While the hard market is continuing at “a tempered pace,” with continued deceleration of price increases for many commercial insurance lines, “in Q2 we might even begin to see rate decreases,” a broker executive said.

In a video presentation published along with Willis Towers Watson’s 2022 Insurance Marketplace Realities report, Jon Drummond, Head of Broking, North America, for Willis Towers Watson, offered the second-quarter forecast for lines other than cyber and fiduciary.

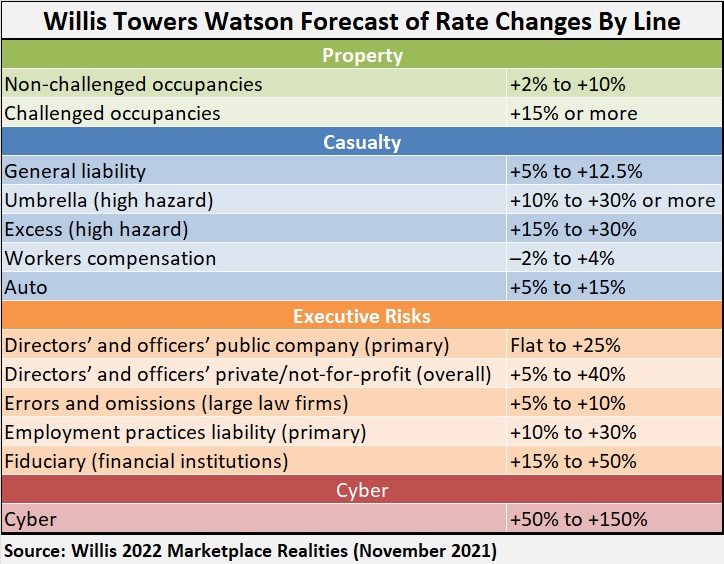

The report includes a discussion of the line-by-line forecasts summarized below:

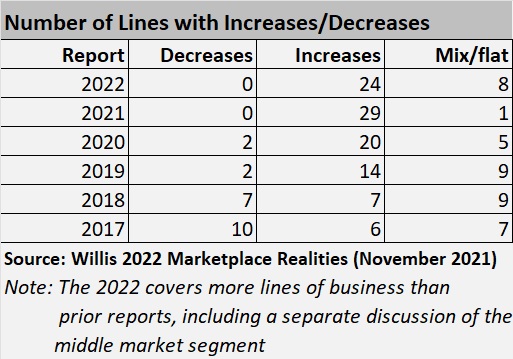

According to the Willis Towers Watson, the report marks the fourth in a row where the number of lines for which rate decreases are predicted has come in at zero. However, the number of lines for which there could be flat renewals or a mix of increases and decreases jumped from one to eight.

“The hard market continues but at a tempered pace. That’s the insurance marketplace in a nutshell and looking ahead we predict continued deceleration into 2022,” said Drummond. “As capacity comes back into the marketplace chasing market share, the law supply and demand kicks in and we see the supply do what it does best—drive down pricing,” he said.

He noted that cyber, fiduciary and high hazard risks, which are still going to see steep rate increases, as exceptions to a trend that “is turning towards buyers” in 2022.

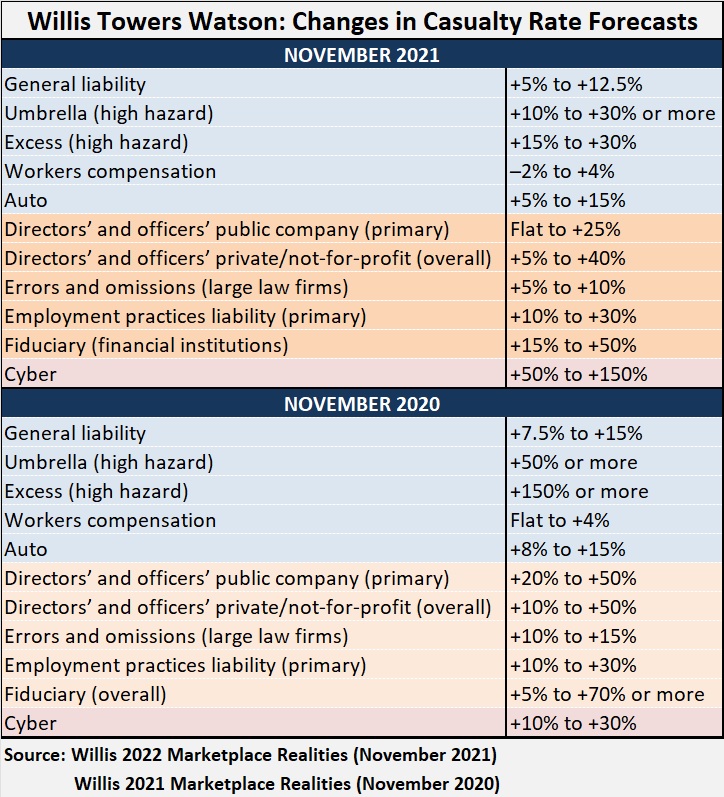

For other casualty lines, the report offers these predictions.

- General liability predictions eased modestly: +5-12.5 percent (from +7.5-15 percent).

- Auto rate forecasts similarly dropped slightly: +5-15 percent (from +8-15 percent).

- Casualty excess liability predictions are now +15-30 percent or more for high hazard risks and flat to +15 percent for low/moderate hazard.

- Workers compensation is one of the lines now looking at a mix of small decreases and increases, with a range of changes expected to extend from 2 percent declines to 4 percent increases.

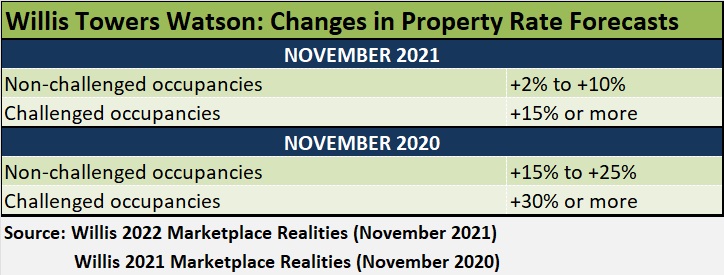

Property rate increases are decelerating, especially for better risks, according to the report. Better risks can expect increases of 2–10 percent, down from 15-25 percent last year.

For challenged occupancies, rate hikes are forecast at 15 percent or more, which represents a continuing decline in increases over recent renewal cycles.

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz