As we head into 2024, many property/casualty companies are primed to grow their businesses, but not all have adequate levels of surplus to support premium growth, an Aon Ward executive said during a mid-December webinar.

Jeff Rieder, partner and head of Ward Benchmarking, noted that many organizations in the U.S. P/C insurance industry recovered nearly all of their policyholder surplus—”and then some”—during the first half of 2023 after a down year in 2022. But by the end of the third quarter of 2023, surplus levels had fallen back down to where they were at the beginning of the year, he said.

Speaking at Aon’s U.S. P/C Performance Outlook webinar in late December, Rieder said Aon is estimating just a 1-2 percent decline in overall policyholder surplus through the first nine months of 2023 industrywide but added that more significant individual dips will particularly challenge many smaller organizations that “have lost more surplus than perhaps they’re able to withstand.”

“By rough estimates, about 15 percent of the U.S. P/C industry is being affected by severely detrimental surplus conditions,” Rieder said.

“Some companies are growing [premiums] at levels that are far greater than they’re able to grow their surplus,” he said.

Through third-quarter 2023, about 170 U.S. carriers are operating with 20 percent less surplus than they began with in 2021, he said. Of those, 103 had lost more than 30 percent of the surplus they had at the beginning of 2021 by the end of third-quarter 2023.

Through third-quarter 2023, roughly 170 U.S. carriers are operating with 20 percent less surplus than they began with in 2021.

And just in 2023, over 30 carriers lost 30 percent—or more—of their surplus since the beginning of the year.

(Editor’s Note: A previous version of this article incorrectly stated that 30 percent of carriers lost 30 percent of their surplus in 2023. The correct figure is roughly 30 carriers.)

“This will certainly have a big impact, and we want to recognize that that’s going to challenge companies in terms of how they’re approaching 2024 and beyond,” Rieder said during a portion of the webinar devoted to a review of key performance metrics. During the rest of the webinar, Rieder and Charlie Gall, associate partner and Ward P/C practice leader, also reviewed inflation trends, insurance labor trends and AI usage trends in the insurance industry.

Rieder and other analysts from AM Best, Standard & Poor’s and Fitch presented industry outlooks in December last year and early this year, highlighting personal lines challenges—not just in auto but in homeowners lines—and the impacts of severe convective storm losses, changing reinsurance appetites and one component of inflation, elevated shelter costs, on carrier results.

Toward the end of the webinar, Rieder stressed that the financial position of the industry as a whole still remains very strong. “With a favorable fourth quarter here, we still have a chance to get back to over a trillion [dollars] in total policyholder surplus,” he said, referring to the industrywide total at midyear 2023.

“But I don’t want to minimize the impact [of financial challenges] on many particularly personal lines-focused organizations…Several have gone into rehabilitation or liquidation, and we’re seeing many that are dealing with surplus positions that are in some cases half of what they were at the beginning of the year,” Rieder said.

“There will be some organizations that will be certainly stressed. The volatility of losses and rising cost of reinsurance and inability to get adequate rate is going to certainly stress the financial strength of those organizations,” he said.

At one point, Rieder displayed a bar graph showing global insured catastrophe losses which impacted property insurers, split between primary perils, shown in green, and secondary perils in gray. The bar for the year 2023 through the end of October, indicating a $92 billion total, was almost completely gray, indicating that convective storms, wildfire and winter weather were the bulk of the 2023 loss total—a stark comparison to any of the prior eight years. A note on the graph indicated that $55 billion of the $92 billion—60 percent of the total—represented U.S. insured convective storm losses.

Midwest Suffers

While much has been written about troubles on the coasts in 2022 and 2023—in California and Florida—Tim Zawacki, principal insurance analyst, S&P Global Market Intelligence, brought the focus to the middle of the country during S&P’s early December webinar, “IN/sights: Outlook and Trends for U.S. Insurers—What to Expect in 2024 and Beyond.”

“What we’re seeing in recent years is that the severity and the impact on the industry of convective storms, which are not as bound by geography as hurricane and wildfire, has perhaps changed the thinking [about] states like Iowa, South Dakota, Wisconsin,” said Zawacki, highlighting the high property insurance loss ratios for insurers that fueled reinsurance industry responses and eventually depleted surplus positions.

“You’re seeing reinsurers become more reluctant or not at all willing to write business for companies that are heavily concentrated in the upper Midwest,” he said. “We’re seeing in Wisconsin, in particular, the town mutual model that’s existed for 150 years really get washed under in this fallout from the reinsurance market just not having the appetite to be so geographically concentrated among cedents that may have small balance sheets,” he said.

Zawacki has written a number of articles on the S&P GMI website detailing problems in the Midwest, including one article about the impacts of 2022 and 2023 storms on Wisconsin Re, a reinsurer of Midwest town and county mutuals now in rehabilitation, and another article on the decision of Wisconsin-based SECURA Insurance to exit the personal lines market—a move Zawacki suggested other carriers squeezed by rising costs and rising cat losses would follow.

In a separate article published by our sister website, Insurance Journal, Jerry Theodorou, director of the Finance, Insurance and Trade Policy Program for R Street Institute, who is a former director of Insurance Research for Conning, described the convective-storm driven troubles of Wisconsin Re and a half-dozen Midwest carriers either in rehabilitation, liquidations or receivership or experiencing surplus declines of 40 percent or more. (Related article: On Tolstoy and Insurance Troubles in the Heartland)

Rating agency AM Best reacted to the surplus hits at two of them, Badger Mutual Insurance Company and Germania Farm Mutual Insurance Association, with ratings downgrades, pushing Milwaukee, Wis.-based Badger’s financial strength rating to C++ (marginal) from B+ (good) in October last year, and Texas-based Germania’s down to B (fair) from B++ (good) in August.

During an AM Best Outlook briefing in mid-December, Director Joseph Burtone explained AM Best’s negative rating outlook on personal lines generally, pointing to elevated storm losses and the ramifications of a hard reinsurance market. “We are seeing retention levels that we have never seen before in all my years that I’ve been here,” he said, referring to reinsurance program structures that force primary carriers must to keep convective storm losses net. “These retention levels are getting to be in excess of 15-20 percent of surplus.”

“These types of losses are death by a thousand cuts for insurance companies, as in most cases these companies are taking those losses from dollar one due to the higher retention levels on their reinsurance programs.”

While Burtone pointed to solid risk-adjusted capitalization levels for most carriers as one of the few bright spots on the outlook for personal lines, persistent underwriting losses have eroded capital cushions of some previously strong carriers, he noted, echoing Rieder. “Some companies that have historically reported excess capitalization have seen adjusted levels decline materially through a combination of underwriting losses, changes to reinsurance structures and increased reserves amid the inflationary environment.”

Responding to a later question posed by Chief Rating Officer Stefan Holzberger, specifically about the impact of tight reinsurance conditions, Burtone said: “It’s been very hard. Operating performance is suffering” as a result of reinsurance program changes. “And when the operating performance is suffering, the companies are usually losing surplus. And when you lose surplus, you’re generally reducing overall risk-adjusted capitalization. There’s pressure on those blocks,” he said, referring to the building blocks of financial strength ratings.

“This is some of the best underwriting I’ve seen…”But [with] all that goes on from an inflation perspective, a weather perspective, it’s hard to see the benefits.”

“It’s been very difficult for the companies… They’re doing a lot,” he said. “This is some of the best underwriting I’ve seen through all the years that I’ve been here from when I started,” he said, noting that personal lines companies are trying to counter the challenges they face with technology, predictive analytics and data. “But [with] all that goes on from an inflation perspective, a weather perspective, it’s hard to see the benefits of all that underwriting,” he said.

Holzberger noted that beyond balance sheet strength and operating performance, the next rating building block—business profile—might come into play as carriers try to “right-size their books of business and manage exposure.”

(The rating agency’s business profile assessments look at factors such as product and geographic concentration, market position, pricing sophistication and data quality, among others.)

Burtone agreed. “Companies that are managing their business profile well are companies that usually generate solid operating results. Companies that generate solid operating results,…usually generate organic surplus growth. So, [the blocks] build on each other the other way,” Burtone said.

“What we’re seeing is [for] these companies that [are] not managing that business profile, especially the single-state or the two-state writers with product concentration, it’s much more difficult to manage that [operating performance] as successfully as it was a couple of years ago,” Burtone said.

Concluded Holzberger, “Operating performance and business profile are leading indicators of future balance sheet strength,” repeating a fact he said is communicated regularly to AM Best rating agency analysts by their chief executive officer, Matthew Mosher.

Addressing Business Profiles

During the Aon Ward event, Rieder described how carriers are working to improve business profiles.

“In the last three or four years, a lot of our discussions were about how companies were going to expand their products and geographic footprint. Now we’re seeing a reverse of those engines…Companies are continuing to evaluate their product and geographic portfolio, which means that we’re going to see companies continue to rebalance and focus on their more powerful and more sustainable lines,” he said.

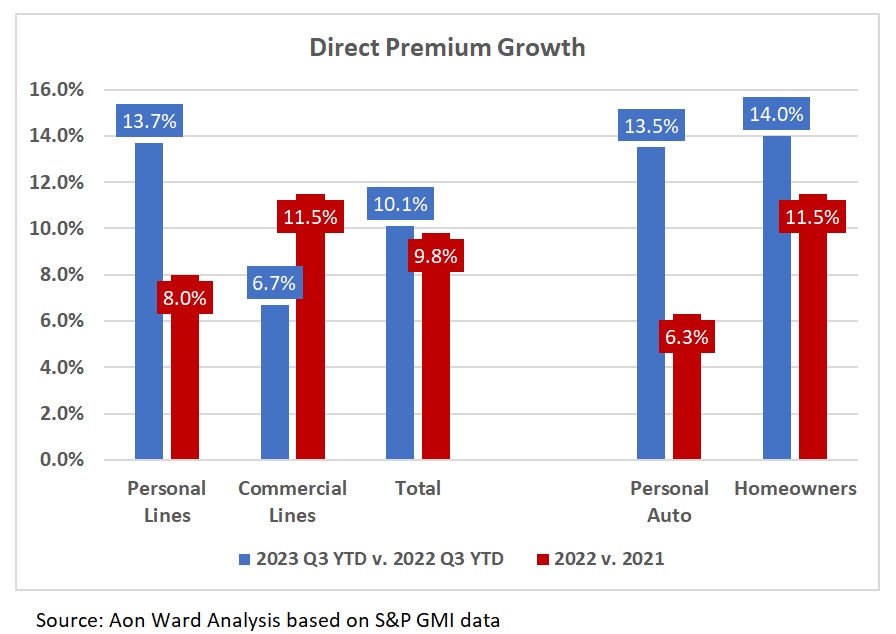

Rieder showed slides displaying premium growth by line and by state, highlighting shifts in portfolios away from personal lines toward better-performing commercial lines, the growth in commercial lines E&S premiums, and he also talked about anticipated moves to the E&S market for personal lines business. He then displayed direct loss ratios by line and by state, revealing that premium hikes in challenged personal auto and homeowners lines did not improve loss ratios.

Key takeaways:

- In 2020, commercial lines premiums overtook premiums from personal lines and has remained higher than personal lines through 2023.

- While the commercial lines growth trend has been favorable, it is starting to slow relative to personal lines.

- E&S premiums now comprise roughly 10 percent of U.S. total market premiums and 20-22 percent of total commercial lines.

- Ward is starting to see growth in the personal lines E&S market, particularly in states like California, Florida and Texas, where this may be a growing segment as insureds find it difficult to find coverage.

- Direct premium growth in 2023 across all lines was slightly lower in 2023 than in 2022. Through the first nine months, total premiums grew 9.8 percent compared to the first nine months of 2022. Total direct premiums for all lines grew 10.1 percent for all lines in 2022 compared to 2021.

- On a state-by-state basis, Texas, which needed a lot of premium growth to keep up with the losses generated from weather events, had the highest growth rate—at 15.9 percent for personal and commercial lines combined. In contrast, New Jersey was the only state showing a decline of about 3.8 percent, while all other states were up by at least 3.9 percent in 2023.

- Midwest states of Iowa (6.1 percent), Michigan (6.8 percent), Wisconsin (7.8 percent), South Dakota (7.7 percent) and Illinois (8.0 percent) had growth rates below the 10.1 percent national average, as did profit-challenged California, where a 6.2 percent overall growth rate ranked as the sixth-lowest state growth rate, according to Aon Ward.

- In spite of premium growth, 2023 direct loss ratios through nine months came in almost identical to nine-month loss ratios in 2022 for every line except homeowners and commercial auto. For all lines combined, the loss ratio was 68 in both years..

- The homeowners direct loss ratio came in five points higher in 2023 through nine months (82 vs 77 for 2022 through nine months), and the commercial auto loss ratio rose four points (to 73 from 69)

- Tracking loss ratio changes by state, Aon Ward revealed that California and states in the middle of the country, including Iowa, Illinois, Michigan, Ohio, Arkansas and Tennessee, experienced direct loss ratio increases between 5 and 10 points through the first nine months of 2023. Oklahoma, Kansas, Mississippi and Kentucky saw loss ratio increases in excess of 10 points.

Rieder also said that industry combined ratio for 2023 is likely to be slightly higher than the 102.4 registered in 2022 when underwriting results are tallied in the next few months.

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’

UN, Scientists Warn Strong El Niño Will Add Fuel to ‘Planet Already on Fire’  Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t