A report from Moody’s Investors Service clearly paints Ian as a loss event for Florida-only home insurers since large, national insurers have significantly reduced exposure in the Sunshine State throughout the years.

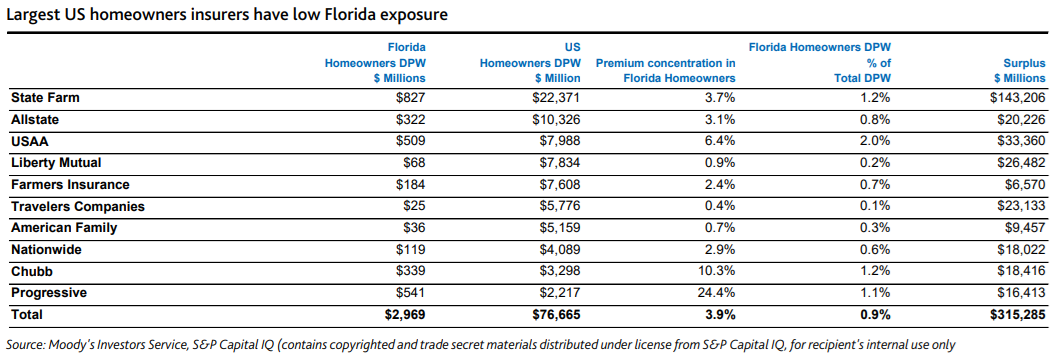

Six of the top 10 writers of homeowners insurance in the U.S. have less than 1 percent of their total writings in Florida. Homeowners direct premiums in Florida represented only 2 percent of the total book of business for the top 10 U.S. homeowners insurers, according to Moody’s.

Hurricane Ian “will not jeopardize capital for major P/C insurers, although it will reduce third-quarter earnings,” Moody’s said. “Large, national homeowners insurers have considerable resources to withstand a significant event based on careful monitoring of their coastal exposures, strong geographic diversification, high-quality reinsurance protection and strong capital bases.”

The opposite is true for Florida-only insurers (defined by Moody’s as insurers with at least 75 percent of home and commercial property premiums in Florida), which rely heavily on property-catastrophe reinsurance to bolster claims-paying ability. Moody’s said insurers highly reliant on reinsurance “could face a liquidity squeeze if there is a lag between the payment of insurance claims and reimbursement from reinsurers,” and face the possibility of capital loss if Ian or future events eclipse reinsurance limits.

Moody’s said auto losses, which will likely consist of total losses due to flooding, will account for a small share of overall losses. Commercial insurers can expect property, flood and business interruption claims, but the risk is spread among regional, national and international insurers, with Florida-only companies writing some small businesses.

However, reinsurers could be looking at “heavy losses,” which will ultimately be determined by primary insurance coverages and terms and conditions of reinsurance contracts. Many reinsurers have reduced exposure to Florida with the use of higher attachment points and more retrocessional coverage, as well as affiliated reinsurance sidecars. Moody’s expects Ian to be an earnings event for reinsurers, but capacity for capital-intensive lines like property-catastrophe reinsurance could be constrained in the near term. Since reinsurers have been ceding more business to alternative markets, substantial losses could be seen there as well.

“We expect property-catastrophe reinsurance pricing to increase significantly, particularly for loss-affected accounts in the U.S.,” said Moody’s.

Four Insurers Join Ward’s Annual Top 50 P/C Ranking for 2026

Four Insurers Join Ward’s Annual Top 50 P/C Ranking for 2026  Self-Driving Car Firms Must Address Emergency Vehicle Interference

Self-Driving Car Firms Must Address Emergency Vehicle Interference  U.S. P/C Industry Books Best Result in a Decade, but Not All Lines Enjoy Success

U.S. P/C Industry Books Best Result in a Decade, but Not All Lines Enjoy Success  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak