In the industrial age, nothing made more progress toward efficiency than the assembly line. In 1913, in a back corner of the Ford automotive factory in Highland Park, Michigan, a test was underway. Before Ford would employ conveyor belts for many different operations, they practiced on the magneto — an electrical device that provided sparks to each of the Model T’s four cylinders. Assembly time for the magneto went from 20 minutes to under 5 minutes — setting the stage for a completely new type of scalable manufacturing process.[i]

One year later, Ford doubled employee salaries and cut work hours, surmising that this move would make the workforce itself more productive. It did.

The three changes — technology, conveyors (process) and wages — seemingly have nothing in common, yet we now know that there is an inextricable link between people, process and technology — that no matter what industry you are in, people, process and technology contribute to efficiency and satisfaction. This is how and why AI, Agentic AI, and Generative AI (GenAI) implementation needs a people-first approach. AI-driven insurance solutions aren’t just technologies to be implemented in a vacuum or a black box. It is creating a new process (conveyor) and an intelligent facilitator where human touchpoints still matter.

AI solutions to streamline insurance business operations and processes across industries, ultimately redefine what is possible in terms of speed, scale, operational efficiencies, reduced costs, and strategic decision-making. Organizations are embedding GenAI and Agentic AI into their operations to automate and streamline workflows, improve employee productivity, enhance customer engagement, drive down operational costs, and improve profitability and competitive pricing and market positioning. Insurance AI solutions is the transformative technology of our lifetimes.

Today, L&AH insurers are facing pressure from multiple fronts. The cost of insurance has increased; the cost of claims, particularly for A&H products, has gone up. The inefficiencies of legacy systems have created productivity and customer service challenges, and overall operational costs have increased, leading to higher expense ratios and less competitive pricing for products. Plus, hiring and keeping good talent can be a struggle in a culture where 50% of employees are “watching for or actively seeking a new job.”[ii]

Majesco’s recent Thought Leadership, A Powerful Chain Reaction: The Financial and Operational Impact of GenAI and Agentic AI Across the Insurance Value Chain, outlines how insurers must set forth a strategy to capture the full value of AI—GenAI and Agentic AI—across the entire business operation to achieve cost efficiencies and productivity that will drive down expense ratios and improve human efficiency and satisfaction. To help insurers envision real-life applications of AI insurance solutions, use cases and benchmarks are given for L&AH that can be used to assess the business value and impact for your organization.

Though the overall goal was to paint a holistic portrait of AI and GenAI for insurance, Majesco dived into detailed task samplings within departments, such as Product, Quote, Underwriting, Issue, Servicing, Billing and Claims. You’ll find these benchmarked tasks within the report.

L&AH Growth and Profitability — State of the Market

The U.S. L&AH insurance market posted strong top-line growth in 2024 but continued to struggle with rising operating costs and pressure on profitability. While total direct written premiums grew by 16.6% to $1.4 trillion, it was led by an 18.6% surge in annuities and only 4.7% for life.[iii]

For group and benefits, increased medical and healthcare costs have led to higher claims costs for some products and impacted enrollment for other voluntary or supplemental products due to rising costs for medical insurance, exacerbated by the impact of inflation on employees’ finances. In addition, the rapidly changing demographics of employees are shifting the focus to worksite and individual products that meet people’s changing behaviors and needs as they move between jobs.

Overall, total expenses rose 14.7%, driven by higher surrenders, benefits, and operating costs. Pretax operating income dropped 27.8%, and net income declined 13.3% to $33.3 billion.[iv] Return on equity fell to 4.6% from 6.2% the prior year, reinforcing the pressure on margins.[v]

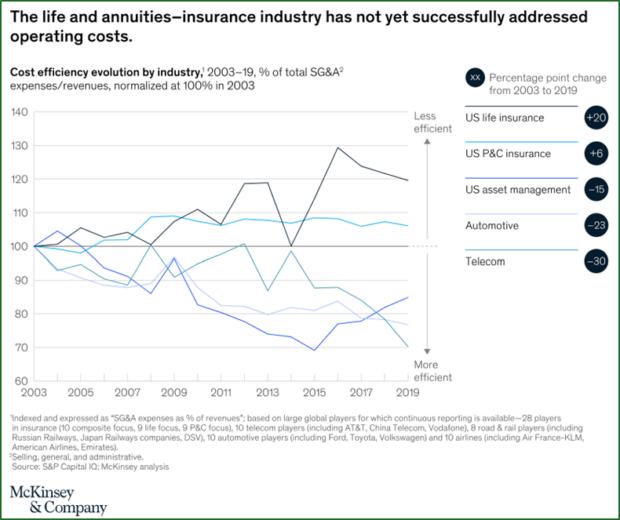

Unfortunately, the L&AH segment has lagged in managing operating expenses – heavily influenced by the lack of business transformation and legacy replacement. A 2021 McKinsey article noted that many L&AH carriers missed earlier waves of cost transformation, relying on legacy systems, manual processes, and fragmented distribution models. This long-standing gap in modernization is now impacting L&AH insurers’ operating costs, productivity and overall financials as seen in Figure 1.[vi]

Figure 1: L&A industry’s relative historical cost efficiency (McKinsey & Company)

There is a heightened urgency to close the operational and technology gap. Future profitability and market competitiveness depend on whether the industry can break from its historical inertia and aggressively modernize its business operating model and cost structure.

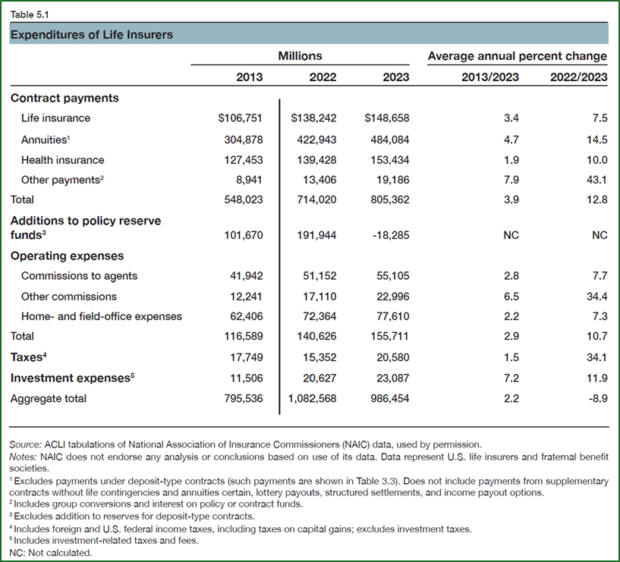

Operating expenses of life insurance companies include commissions to agents, other commissions, and home- and field-office expenses. In 2023, home and field-office expenses represented 49.8% of operating expenses, as shown in Figure 2.[vii]

Figure 2: Life insurer expense categories

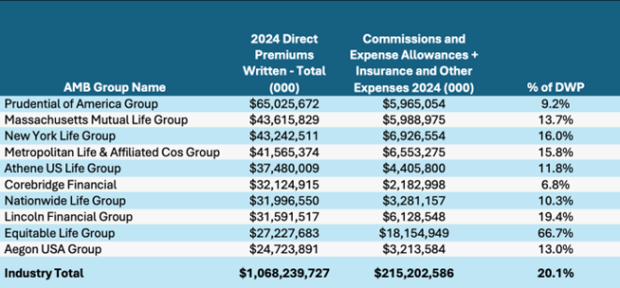

In looking at the top 10 AM Best L&AH groups based on premiums for 2024, there is significant room for improvement in expenses as a percentage of DWP. (SeeTable 1)

Table 1: 2024 Expenses as percentage of DPW by AM Best Top 10 L&AH DWP Groups

Sources: AM Best BestLink data, First Look: 2024 US Life/Annuity Financial Results

Sources: AM Best BestLink data, First Look: 2024 US Life/Annuity Financial Results

L&AH Market Leaders

Leveraging GenAI and Agentic AI solutions for L&AH insurance throughout the entire value chain equips insurers with enhanced operational capabilities, consistency, and quality that can deliver greater business value and customer satisfaction. By accelerating claims, service, underwriting, and quoting processes, these advanced technologies allow insurers to accomplish more with existing staff, respond to rising demand, and prioritize submissions more effectively, driving new levels of efficiency and profitability. At the same time, insurers face mounting pressure to meet the evolving digital and insurance expectations of an employee base increasingly dominated by Millennials and Gen Z—segments that will not work with legacy systems.

Once again, success requires leadership and the willingness to rethink the business. We see these key characteristics of AI and GenAI Leaders:

- Concentrate on core business processes (underwriting, policy, billing, claims) for competitive advantage.

- Emphasize people and processes over technology to rethink the business.

- Move beyond operational productivity to revenue, profitability, and employee empowerment.

- Invest strategically in key areas to scale and maximize AI, GenAI and Agentic AI value, advancing broader investment across the value chain.

L&AH Future State with AI, GenAI and Agentic AI Operational Impact

The L&AH insurance value chain has broad opportunities to leverage AI, GenAI and Agentic AI in game-changing ways. Majesco is leading the industry in the use of AI, GenAI and Agentic AI embedded in all our solutions across the insurance value chain to create a new era of operational excellence, addressing the decades-old issue of operational inertia.

The L&AH sector is ripe for streamlining operations, reducing expenses, and improving cycle times across the insurance value chain. It is especially valuable in an environment where product complexity, administrative burden, employee expectations, and customer expectations continue to rise.

Majesco Copilot — Majesco’s “on board” AI — is available on every screen of our solutions, providing the ability for users to ask basic questions such as how to do a transaction, summarize information, draft a reply and more. These general capabilities leverage the embedded online documentation and data within the system.

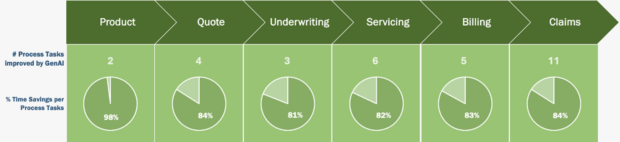

In addition, Majesco has developed more in-depth capabilities that go beyond the ability to provide transactional guidance, summarize information and accelerate routine administrative tasks, by assisting in actionable tasks and transactions. Figure 3 highlights the high-level L&AH value chain with the number of current use cases for these actionable tasks and their average time savings within each process. Each of the use cases has been benchmarked with and without GenAI or Agentic AI for actual time savings.

Figure 3: Number of Current GenAI-Aided Use Cases and Average Time Savings: L&AH

Because each company’s business is different in terms of products, organizational structure, jobs and business volume, we have estimated the time savings per task with an illustrative “hours saved” per day and per year based on an assumed number of tasks each day. Each company can estimate their specific time savings based on their business and then correlate that to the cost per hour for that role to calculate the ROI business value potential.

Based on the details provided below for each high-level core business process and illustrative examples, an insurance company using Majesco’s L&AH Intelligent Core with the current use cases based on a single transaction and user could save 35,031 hours per year. Assuming an average workable time annually of 1,700 hours per person and an average salary of $70,000, the baseline (one person per use case) would save the time of 21 people at $1,442,439 across the value chain.

More importantly, this baseline would substantially increase when applied to the true number of people, the number of tasks performed daily and their actual salaries, raising the potential savings well into the six and seven-figure range for many companies. Depending on the company, it is not unrealistic to consider a minimum of 2% – 5% impact on the expense ratio – either through reduction of cost or by processing more at the same level of staffing.

The business value and impact is real. To see the time reduction detail on the specific L&AH tasks, be sure to download the report.

Finding the right approach

A recent McKinsey article asserts that with GenAI, companies can generate intelligence at scale. GenAI’s ability to reason and make autonomous decisions means it can extract insights from data and then turn those insights into action directly within business workflows—enabling the data-driven enterprise of the future.

For insurers, this requires new operating models that are AI and data-driven have the opportunity to leverage the full value of GenAI and Agentic AI in L&AH insurance, creating value across the entire value chain that can accumulate significant ROI in terms of time savings that can drive down expense ratios, which in turn can improve profitability and market competitiveness with pricing that can take advantage of lower costs.

The undesirable alternative is to implement one-off solutions for GenAI and Agentic AI. This limits the potential operational impact.

Instead, insurers must look at GenAI and Agentic AI as catalysts for enterprise-wide transformation and operational optimization. Every operational activity in insurance can be augmented with Agentic AI. GenAI and Agentic AI value compounds over time as insurers embed them into more workflows across the entire value chain, extending business value beyond time and cost savings to include improved decision quality, faster innovation, employee satisfaction, and stronger customer loyalty.

To fully capture the full advantage of AI, insurers must begin with a clear roadmap and the right solution partner who is investing in the core solutions that will deliver broader value. The roadmap would include high-impact use cases where AI can drive immediate value—such as quote and underwriting automation, and enhanced customer service. These early tests and wins create momentum, provide critical learning experiences, and address fear or concerns about the technology. They pave the way for new ways of working and thinking.

Are you ready for a new business model and technologies that dramatically improve cost ratios as they make better use of your vital talent resources? Be sure to download and read Majesco’s Thought Leadership report, A Powerful Chain Reaction: The Financial and Operational Impact of GenAI and Agentic AI Across the Insurance Value Chain, and be sure to watch Majesco’s webinar, 2026 Trends Vital to Compete and Accelerate Growth in a New Era of Intelligent Insurance.

[i] Davis, Wed, American Journey: On the Road with Henry Ford, Thomas Edison and John Burroughs, p. 20, 2023, W.W. Norton & Co.

[ii] Gallup, State of the Global Workplace 2025: Understanding Employees, Informing Leaders, p. 23, May 2, 2025

[iii] “U.S. Life and A&H Insurance Industry Analysis Report 2024,” NAIC

[iv] Coppola, Matthew, “First Look-First Look-2024 US Life/Annuity Financial Results,” AM Best, April 2, 2025

[v] NAIC, op. cit.

[vi] D’Amico, Alex, et al, “The productivity imperative for US life and annuities carriers,” McKinsey & Company, March 16, 2021, https://www.mckinsey.com/industries/financial-services/our-insights/the-productivity-imperative-for-us-life-and-annuities-carriers

[vii] “Life Insurers Fact Book 2024,” American Council of Life Insurers, https://www.acli.com/-/media/public/pdf/news-and-analysis/publications-and-research/2024-fact-book/pub_2024aclifactbook_complete.pdf

Cyber Insurance Market Faces Pressure as Claims Severity Climbs

Cyber Insurance Market Faces Pressure as Claims Severity Climbs  Progressive Is Biggest Auto Insurer, Surpassing State Farm: S&P GMI

Progressive Is Biggest Auto Insurer, Surpassing State Farm: S&P GMI  With Customer Reviews Increasingly Polarized, Communication Is Key: Trustpilot

With Customer Reviews Increasingly Polarized, Communication Is Key: Trustpilot  Executive Viewpoint: What Telematics Got Wrong and What It Means for Commercial Auto

Executive Viewpoint: What Telematics Got Wrong and What It Means for Commercial Auto