For the last several years, participants in the insurance-linked securities (ILS) market have frequently discussed the question of market expansion. In a market with consistently declining property catastrophe yields and plentiful capital, these conversations often turn to the potential of ILS-based products in other lines of business, such as those falling under the category of casualty or liability (including financial guaranty) reinsurance.

Executive Summary

While progress has been made in the development of casualty insurance-linked securities (ILS), there still is significant work to do, says Aaron C. Koch of Milliman, who discusses some of the key structural and product design questions that must be answered before casualty ILS can meet the needs of cedents and capital market investors.In the wake of the major catastrophes of 2017, the attention in the ILS space has—perhaps justifiably—refocused itself on the rates and new issuances in the property catastrophe space. Investors eager to take advantage of the post-event rating environment have in many cases significantly expanded their capital commitments. If the desired property catastrophe rate increases fail to materialize, however, that capital will either need to be used elsewhere or be returned.

In that context, it is timely to revisit ILS’ potential in other lines of business, most notably casualty. Important progress has been made in establishing a precedent for casualty ILS transactions in the last several years, but there is still significant work to do. Only a limited number of successfully completed transactions have been seen to date. For the casualty ILS market to reach the expectations of its more optimistic supporters, it will need to continue to evolve and answer several key structural and product design questions in the upcoming years.

Initial Steps Toward Casualty ILS

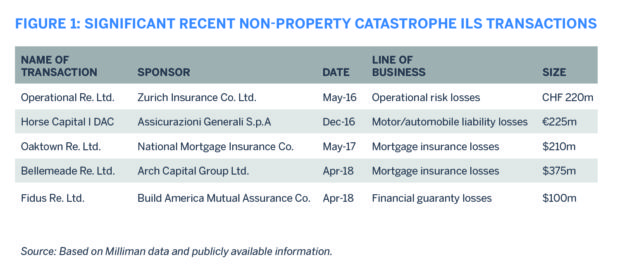

The amount of casualty-related ILS issuances have been on the rise in the past several years, with 2018 already shaping up as the largest year to date. Recent transactions cover a relatively broad range of lines of business—from traditional casualty lines, such as auto liability, to financial-related lines, including guaranty and mortgage credit risk. Several recent examples of transactions are shown in the table below.

It is also worth noting what is not included in the above list: most notably, cyber insurance, longer-tailed lines of standard casualty business, such as general liability, and “casualty cat” covers that aim to protect against future industry events similar to the asbestos or pollution crises of the past.

It is also worth noting what is not included in the above list: most notably, cyber insurance, longer-tailed lines of standard casualty business, such as general liability, and “casualty cat” covers that aim to protect against future industry events similar to the asbestos or pollution crises of the past.

Casualty ILS is a market still in the relatively early stages of evolution, with several key questions to be addressed before we are likely to see a prevalence of such types of risk:

- Are the economics of casualty risk appealing to alternative capital investors?

- Can casualty risk be modeled to the degree of detail and insight expected by alternative capital investors?

- Can a casualty ILS product offering be designed to meet the operational needs of both cedents and alternative capital investors?

We’ll now look at each one of these questions to identify where recent transactions have laid out the potential path to a broader casualty ILS market—and in turn, where more product refinement still may be needed.

Are the Economics of Casualty ILS Sound?

Of the three key questions, this is perhaps the one that is most crucial: If casualty risk is not an appealing investment opportunity for alternative capital providers, then all of the modeling tools or excess capacity in the world will be irrelevant. There are at least two potential structural objections to casualty ILS that historically have been raised on this basis.

The first objection is that casualty ILS might be significantly more correlated with the broader financial markets than property catastrophe ILS. Will investors be interested in adding risk to their portfolio that conflicts with the “zero-correlation” assumption that helped make ILS appealing in the first place?

The presence of several recent mortgage insurance transactions indicates that certain investors are willing to supplement their portfolios with potential risk that is correlated with the broader performance of the economy, at least in small quantities.

The presence of several recent mortgage insurance transactions indicates that certain investors are willing to supplement their portfolios with potential risk that is correlated with the broader performance of the economy, at least in small quantities.

Similar challenges will exist for a range of potential future casualty perils. For instance, it is evident how a truly major, multicompany cyber catastrophe could have an impact on the financial markets. The most likely outcome may be that we see a bifurcation among alternative capital investment funds. Some will choose to keep focus on the property catastrophe space, while others will build the analytical capacity and knowledge base to expand their offerings and provide a market for non-property risks.

Some funds will even choose to do both, offering peak peril-focused portfolios to investors who prefer that risk and more diverse reinsurance opportunities to investors with a broader risk appetite.

The second objection to casualty ILS is that the casualty reinsurance market might not be subject to the same types of underlying capital constraints as those caused by peak natural perils. This would imply that the spreads for casualty ILS will fall short of the returns that drove the growth of the natural catastrophe market and thus prove unappealing to financial markets investors.

In one sense, this is unquestionably true. Margins in the casualty market will likely never reach the returns historically available in the cat bond market. However, the strongest of these past returns are probably artifacts of the past for property catastrophe perils as well. The halcyon days when a handful of investors took advantage of a poorly known asset class are now in the past.

We already have seen how investors react when spreads on peak perils get compressed and they have additional capital on hand. They find other vectors through which to deploy their money. In the last several years, this has most often taken the form of participation in major industry quota shares, as well as investment in private collateralized deals “further down” cedents’ reinsurance towers. Both types of transaction are exposed to much smaller events than a traditional catastrophe bond. The growth of fund-related Lloyd’s syndicates and primary insurance initiatives shows much the same trend: Alternative capital is no longer solely “peak peril” capital. Indeed, capital market interest is growing in a range of risks across the whole of the reinsurance enterprise.

This, in conjunction with increasing regulatory capital pressures such as Solvency II, illustrates a potential path to economic viability for casualty ILS, even at lower margins than traditional property catastrophe business. To reach this point, however, structurers of casualty ILS deals must first develop answers to the modeling and design challenges facing this space.

Can Casualty ILS Be Sufficiently Modeled?

Compared to other alternative asset classes, one of the standout attributes of the ILS market is the extent to which its publicly traded securitizations are independently modeled, using common tools that are generally accepted across the market. Catastrophe models allow for a common framework of risk across the market and comparability across transactions that cover natural perils.

By comparison, the modeling for casualty lines is less familiar to investors. In some cases (e.g., cyber), this is because the peril itself is still at the developmental stages of modeling. In other cases, actuarial models exist for the peril (e.g., workers compensation or general liability) but are still not as familiar to investors as traditional catastrophe models.

The development or extension of these models to meet the needs of an ILS audience will be key to the success of casualty ILS. In some ways, this will be a reasonably straightforward evolution. Key metrics produced by catastrophe models such as attachment probability and expected loss can be replicated in an actuarial setting, as can scenario and sensitivity testing of the key input parameters. In this way, models for new ILS perils can “speak the language” already familiar to investors, ensuring that the focus can be on understanding the methodology employed as opposed to interpreting the format of the results.

In other matters, risk models for new classes of business will require further refinement in order to earn acceptance from the ILS investor community. Two of the biggest inherent weaknesses to casualty actuarial models, for instance, are the uncertainty associated with modeling the loss process (particularly for business with a long payment horizon) and the challenge of modeling low-frequency, severe “tail” loss outcomes.

It should be expected that investors will be cautious to embrace these models. After all, it was traditional insurance models’ weaknesses in tail modeling that led to the birth and success of the catastrophe model industry and with it ILS. However, in a maturing market where investors have begun to consider the 1-in-10-year risk alongside the 1-in-100, the expansion of the set of useful ILS models should be expected.

If nothing else, the events of 2017 (and the enormous variations in initial modeled loss estimates provided by catastrophe modelers for certain storms) should give the industry reason to reassess the amount of uncertainty in the models with which they already are familiar. It is possible that the move to modeling new classes of business will not prove as much a leap into the unknown as first expected, when compared to the uncertainty inherent in the existing models on which ILS has built its foundation.

Can Product Design Challenges Be Overcome?

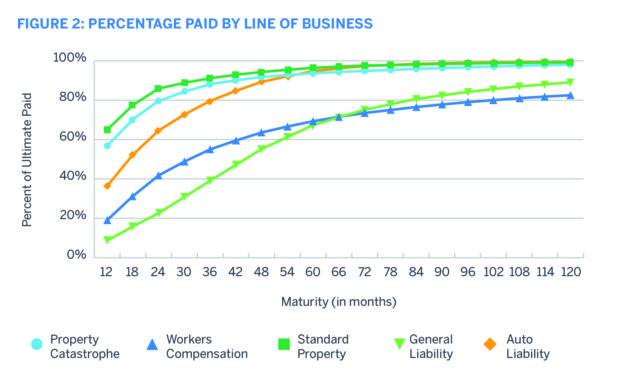

Operationally, casualty business is fundamentally different from property business—the significant (albeit declining) market presence of property-focused reinsurers attests to that. For ILS, perhaps the most important difference is the increased length of time it takes before casualty losses can be reliably estimated and then paid, as shown below.

The differences are stark. When a given set of losses has matured for three years, over 90 percent of property losses will be paid but less than half of the general liability losses will be paid. This even sets aside the fact that for catastrophic liability events, such as asbestos or a series of major explosions, the true scope and nature of liability in the excess layers may not become apparent for a decade or significantly more in some cases.

The differences are stark. When a given set of losses has matured for three years, over 90 percent of property losses will be paid but less than half of the general liability losses will be paid. This even sets aside the fact that for catastrophic liability events, such as asbestos or a series of major explosions, the true scope and nature of liability in the excess layers may not become apparent for a decade or significantly more in some cases.

This fundamentally clashes with the time horizons of ILS investors as currently understood by the industry. Setting aside the liquidity associated with publicly traded cat bonds, even investors who “buy and hold” can generally expect to receive closure on a loss within a reasonable time frame (say three to four years) after the loss occurrence. Even this length of time has rarely needed to be utilized in the past due to the lack of ILS claim activity, and it will be instructive to monitor investors’ reactions to the claim development process for the 2017 events.

For longer loss horizons, a rated balance sheet historically has been the preferred tool. There are two things worth noting:

- Several ILS managers already have begun to set up affiliated rated balance sheets to write risk. This not only makes certain aspects of existing deals (e.g., reinstatements) easier to handle but also provides them with a platform to eventually take long-tailed and runoff risk. At that point, it becomes a matter of matching certain tenors of risk to the vehicles best suited to handle them.

- Other participants in the reinsurance markets specialize in taking runoff risks, including some like Berkshire Hathaway, which focus on sizable longer-tail liabilities that no one else has the capacity to absorb.

Returning to the three-to-four-year time horizon, to securitize casualty risks, instruments will need to innovate on the existing ILS loss settlement process. Currently, commutation clauses focus on reaching a final settlement between the original ceding party and investor. It is clear that very few casualty cedents would be interested in a cover that would return so much uncertainty to them at the end of the extension period.

One potential option is to settle based on a loss index of some sort. However, the examples of casualty ILS to date have focused on indemnity triggers that pay based on a cedent’s actual losses, and it is not clear whether the potential benefits provided by an index are worth taking on the additional basis risk of an index transaction for cedents.

Instead, perhaps the challenge is to find an economical way to bring two sets of investors to the original transaction—one to accept risk for the length of a reasonably standard ILS transaction, and another whose participation is contingent on the occurrence of a loss event—and then offer their backing to absorb the runoff of the payment stream for an appropriate price.

While the details will necessarily vary, building such a “runoff agent” into a transaction from the beginning has two major benefits: Not only does it avoid having to find a runoff partner down the road in a distressed loss scenario, but it also allows for spreading a potentially sizable commutation risk margin over a broad number of transactions, the majority of which will never require runoff.

After developing such a clause, we can then differentiate between perils where the loss is likely inestimable within the three-to-four-year time frame and perils where loss estimation is possible but characterized by high uncertainty. Examples of the former are likely to include asbestos-like exposures, while the latter might represent a more stable book of business and reserve development on lines such as general or professional liability. The latter scenario offers significantly more optimism for viable transactions relying on some form of third-party commutation.

Overall, the challenges facing casualty ILS are real but not insurmountable. For the next few years, the path to success may involve defining which types of casualty risks are most palatable to the end investor.

To this end, financial-related risks such as guaranty and mortgage insurance have shown appeal, as have shorter-tailed casualty lines such as auto liability. With each additional transaction that comes to market, the path is being laid for future incremental development. On this basis, the next stage of the ILS markets can be built.

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns

Insurers Are ‘Actively Evaluating’ New Catastrophe Risks as Europe Burns  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry