Ridesharing company Uber on Friday said it has new insurance to cover a gap between personal and commercial policies when drivers are using the app-based ridesharing service, while the company’s CEO said the San Franciscso-based firm is also working with insurers to develop more insurance products to cover the activity.

Uber made the announcement on a blog on its website in the morning.

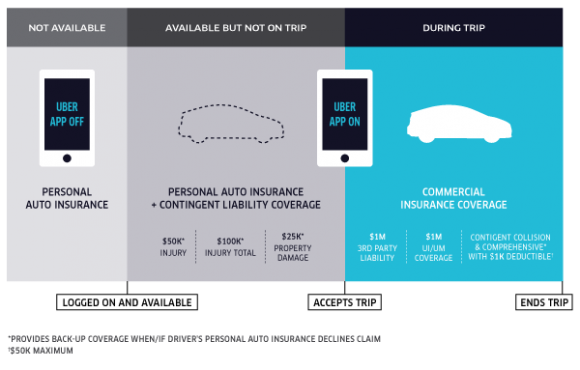

“Since the tragic accident in San Francisco on New Year’s Eve, there has been much written about an ‘insurance gap’ during the time that ridesharing drivers are not providing transportation services for hire, but have the Uber app open and are available to receive a trip request,” the blog stated.

The blog was referring to a car being driven by an Uber user who ran into and killed 6-year-old Sofia Liu. Her family has filed a lawsuit against Uber. Uber issued a statement saying the driver, 57-year-old Syed Muzzafar, was not responding to a fare didn’t have a passenger in his car when he struck Liu.

Uber appers to be the first company to have a policy that expands the insurance of ridesharing drivers to cover potential insurance gap for accidents that occur while drivers are not providing transportation service for hire but are logged onto the Uber network and available to accept a ride.

The new policy will provide contingent coverage for a driver’s liability at the highest requirement of any state in the U.S: $50,000/individual/incident for bodily injury, $100,000 total/incident for bodily injury and $25,000/incident for property damage, according to Uber.

This policy kicks in when a driver’s personal policy is no longer in effect, after a driver has turned on the Uber app, and before Uber’s $1 million commercial policy is in place, which covers drivers en route to make a pick up and when drivers have passengers.

Uber CEO Travis Kalanick described the policy, which is carried by its commercial specialty insurer, James River Insurance Co .

“I would say it’s almost like a contingent policy of sorts,” Kalanick said.

He said they haven’t come up with an official name for the type of coverage.

Transportation network companies like Uber, Lyft and Sidecar have become popular across the country and bills in several states as well as several city ordinances are in the works to create rules and regulations to govern these TNCs. Taxi companies and the insurance industry have also questioned the practice and are seeking restrictions or regulations to govern their operation.

Lyft and Sidecar spokespersons were asked if they planned on initiating coverage similar to what Uber announced.

Sidecar spokeswoman Margaret Ryan responded via email.

“We’ve been working with our insurance carriers over the last few months to offer the single, most comprehensive insurance coverage for peer-to-peer transportation,” she said. “Sidecar plans to provide coverage to drivers when they are live on the system but may not have a passenger in the car. We plan to roll out this coverage soon. This is in addition to Sidecar’s commercial liability insurance policy of up $1 million of coverage per occurrence. We’ve also added a new collision policy for drivers that will take effect in April.”

An email from Lyft spokeswoman Paige Thelen noted that the San Francisco-based company last month introduced additional coverages, including uninsured/underinsured motorist and collision.

“Lyft’s liability policy was designed to cover the time when drivers have passengers in their cars, as well as the period when a driver is on the way to pick up a passenger,” she said. “While we do expect personal carriers to cover the time period prior to carrying a passenger, in order to erase any uncertainty, Lyft will now provide additional protection. This new protection will provide backstop coverage to drivers when they are in match mode and are not providing rides. We will be rolling this out state-by-state in the days to come.”

Seattle’s city council has discussed an ordinance to create a two-year pilot program to deal these ridesharing services and the drivers. Seattle is believed to be the first U.S. city to come out with such regulations. Seattle Mayor Ed Murray said such services may be shut down if they don’t start carrying more insurance.

Bills backed by Uber have been introduced in Arizona and Colorado that are wending their way through legislature.

The Property Casualty Insurers Association of America, one of the groups speaking loudest about the gap in coverage, said Uber’s announcement on Friday makes a point the group has been harping about all along, which Uber has seemed to avoid acknowledging until now.

“This announcement makes our point,” said Robert Passmore, PCI’s senior director of personal lines policy. “We’ve always argued there needs to be specific insurance that applies to the ridesharing act for the entire time it’s available.”

PCI has been vocal that TNC drivers’ personal auto insurance is not intended to cover the activity of ridesharing, and that the act of providing a livery service is specifically excluded in most auto policies.

Despite the new coverage, Passmore believes there are still concerns that need to be addressed.

For example, proposed legislation in Colorado would enable TNCs to operate in the state under Colorado Public Utilities oversight, and it includes a livery exclusion, which states that when a driver is not providing a ride or on their way to pick up a ride, they are under their personal auto policies.

In some cases people may argue that the livery exclusion is actually boarder than the activities being performed, and therefore seek a lawsuit in the instance of an accident involving a TNC driver beyond what’s being paid from the insurance policies in place.

Passmore also expressed concern the new insurance also doesn’t address what happens when drivers, who often put large pink mustaches on their front bumpers to be easily identified, operate outside of Uber’s policies and accept street hails.

“They do have big pink mustaches on their cars and we know there are times drivers take rides outside the app,” Passmore said.

No fault states leave other question marks lingering over Uber’s new coverage, Passmore added.

Michigan has a no fault law that mandates unlimited medical coverage, while there are no fault laws in a number of states like New York, New Jersey and Florida, he said.

Travis said Uber’s new policy in place gives time for cities, states and the insurance industry itself to figure out how to better deal with ridesharing, and that Uber is working with at least one carrier to develop related products.

“Could an insurance company sell an endorsement on to your personal insurance if you happen to be a ridesharing driver?” he said, offering an example of the possibilities. “There’s a lot of really interesting things I think the insurance industry can do to create a market there.”

Travis said Uber looked at the highest minimum requirements for a state then matched that with its policy.

“50-100 is a pretty reasonable policy,” Travis said. “We feel it sort of goes down the fairway with what divers adopt for themselves.”

Travis declined to state how much Uber was paying in premiums for the insurance, but said its structured similar to its commercial policy in that it’s based on mileage.

“The bottom line is we are paying per mile, but we don’t like disclosing what per mile,” he said.

Uber posted a blog on Friday morning with this graphic explaining their new policy to cover a gap between personal and commercial insurance.

(This article was originally published on Insurance Journal. Reporter Don Jergler is the West Coast editor of Insurance Journal.)

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry  A Matter of Trust

A Matter of Trust  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz