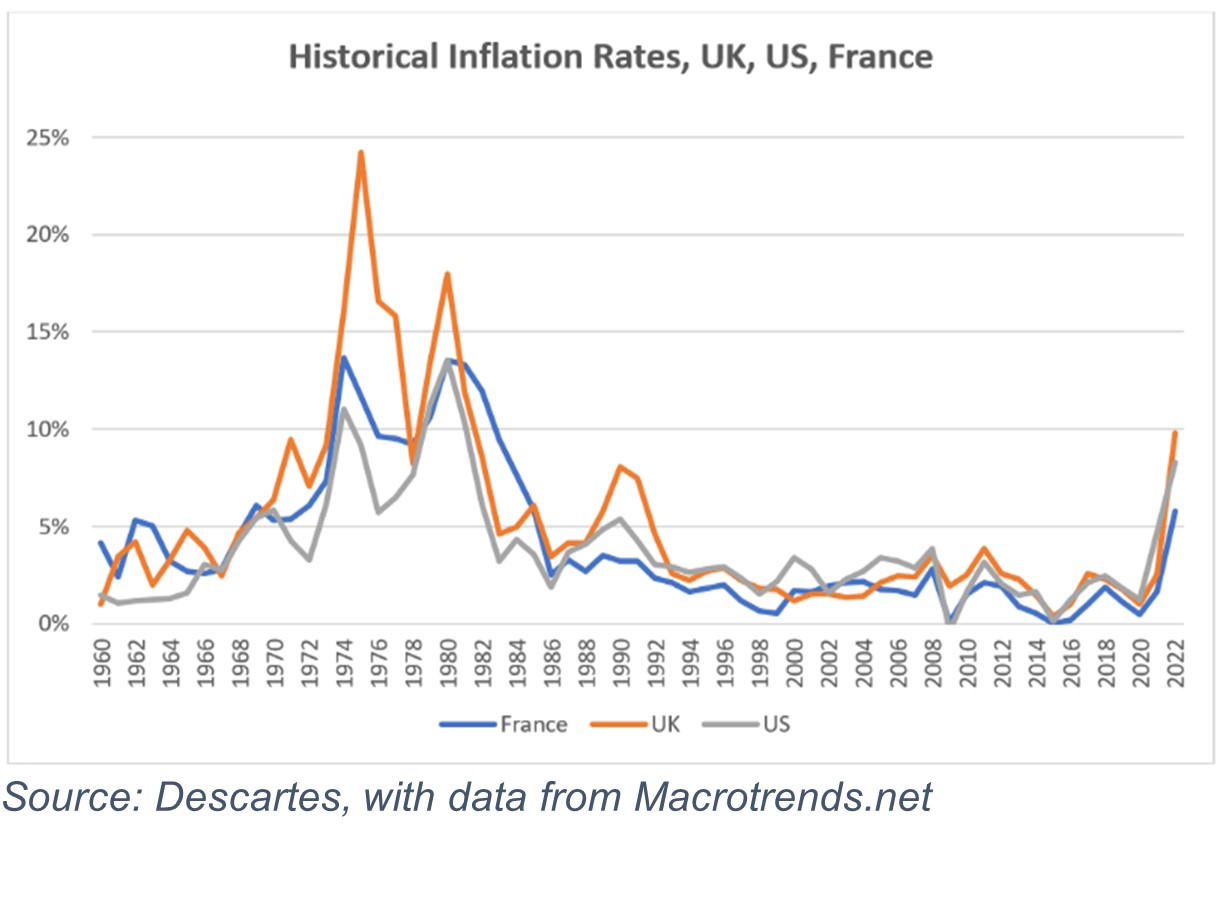

Annualized inflation in the U.S. topped 5 percent just once since 1981—until now.

In the UK, it exceeded 3 percent only rarely since 1992, and only ever by a fraction.

In France, the change in the cost of things has been even more stable during the past three decades, but inflation is back.

Executive Summary

Inflation creates an extra source of uncertainty for P/C insurers setting loss reserves for incurred claims. And insureds face higher premium costs as inflation gets factored into insurer pricing calculations. Both impacts are gone when parametric insurance policies replace traditional offerings, Lockton’s Peter Rapaciewicz reveals here.After a detailed discussion of inflations impacts on carriers and customers alike, Rapaciewicz explains that because financial loss is not directly relevant under a parametric insurance policy, neither premiums nor claims for such policies are impacted by inflation.

For the year ending Aug. 31, it was 8.3 percent, 9.8 percent and 5.8 percent, respectively, in those countries.

After decades of price stability, the return of inflation is causing a measure of havoc. While headlines herald a cost-of-living crisis, rising prices are having a complicated and sometimes convoluted impact in other areas, including the commercial insurance sector. Premium rates have been rising steadily for several years and still are on the increase, but little of the uplift so far has been intended to cover economic inflation. In some cases, inflation is only just now figuring into insurance pricing calculations after years of soft-market conditions.

As rates rise and inflation continues to create uncertainty, parametric insurance provides a solution for insurers and insurance buyers alike.

Double Pressure

Insurers’ performance is newly pressured on two fronts. The cost of new claims is rising, and the reserves set aside for incurred claims—particularly for third-party liability claims which may take years to be resolved—may now be looking insufficient in the new inflationary world.

Insurers have always factored in inflation for incurred claims (especially given the phenomenon of “social inflation,” which has seen increasingly generous jury decisions drive up the total cost of liability claims). However, property underwriters are not used to managing inflation costs. Now, as reinsurers demand to hear about each client’s inflation strategy, insurance companies are having to get to grips quickly with the impact of inflation on their businesses.

It is no easy feat. The challenge is highlighted by the phenomenon recently described as “loss creep,” which is shorthand for the initial understatement of many major catastrophe losses, experienced in events including Hurricane Irma in 2017 and 2018’s Typhoon Jebi.

Ian: How Much?

This year, Hurricane Ian has already highlighted the challenge of estimating the cost of claims, especially in light of the re-emergence of inflation. In the immediate aftermath of the event, total insured loss estimates by credible modeling firms ranged from $31 billion to $53 billion by CoreLogic to $63 billion by Karen Clark & Co. Later, Stonybrook Capital, the insurance-focused investment advisory firm, pegged the loss at $75 billion or more. That’s a difference, from the low end to high, of $44 billion, which itself would be a significant catastrophe-event loss. Estimates exclude flood losses of circa $10 billion covered by the National Flood Insurance Program.

Larger total loss estimates across the industry partially could be the result of litigation trends, and therefore could be attributed to the branch of inflation known as “social inflation.” It would occur if the plaintiffs’ bar seeks and achieves higher settlements for claimants from their insurers. Stonybrook cited loss adjustment expenses (LAE) as one element of its $75 billion-plus figure, which it estimates will account for about 20 percent of the total Hurricane Ian claims burden. Stonybrook said: “Ian’s LAE inflation and insured demand surge will be at very high levels. Some of the modelers explicitly address demand surge, but in this economy there’s more room here for negative surprises than positive.”

Covering Economic Inflation

Simple economic inflation wasn’t one of the factors driving loss creep in the cases which made the term common parlance, since they occurred before the current surge in the cost of goods and services. However, post-catastrophe supply-related inflation certainly was. Put simply, after a major catastrophe event, the ready supply of everything from loss adjusters to roofing materials is pressured by a sudden surge in demand, which naturally drives prices higher. Further, it is not unnatural for a supplier with a large stock of, say, roofing shingles to hold it back until shortages become severe, then take advantage of even higher prices.

Add economic inflation, and repair costs are soaring.

Loss adjusters Woodgate Clark, in their May 2022 Commercial Property Costs Update, reported that the cost of roofing repairs in the UK has increased by 91 percent between January 2021 and 2022. According to Checkatrade, big building jobs in the UK—like a ground-up rebuild after a house fire—may suffer the most, because roofing, bricklaying and general building work are recording some of the biggest price rises. Even plumbers cost on average 67 percent more.

In the U.S., data from the Bureau of Labor Statistics places the increase in the cost of “materials and components for construction” at 14.3 percent between September 2021 and September 2022. That includes the cost of materials for rebuilding or repairing homes and business premises damaged by natural catastrophes, and will accrue directly to the cost of insurance claims arising from Hurricane Ian. The price of the cost of construction itself increased 11 percent over the same 12-month period, and the cost of construction machinery and equipment 13.2 percent.

Insurance Impact

Consultancy McKinsey & Co. has made an attempt to quantify the cost of inflation on claims paid by U.S. property/casualty insurers. Its estimates indicate an increase in loss costs of approximately $30 billion in 2021, over historical loss trends.

“Price increases have been exceptionally high for the goods and services that drive personal insurance claims,” McKinsey reported. “Prices for motor vehicle parts and equipment rose 22.8 percent between June 2021 and June 2022… Loss costs for lines with long settlement periods, such as workers compensation, went up by an incremental $4 billion, and high prices for core commodities drove up loss costs in multi-peril insurance lines, both personal and commercial, by an incremental $8 billion and $2 billion, respectively.”

As insurers begin to negotiate their annual Jan. 1 reinsurance renewals, emphasis on concerns around inflation will very much be on the minds of reinsurers.

Inflation-Proof Coverage

Parametric coverages provide a simple solution to the inflation challenges faced by insurers and insurance buyers. Unlike traditional coverage, which relies on the lengthy loss adjustment procedures necessary to indemnify actual, measured losses, parametric insurance pays out a predetermined claim amount. All that is required for a parametric policy to be triggered is the occurrence of a predefined event, as measured by a specified index. It is the provider that informs the insured that a claim can be made, turning usual practice on its head.

Parametric insurances are appearing increasingly often among the product lines offered by conventional insurers and brokers. Typically, they are created and administered by a managing general agent or underwriter (often considered an “InsurTech”) that manages to assess risk and monitor triggers. The entire process, from underwriting to claims settlement, is remarkably efficient, since it eliminates a huge share of the administration and loss adjusting expenses associated with traditional insurances. That makes parametrics attractive both to carriers and to insureds, as the ratio of expenses to limit is usually lower.

Eliminate Reserving Risk

Simply put, the quantum of the financial loss is not directly relevant under a parametric insurance policy, so neither premiums nor claims are impacted by inflation. It is the loss event that’s insured, not the cost of putting things right. The entire inexact science of claims reserving and associated reserving risk are therefore eliminated, delivering incredible new levels of certainty for insurers, since claims severity is removed from the equation.

Some proof of loss or at least a measure of exposure (an “insurable interest”) is necessary under the law in almost all jurisdictions to ensure that the contract is a regulated policy of insurance rather than a derivative. Parametric coverage is not just a wager, nor are the claims it pays direct indemnities.

The trigger of a claim could be a flood, cyclone, earthquake or almost any other insured occurrence within the covered location during a minimum period. It must simply surpass a specified threshold (such as, respectively, water level, windspeed or intensity), as measured by the relevant index, always based on data provided by a third party. The use of fixed payments and third-party data eliminates not only the costs and delays associated with claims adjustment but also the moral hazard related both to trigger thresholds and to claims circumstances and severity.

Risk managers are more sophisticated than ever and look to use a new generation of products to replace traditional insurance coverage, as capacity dwindles and prices surpass affordability. More importantly, parametric products can also be used to complement traditional insurance coverage, proving effective as a protection against non-damage losses and policy-coverage gaps. Parametrics are also extremely efficient and effective as triggers for reinsurance. Instead of waiting, for example, for accumulated claims to accrue in sufficient volume to trigger a retrocession layer, a parametric policy will pay the sum specified within days of the occurrence of a measured event.

Now for Corporate Buyers, Too

These innovative new risk transfer products are no longer limited to sophisticated plays in the insurance-linked securities (ILS) market. Parametric policies are equally efficient and effective when underwritten by conventional risk carriers in partnership with parametric specialists, for sale through brokers or direct to insured clients. Organizations ranging from states, NGOs, corporations and midsize enterprises to insurers and reinsurers can now benefit from a huge range of parametric products, which cover everything from active shooter incidents to cloud downtime. They remain particularly widespread in the management of climate-related risks, including those exacerbated by climate change.

Clients like parametric insurance solutions because they are priced based on the likelihood of the occurrence of the storm, flood, heatwave or other parameter. Insureds are protected from the difficult-to-predict and sometimes seemingly uncontrolled rate increases imposed by insurers seeking to shield their balance sheets from inflation impacts. That price stability puts clients in the driving seat. They can decide, with support from their brokers, about the adjustments to their retentions and sums insured necessary to reflect the impact of inflation on their business. That makes parametric products an essential offer of any insurer in the current inflationary environment.

Wildfire, Flood Risk Boosted by Extreme Weather Threaten U.S. This Week

Wildfire, Flood Risk Boosted by Extreme Weather Threaten U.S. This Week  What Happens to Property Pricing in ’27, Insurance, Reinsurance Execs Ask

What Happens to Property Pricing in ’27, Insurance, Reinsurance Execs Ask  USAA Not Done With Dividends: Florida Reforms Prompt $0.5B Payout

USAA Not Done With Dividends: Florida Reforms Prompt $0.5B Payout  Insurance AI: What You Won’t Read in the Press Releases

Insurance AI: What You Won’t Read in the Press Releases