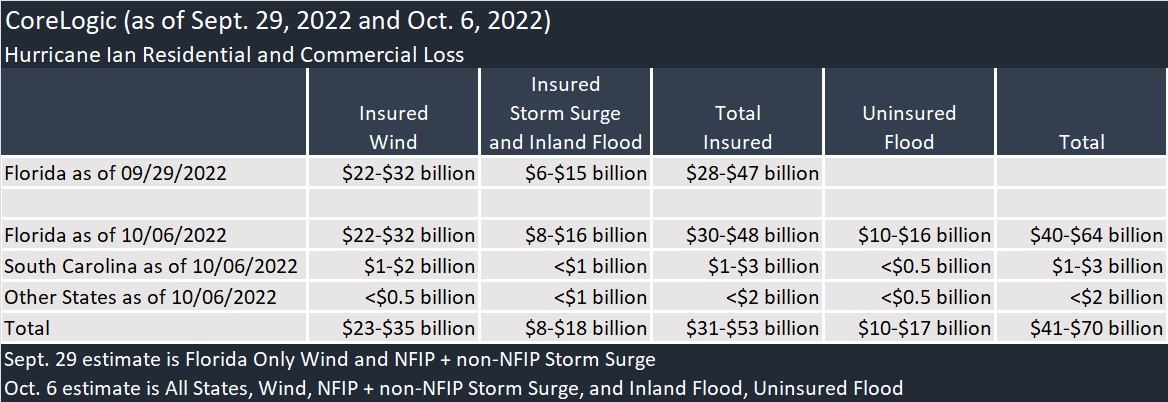

The low end of the range, coincidentally matched the high end of a range published by CoreLogic a day earlier for both private market insured losses and losses to be covered by the National Flood Insurance Program.

RMS, a Moody’s Analytics risk modeling company, said its best estimate of total private market insured losses from Hurricane Ian is $67 billion. RMS also estimates that the NFIP could see an additional$10 billion in losses from storm surge and inland flooding as a result of the event.

The RMS estimate reflects losses from property damage, contents, and business interruption, across residential, commercial, industrial, automobile, infrastructure, watercraft, and other specialty lines.

The estimate also considers the impacts of post-event loss amplification (demand surge), inflation, and non-modeled sources such as the Assignment of Benefits and litigation.

Updating earlier estimates of wind and storm surge losses for Florida to add provisions for other states impacted by Hurricane Ian, and Florida inland flood losses, CoreLogic now puts total insured losses in the $31-$53 billion range.

In an announcement Thursday, CoreLogic upped earlier estimates for insured Hurricane Ian losses for the state of Florida that had been published on Sept. 29 to include an estimate of Florida inland flood. CoreLogic’s estimates of water-driven insured losses for Florida now fall in the $8-$16 billion range. Estimated Florida wind losses from the global property information, analytics and data-enabled solutions provider remain unchanged at $22-$32 billion.

Adding wind and water losses for South Carolina and other states to the estimates, coming in at $1-$5 billion, brings total insured losses for the event to $31-$53 billion.

The storm surge and inland flood losses encompass both losses covered by private insurers and those that fall under the National Flood Insurance Program.

CoreLogic also published estimates of uninsured flood losses—$10-$16 billion for Florida, and $10-$17 billion for all states impacted by Hurricane Ian.

CoreLogic reported extreme riverine flooding along Peace River in Arcadia, Fla., located south of Tampa, and north of Punta Gorda. According to the modeler, Peace River, which normally runs 130 feet wide, flooded to more than a mile wide due to Hurricane Ian surge and rainfall. However, housing is sparse in this location which is designated as a Special Flood Hazard Area (SFHA) by FEMA.

“Without constraints in development in the SFHA, flood damages would have skyrocketed,” said Tom Larsen, senior director of Hazard and Risk Management, CoreLogic.

Explaining the more significant wind and surge losses, CoreLogic said Hurricane Ian’s large wind field and landfall path caused damage from those perils along the densely populated coast. “The key reason Hurricane Ian is so economically destructive is due to the massive growth in coastal real estate in Florida,” Larsen said in a statement. “Florida’s population has grown 50 percent since 1992 when Hurricane Andrew hit Miami, with disproportionately more growth in South Florida.”

“The extra costs incurred from the surge in repair needs simultaneous with a fragile economy are headwinds to rapid reconstruction and we should expect to see resident displacement and housing affordability issues in the state for some time to come,” he said.

Like CoreLogic, RMS expects the majority of total insured losses from Ian to be driven by wind. However, a sizable portion (up to 25 percent) of the total insured losses (incl. NFIP) will be driven by surge and flood. While insured wind losses and losses to the NFIP will be driven by residential lines, surge and inland flood losses to the private market will be dominated by commercial, industrial, and automobile lines, RMS said.

“Ian was a historic and complex event that will reshape the Florida insurance market for years to come,” said Mohsen Rahnama, Chief Risk Modeling Officer, RMS.

Jeff Waters, Staff Product Manager, Product Management, RMS, noted: “Much of the building stock affected by Ian was also impacted to varying degrees by Hurricane Irma in 2017 and Hurricane Charley in 2004. In some cases, roofs or structures were replaced after Irma and performed well in Ian. However, where buildings were not upgraded to recent codes, Ian’s destructive wind and storm surge will cause widespread roof replacements or total losses.”

Waters said the RMS key aspects of the Florida Building Code in its loss estimation process. “Aside from property damage, we expect significant losses to automobile and watercraft lines in this event due to fewer evacuations in the worst-affected region,” he said.

How They Compare

In addition to falling below RMS, CoreLogic’s range of insured loss estimates, which the firm described as its final estimate in an Oct. 6 statement, still falls below estimates from two other modelers—Karen Clark & Company (KCC), which published a flash estimate of $63 billion in insured losses for the U.S. and the Caribbean on Friday, Sept. 30, and Verisk, which announced an estimate of insured losses to onshore property in the range of $42-$57 billion on Oct. 3.

Related Article: Ian Insured Loss Estimates Rise: New High Over $60B

Unlike CoreLogic, KCC and Verisk have estimated privately insured losses only, excluding NFIP losses. Like RMS, KCC’s estimates and Verisk’s estimates also include provisions for estimated demand surge—post-loss amplification related to demand exceeding supply of materials and labor. The CoreLogic estimates do not.

“A sizable portion of the losses from Ian will be associated with post-event loss amplification and inflationary trends, said Rajkiran Vojjala, Vice President, Model Development, RMS. “A combination of high claims volume, additional living expenses related to the massive evacuation efforts, prolonged reconstruction in the worst-affected areas, and the prevalent higher-than-average construction costs will contribute to a significant economic demand surge.”

“Additionally, we expect the Assignment of Benefits and litigation—despite recent legislative efforts to curb their misuse, to influence the overall loss severity, especially in cases where coverage leakage of water losses onto wind-only policies is likely,” Vojjala added. “All these social inflation factors will lead to complex and lengthy claims settlement processes in this event, amplifying loss adjustment expenses and corresponding claim costs.”

The photo of hurricane damage in Fort Myers Beach was provided by EagleView Technologies, a geospatial technology company with a geospatial data and imagery library encompassing 94 percent of the U.S. population. EagleView shared more photos with Carrier Management, which are captured in the accompanying video presentation on Insurance Journal TV.

Eagleview’s Disaster Response Program has had the mission to support natural disaster response and recovery efforts with pre- and post-event imagery for over 15 years and is currently supporting six Florida counties with plans to continue across the state.

In preparation for Ian, the company staged a fleet of fixed-wing aircraft in counties along the state’s western coastline. As soon as weather conditions allowed, EagleView had planes in the air to capture high-resolution aerial imagery of the storm’s damage. Access to imagery is being rolled out to customers in local government, insurance and construction as soon as it becomes available, the company said.

Additional damage footage was captured via drone video by Insurance Journal’s Southeast Editor William Rabb and his son, August Rabb, who recorded the damage in the days after Ian’s Florida landfall.

Leadership Change at Vantage: Former Arch Execs Grandisson, Gansberg to be Chair, CEO

Leadership Change at Vantage: Former Arch Execs Grandisson, Gansberg to be Chair, CEO  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak