Although workers compensation results remain strong—and the line continues to outperform all other commercial insurance lines—worries about continued soft pricing and loss reserve levels for workers comp specialists prompted a rating agency warning recently.

“As rate levels continue to decline, competitive pressure could mount on [workers comp] specialists to the point that will adversely affect not only company income statements, but balance sheets as well, especially if companies are unable to set aside adequate capital for loss reserves,” AM Best analysts wrote in Best’s Market Segment Report, “Declining Rates Could Threaten Profitability of U.S. Workers’ Compensation Line,” published in late December.

The statement came in a 26-page report that sets forth historical workers comp results through 2018 for the industry overall (with some estimates for 2019), and also for workers comp specialists (including and excluding State Funds) and for State Funds alone.

Results Good For Now

The report begins with continued good news for the line, noting that not only is the line profitable—with a combined ratio of 86.1 for the latest full year available, 2018—but also that as the biggest component of commercial lines segment insurance overall, workers comp is fueling a continued stable outlook for the entire segment. AM Best’s outlook for workers comp, by itself, is stable and the “line’s favorable underwriting performance has helped offset the negative effects of other lines on the commercial lines’ overall performance,” the report says.

The 86.1 combined ratio was down nearly 6.0 points from 2017 and 15.5 points from 2014, the earliest year shown in the report. That 2018 result compares more favorably to results going back further than 2014, the report says, without projecting any estimates for 2019 or 2020.

In spite of declining premium rates in recent years, workers comp net premiums written rose 7.4 percent across the industry in 2018—marking the highest growth rate in the five years through 2018.

A robust jobs market and higher payrolls offset the insurance price drops, AM Best analysts said. The opposing forces of competitive insurance prices and higher payrolls just about offset each other, keeping direct premiums relatively flat in 2018 (with a 0.4 percent decline recorded). Net premiums still rose, however, because carriers retained more of their workers comp premium rather than ceding it to external reinsurers.

In addition to the good U.S. jobs market, key factors contributing to favorable underwriting results include:

- Low reported claims frequency

- Legislative reforms

- More effective use of data and predictive analytics

- Enhanced workplace safety measures

Potential negatives for the years ahead include:

- Medical cost inflation

- Diminishing prior accident-year loss reserve redundancies

- Higher average settlements

According to the report, medical cost inflation has not boosted loss severity to the point where it more than offsets declining claims frequency—yet.

The report also notes that “any material weakening in the U.S. economy could lead to an adverse turn in loss frequency and further pressure underwriting profits.”

Specialists at Risk?

Turning from the industrywide results for the workers comp line to analyze all-lines results for workers comp writers, AM Best analysts suggest that more problems might creep into the otherwise stable picture.

Focusing on a group of U.S. private carriers and state funds for which workers comp net premiums (including excess comp) constitute at least half of their total net property/casualty insurance premiums—AM Best’s Workers Compensation Composite (WCC)— the report notes that the WCC insurers have taken on some of the business shed by larger insurers that have refined their risk appetites, tightened underwriting guidelines, and decreased exposure to the line in recent years. In fact, the WCC increased its market share of all U.S. workers comp net premiums from 33.8 percent in 2010 to 51.7 percent in 2018. In 2018, the WCC wrote $26.4 billion of the $51.0 billion of industrywide U.S. workers comp net premiums.

The report suggests that the recent growth may fuel some negative consequences in the years to come.

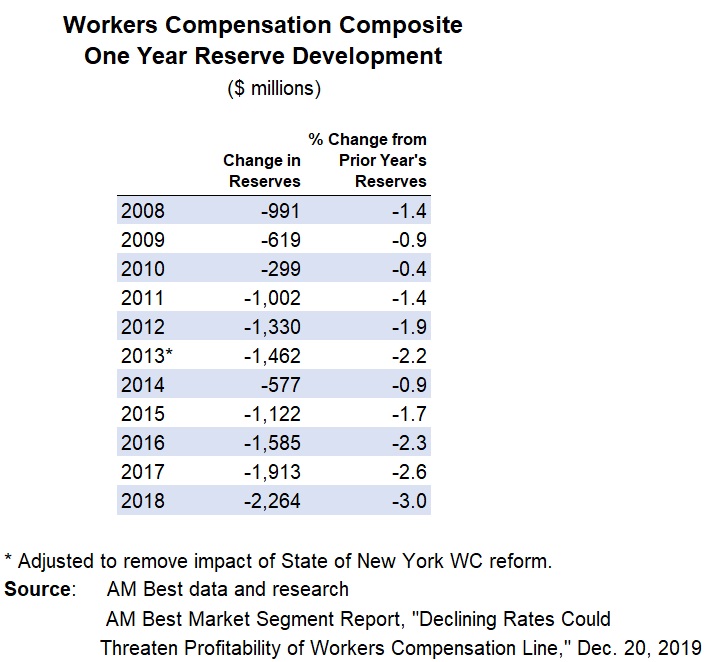

In particular, AM Best analysts note that recent underwriting profits were partly attributable to takedowns in loss reserves for prior accident years, which may not be available going forward. According to figures in the report, the WCC reported $4.6 billion in net income in 2018, driven by $940 million in underwriting profit. But the WCC had nearly $2.3 billion in favorable reserve development—the highest level recorded in 10 years.

The presence of soft workers comp market conditions “replete with consistent rate decreases in most states the last few years, future loss reserve development could prove less favorable—possibly even unfavorable,” the report said. In addition, “if the generally favorable recent year trends for claims frequency have been overestimated, or the increase in claims severity has been underestimated, the policyholders surplus accumulated in recent years could erode quickly, affecting not just the [workers comp] writers’ income statements but their balance sheets as well.”

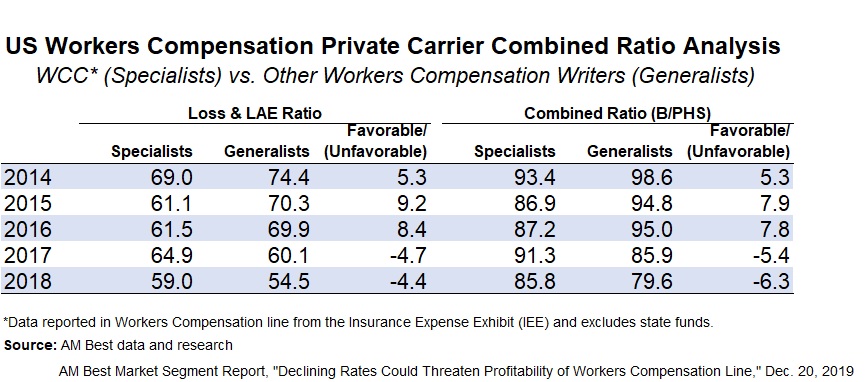

The report also analyzes premium growth and loss ratio results for just the private carriers in the WCC (WCC excluding state funds), referring to this group as workers comp “specialists” and compares their results to those of workers com “generalists”—private carriers whose comp premiums account for less than 50 percent of total writings.

While the specialists saw aggregate loss and loss adjustment expense ratios improve by 10 points of the five-year period from 2014 through 2018, for generalists, the improvement was nearly 20 points. As a result, aggregate loss ratios and combined ratios for generalists were 4-6 points better than specialists in both 2017 and 2018, the report notes. The reverse had been true in 2014-2016, when specialists had a loss ratio advantage of anywhere from 5-9 points.

Postulating some reasons for the change, AM Best analysts suggest that the larger generalists writing comp may have shrunk their portfolios slightly due to higher market competition and the difficulty of writing the coverage profitably.

“How much more profit margins will narrow and whether risk pricing will start to rise in response remains to be seen—especially if the specialists find their bottom line profitability threatened to a degree that calls for a change in strategy,” the report says.

Parenthetically, the report notes that the improvement for generalists in 2017 and 2018 is partly attributable to a changes in reserve development at AIG. In 2016, AIG had almost $1.0 billion in adverse workers comp prior year reserve development, which reversed to more than $1.3 billion in favorable development in 2017, followed by another $877 million in favorable development in 2018, the report indicates.

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry

Business Uncertainty Drives Changes in C-Suite Strategy: Sentry  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz  Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs