Directors and officers liability insurance premium rate hikes have not had the anticipated impacts on loss ratios that carriers had hoped for, AM Best reported Monday, citing the impact of social inflation on rising claims and defense costs.

Separately, in mid-January, Kevin LaCroix, the author of the D&O Diary blog, noted that regular economic inflation—in particular, the trio of supply chain disruption, labor shortages and economic inflation—has started to contribute to a new wave of securities lawsuits.

And while both the AM Best analysts and LaCroix have noted the federal securities class actions dropped in 2021, offering slightly different interpretations of the data, they agree that risk factors like climate change, discrimination cases, and growing cyber exposures are all contributing to new varieties of D&O insurance losses.

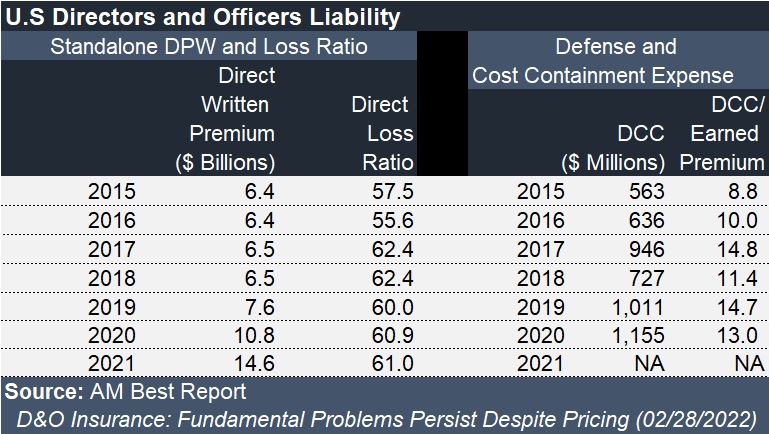

The Best report, “D&O Insurance: Fundamental Problems Persists Despite Pricing,” shows that direct premiums written for the D&O product line grown 15 percent, on average, over the last six quarters, and that $14.6 billion of premium estimated for 2021 (annualized based on a nine-month figure) was more than double the annual levels of around $6.5 billion that persisted from 2014-2018.

Direct loss ratios, however, after falling 2.4 points from 62.4 in 2017 and 2018 to 60 in 2019, ticked back 60.9 and 61 in 2020 and 2021, in spite of the premium jumps, according to data compiled by AM Best.

In addition, defense and cost containment expenses (DCC) for D&O liability rose to 14.7 and 13.0 percent of earned premiums in 2019 and 2020 (2021 figures not provided), compared to levels averaging of 9.1 percent from 2011-2016.

In addition, defense and cost containment expenses (DCC) for D&O liability rose to 14.7 and 13.0 percent of earned premiums in 2019 and 2020 (2021 figures not provided), compared to levels averaging of 9.1 percent from 2011-2016.

“Whether the aggressive rate increases and higher premiums are sufficiently offsetting complex risk factors for carriers insuring D&O risks remains unclear,” the report says, noting that 2021 price increases will show up in earned premiums in 2022, revealing more of the story about price adequacy and D&O profitability.

Why Did Federal Securities Class Actions Drop?

LaCroix tallied 210 federal court securities class action lawsuits filed in 2021, representing a 34 percent decline from the 320 in 2020, and a 48 percent drop when measured against an average annual number of 405 for the 2017-2019 period.

The biggest factor contributing to the decline, he said, was a decrease in the number of federal court merger objection class action lawsuits. Dropping those out of the comparison, LaCroix counted 192 “traditional” securities suit filings in 2021, representing only about an 11.9 percent decline from the 218 traditional filings in 2020.

“The filing levels in 2021 simply returned to long-term historical levels, compared to the artificially elevated levels that prevailed during the 2017-2020 period,” he said, adding that plaintiffs’ lawyers are still filing merger objection lawsuits–but now as individual actions rather than as class actions.

AM Best points to the U.S. Supreme Court’s March 2018 decision in Cyan Inc. v. Beaver Country Employees Retirement Fund as a factor in the decline of securities class action filings and a rise in the number of state court class action suits. In Cyan, the Supreme Court ruled that IPO-related lawsuits filed under Section 11 of the Securities Act of 1933 could be brought in all state courts.

“Cases may be complicated in more difficult to defend in state courts, which could further increase DCC costs,” AM Best said.

Referring specifically to the increase in DCC, mainly for legal expenses, in 2017-2019, the report notes the high levels of federal securities class actions in those years (which have since fallen). The AM Best analysts concede that the exact cause of the rise in DCC isn’t clear without more detailed claims data, suggesting greater complexity of cases may have been a driver. “What is clear is that the development on open claims is causing companies to add to their initial estimates on individual claims, which will manifest in worsening calendar years results,” the report says.

The report goes on to discuss social inflation, and the impacts of increased levels of plaintiff attorney advertising and for-profit litigation funders. But Best analysts refrain from making go-forward forecasts about social inflation trends on D&O loss and loss adjustment expense ratios. “Social inflation issues are being driven by a generations-long deterioration in the public’s trust of corporations, and making predictions about social inflation is difficult, because they are not driven by empirical evidence but by changing demographics and public perception of corporate behavior, especially with the expanding influence of social media.”

What about economic inflation and the problems the state of the economy?

LaCroix, executive vice president of specialty insurance intermediary RT ProExec, listed economic drivers of securities litigation as the No. 4 trend on a list of Top 10 D&O Stories for 2022 in a early January post on his D&O Diary blog, under the subheading, “Pandemic-Related Effects Roiling the Economy.”

Supply chain disruptions, labor supply shortages and economic inflation, he said, are second-level impacts from the coronavirus, reporting that securities lawsuits tied to a worsening economy already started emerging in 2021. “I think they will contribute to securities litigation in 2022 and beyond,” he added during a webinar about his Top 10 predictions.

Detailing the types of lawsuits that will emerge, he presented an example of a case against a maker of batteries for electric vehicles filed last year, Travis Nichols, et al. v. Romeo Power Inc., et al., which experienced supply chain issues for their battery cells. “Their battery cells were stuck somewhere on a boat out in the Pacific, and they weren’t able to maintain their production levels. And the investors allege that Romeo Power misrepresented the durability of its supply chain,” LaCroix said demonstrating the one way in which supply chain disruption is linked to the possibility of litigation.

A securities class action against a national chain of physical therapy clinics, Kevin Burbige, et al. v. ATI Physical Therapy, Inc., et al., also arose out of COVID-related economic impacts—The Great Resignation and labor supply shortages, LaCroix said. The complaint alleges that defendants failed to disclose to investors that ATI was experiencing attrition among its physical therapists and faced competition to hire replacements, as well as increased labor costs and the possibility that it could not open new clinics, among other things.

Both the Romeo Power and ATI cases also are examples of companies that were sued shortly after their companies merged with a SPAC, and both LaCroix and AM Best highlight the explosion of SPACs as a trend to watch for 2022.

“The growth in SPAC-related litigation also has played a role in the coverage and cost of D&O insurance,” said David Blades, associate director, industry research and analytics, AM Best. He added, however, that “the number of insurers in the market who are willing to write D&O coverage for SPACs has been somewhat scarce.”

Climate Change and Cyber

Returning to the impacts of changes in the economy on D&O losses, AM Best noted in its report that hiccups in the financial markets can “lead to an increase in new and creative securities class actions.”

“Any market declines due to inflation fears, potential spikes in infections owing to COVID-19 variants, and the prospect of armed conflict between Russia and the Ukraine could lead to a rise in class action filings,” the AM Best report says.

Both AM Best and LaCroix cited another supply chain disruption case—this one driving a class action against mattress maker Sleep Number (Steamfitters Local 449 Pension & Retirement Security Funds, et al. v. Sleep Number Corporation, et al.), which alleges that the company didn’t have supply chain flexibility when it experienced disruption in its supply of foam for bedding as a result of the Winter Storm Uri.

That case suggests yet another potential avenue for D&O lawsuits to LaCroix—climate-related D&O litigation. “If you pay attention to the warnings of climate change scientists, there may be increasing numbers of climate events. Certainly, we saw a number of them in 2021, the heat wave in the Pacific Northwest in the United States, the wildfires, the storms in the Midwest during the year, and the Texas winter storm. If we see more of those types of weather events, will we see more lawsuits like the Sleep Number case? Is this perhaps representative of the kind of litigation climate-related D&O litigation we might see in the future?” LaCroix asked during the webinar.

Another set of risks that AM Best analysts and LaCroix have their eyes on are growing cyber and privacy exposures. Here, LaCroix notes that the track record for plaintiff lawyers in this area was blemished by dismissals in 2021. That’s small consolation for insurers, however, since the plaintiffs’ bar has racked up some high-profile wins in the past, and will continue to file cases (“It’s just, that’s what plaintiffs’ lawyers do. Fish got to swim, birds got to fly, plaintiffs’ lawyers got to file lawsuits,” LaCroix said.)

Regulatory enforcement actions and shareholder derivative cases are also on the horizon for cyber, he said, highlighting a trend in Delaware courts sustaining claims alleging breach of the duty of oversight.

LaCroix highlighted a shareholder derivative lawsuit against the board of Solar Winds—a software company, which suffered a hack (allegedly carried out by Russia’s foreign intelligence service) that compromised nine federal agencies and hundreds of private sector companies in late 2020. In this case and others, there are “allegations relating to ‘mission critical operations,’ and [situations] where the board allegedly has disregarded ‘red flags,'” he said. These echo language in a Boeing 737 Max Air Crash derivative suit, which survived a motion to dismiss late last year, he said, citing that Boeing case as one of several Delaware cases paving the way for cybersecurity-related derivative actions with similar pleadings.

The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums