Since reinsurance costs are ultimately a substitute for direct costs of capital, we can better understand the ratemaking process in California by understanding how companies are allowed to incorporate cost of capital into their rate filing support.

California Code of Regulations (CCR), Title 10, Section 2644.16–Catastrophe Adjustment provides guidance on the maximum and minimum permitted after-tax rate of return on capital as follows:

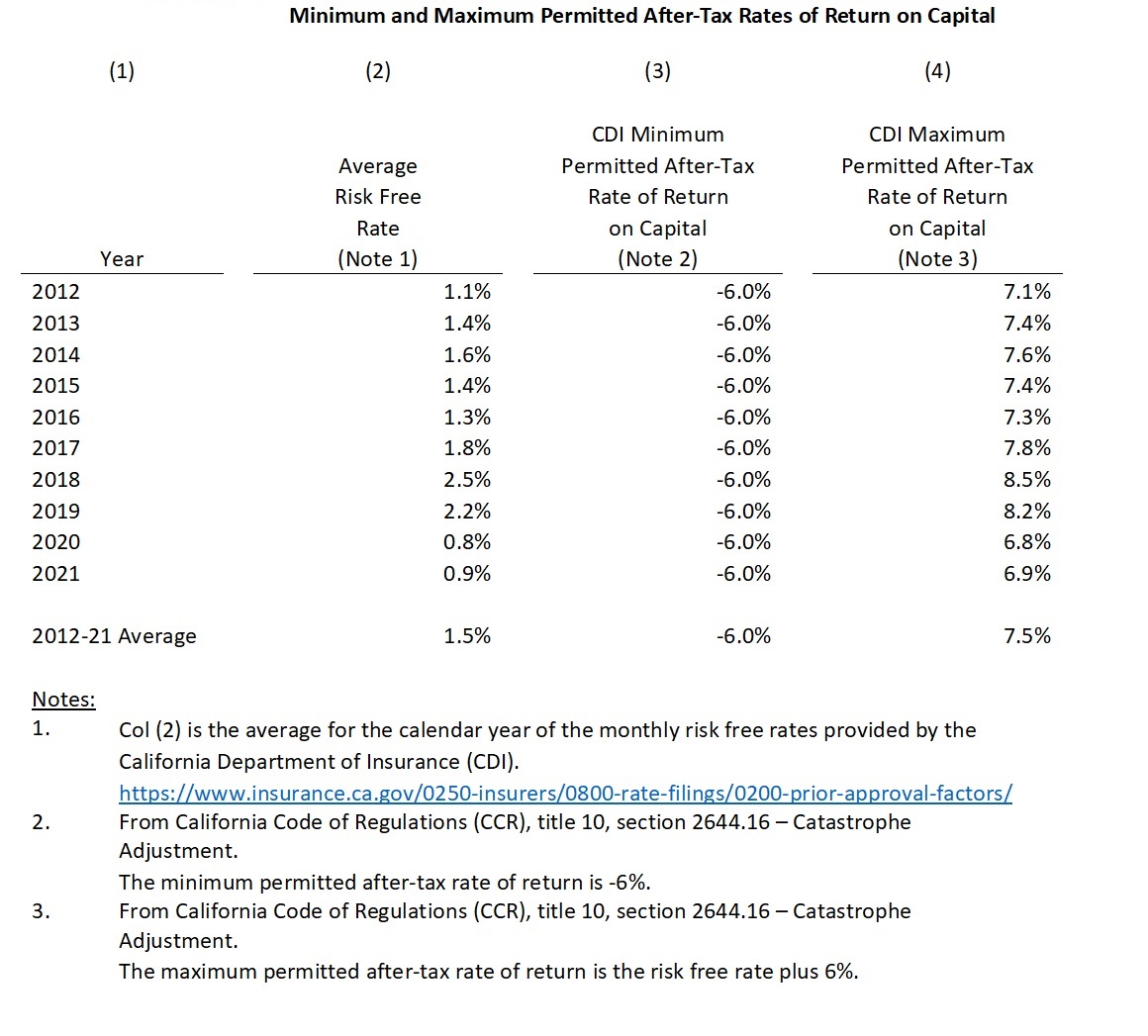

- The maximum permitted after-tax rate of return means the risk-free rate, as defined in section 2644.20(d), plus 6 percent.

- The minimum permitted after-tax rate of return shall be -6%, which the Commissioner finds is high enough to prevent any undue risk of insolvency and to prevent injury to competition through predatory pricing.

As of August 2023, the risk-free rate of return calculated by the CDI is just below 4.6 percent, resulting in a maximum permitted after-tax rate of return on capital of just under 10.6 percent.

This rate is actually substantially higher now than over the past decade, due to recent increases in interest rates. By comparison, the average maximum allowable rate of return from 2012 to 2021 was 7.5 percent.

How does this compare to the necessary returns that insurance company shareholders expect?

See related articles, “Rebuilding the California Property Market: Reinsurance Costs and Recent Reforms” and “Calculating Targeted California Returns on Surplus.”

The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs