We’ve entered an inflationary environment, and a significant one at that. The Consumer Price Index (CPI), which has been slowly inching upward since May 2020, increased 0.9 percent from September to October while also reaching its largest year-over-year hike—6.2 percent—since 1990.

Inflation has a larger impact on the insurance industry than most others. However, inflation doesn’t affect all areas of the insurance industry in the same way. Insurance carriers typically suffer during inflationary periods while insurance distributors do well.

Inflation’s Negative Impact on Insurance Carriers

Supply chain issues, labor shortages and rising energy costs are all coming together to further increase loss costs for home insurance premiums. Auto insurance is impacted even more severely with rising costs for cars and car parts.

In many industries, the response would be to raise prices, but there are two key reasons that doesn’t work for insurance carriers. The first is simply the competitive market. No insurance carrier wants to be the first to raise its rates and send its policyholders looking for a new company.

The second reason, however, is the bigger hurdle to overcome, and that’s regulations. Insurance companies writing on an admitted basis (which is the vast majority of the market) have to file their rates with state insurance departments, and that means providing an actuarial justification for the increase. Essentially, insurers must provide historical data, usually more than a year’s worth, that shows their rate increases are necessary.

It usually takes about six months to get approval, another year to reprice the policies (assuming one-year policies) and then another full year for the higher premiums to be earned. In other words, insurers are losing money for roughly two-and-a-half years while trying to adjust for inflation—and there’s always the chance that loss costs will continue to rise in the interim.

Why Distributors Weather Inflation Better

Insurance distributors—agents and brokers—generally have better economics than insurance carriers, with higher margins, lower volatility and lower capital requirements. They also don’t suffer the negative impacts of rising loss costs because they aren’t responsible for paying claims. Distributors may have some parts of their revenue, called contingent commissions, that are impacted by loss ratios, but the majority of their income comes from commissions that are a fixed percentage of premiums.

Moreover, distributors benefit once carriers are allowed to raise their rates. Their commissions are a fixed percentage of the premiums they bring in, so a rate increase generally means more money in their pockets. Plus, customer acquisition costs will most likely go down as more people are in the market for new policies.

The one downside distributors need to grapple with is that underwriting capacity may be harder to find for new customers as insurance carriers become more selective with their underwriting. Overall, however, the data indicates that distributors and other intermediaries fare much better than carriers in an inflationary environment.

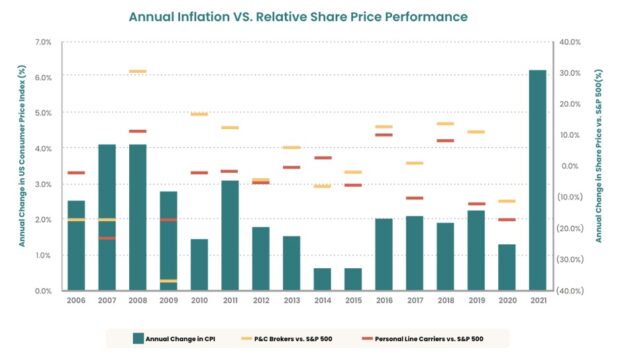

To demonstrate this, we looked at the annual change in the CPI from 2006 onward and compared several property/casualty brokers’ performance against the S&P 500 to personal lines carriers’ performance against the S&P 500.

We found that P/C brokers outperformed personal lines carriers every year except in 2006, 2009 and 2014. And if we only consider years when the CPI changed by 3 percent or more, P/C distributors always outperformed carriers.

The Effect of Misaligned Interests

Distributors have increased margins and want to grow during inflationary periods, while carriers have decreased (and even negative) margins and don’t want to grow, which creates a misalignment of interests. Scarce capacity doesn’t negate the benefits insurance distributors enjoy in an inflationary environment, but without the misaligned interests, those benefits would be even greater.

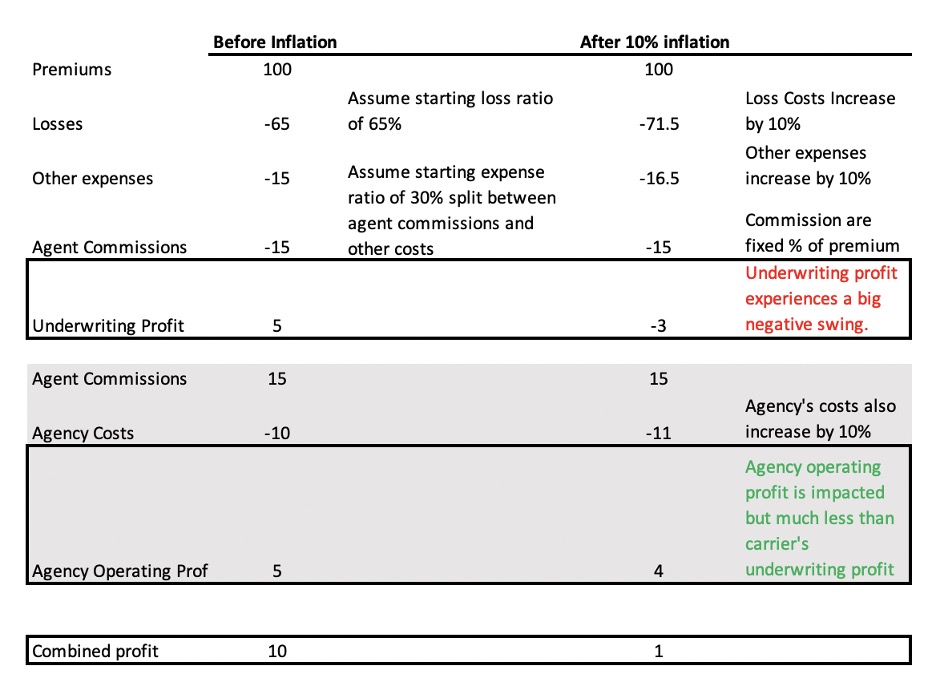

Consider the following hypothetical example that assumes a 10 percent shock to both loss costs and operating costs for the carrier and the agent.

The carrier, which I assume starts with a 5 percent underwriting margin, is negatively impacted because premium initially stays constant while all costs increase—except agent commissions, which are a fixed percent of premium. The result is a swing from underwriting profit to underwriting loss.

The agency, which I assume starts with a 33 percent operating margin, is also impacted by increased costs without an increase in revenue, but the effect on operating income is much less than what the carrier experiences.

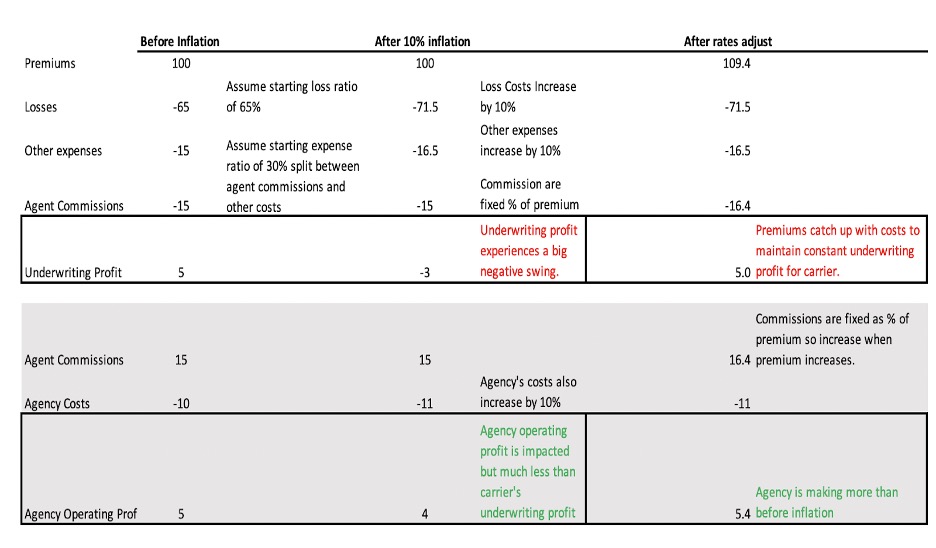

Once the rates adjust, the carrier returns to its initial 5 percent underwriting margin and the agent benefits from an increased commission because of higher premiums, resulting in higher margins.

Embracing an Alternative Business Model

Carriers that rethink the role of agents and keep the more attractive distribution economics by selling direct will benefit from a valuable hedge against underwriting profit.

In this example, the combined carrier and agent never goes negative during an inflationary period. In fact, it performs better than it did before the inflationary period began.

That is a unique opportunity for the direct carrier because it can continue to grow profitably even when the underwriting environment is unfavorable.

Drone Crashes, Severed Fingers Pose Problems for $13B Silicon Valley Military Startup

Drone Crashes, Severed Fingers Pose Problems for $13B Silicon Valley Military Startup  From ‘FBI Claims Handling’ to AI-Assisted Workflows

From ‘FBI Claims Handling’ to AI-Assisted Workflows  The Big Dog Is Off the Tech Porch: State Farm as ‘Next Gen Good Neighbor’

The Big Dog Is Off the Tech Porch: State Farm as ‘Next Gen Good Neighbor’  The Readiness Is All: New AIG CEO Andersen Talks Industry Relevance

The Readiness Is All: New AIG CEO Andersen Talks Industry Relevance