U.S. property/casualty insurers have benefited from significant increases in commercial premium rates for nearly three years. However, recent industry statutory underwriting performance improvement was dampened by several factors, including persistently high natural catastrophe losses and claims related to the COVID-19 pandemic, limiting the market to slightly better than break even underwriting gains.

While 2022 underwriting performance is projected to improve as commercial pricing trends remain largely favorable, it is unlikely that industry combined ratios and return on surplus will reach levels achieved in the last hard market that occurred in the early-mid 2000s. Potential for adverse claims experience in multiple segments and shifts in industry profit fundamentals over time are key offsets to future profit improvement.

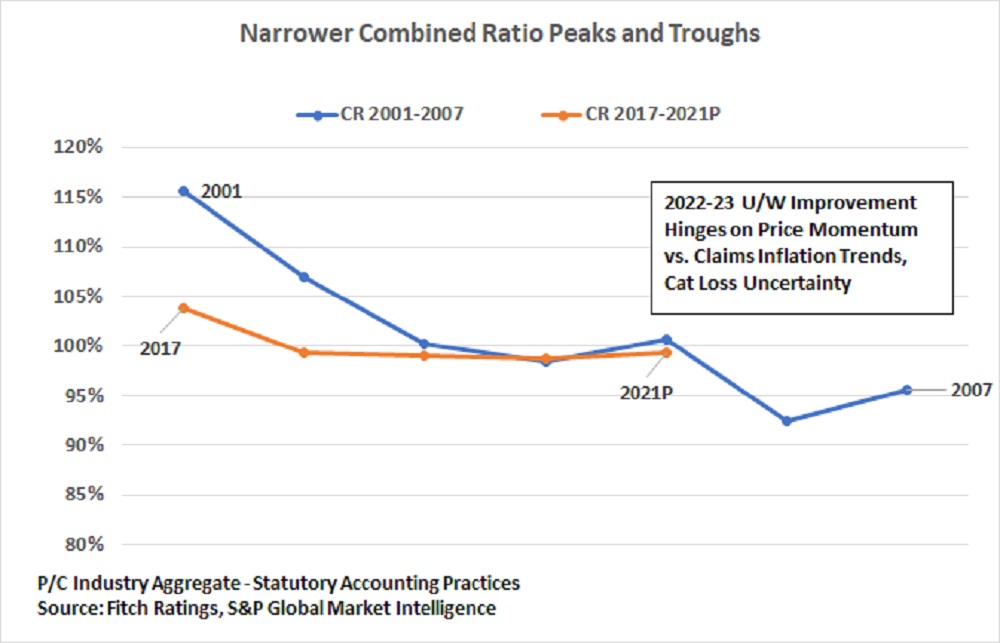

Commercial property rates started shifting positively following a 104 industry combined ratio in 2017, (tied to severe catastrophe events, including hurricanes Harvey, Irma and Maria). Profit deterioration in most liability lines relating to escalating litigation and settlement costs promoted a material pricing turn in many other commercial segments in 2019.

Rate increases accelerated in 2020, to levels last seen in 2003. The change in commercial market premium rates has averaged 10 percent for the last seven quarters from first-quarter 2020 through third-quarter 2021, according to the Council of Insurance Agents and Brokers market survey. Shifts in pricing and shifts in underwriting practices—more conservative limits, retentions, use of sublimits and exclusions—also continued.

Industry profitability steadied with a reported statutory combined ratio approximating 99 for calendar years 2018-2020, and likely repeated for full-year 2021, with annual net profits ranging around $60 billion for the last four years as well.

The last hard market was spurred by more severe losses and deep reserve weakness that led to a more pronounced turnaround in performance. The industry reported its first statutory net loss in modern times in 2001 with a combined ratio of 116, driven by large losses from the September 11 event, extremely poor commercial lines market conditions and substantial reserve deficiencies in casualty lines. Industry surplus declined by 8 percent in 2001 as investment market losses added to poor operating results.

Recovery in profitability took some time to emerge given the magnitude of pricing inadequacy and recognition of prior reserve deficiencies, but the industry reported its first sub-100 combined ratio since the late 1970s in 2004. Effects of hurricanes Katrina, Rita and Wilma moved the market back to a slight underwriting loss in 2005, before industry performance peaked with combined ratios of 92.4 and 95.6 in 2006 and 2007.

In reaction to the strong results, an inevitable market softening led to deterioration in underwriting performance in future years.

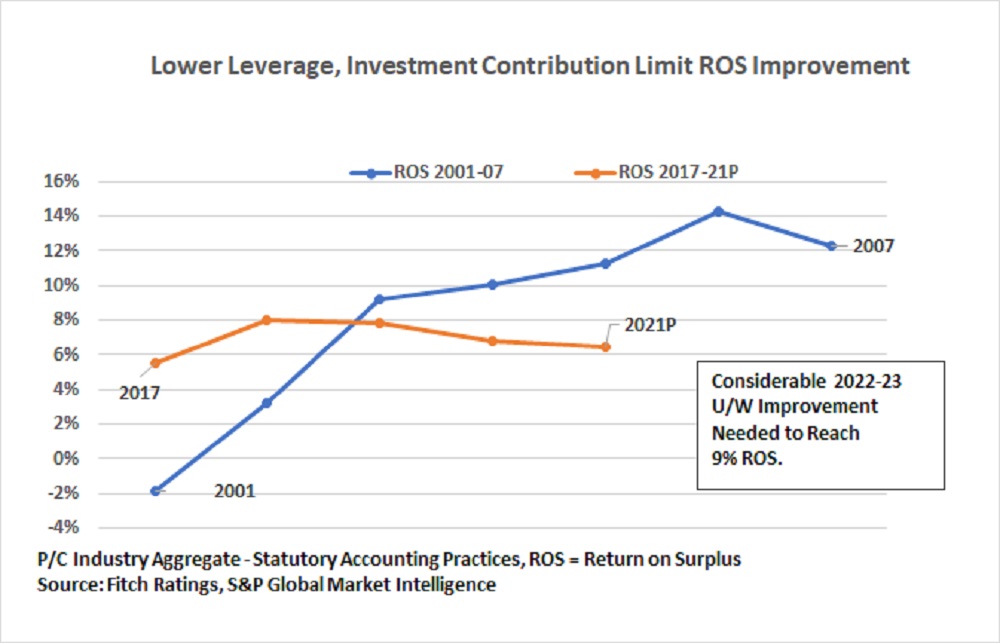

Disparities in the magnitude of the peaks in the market cycle are demonstrated in the returns generated during the respective periods. The industry generated a double-digit return on surplus (ROS) for four consecutive years (2004-2007) in the last hard market. In contrast, ROS will average over 7 percent from 2018-2021.

The market shift to a hardening phase in the current cycle prior to reaching a weaker soft market nadir of previous periods is a testament to improvements in underwriting practices and better information systems promoting quicker recognition of adverse trends. However, the stability in recent results and challenges in further boosting profits and returns are representative of a highly competitive market and less attractive profit fundamentals and macro-factors.

The market shift to a hardening phase in the current cycle prior to reaching a weaker soft market nadir of previous periods is a testament to improvements in underwriting practices and better information systems promoting quicker recognition of adverse trends. However, the stability in recent results and challenges in further boosting profits and returns are representative of a highly competitive market and less attractive profit fundamentals and macro-factors.

Since the mid-2000s performance peak, insurers’ capital management practices grew more conservative due to recognition of expanded catastrophe and liability risk and more stringent regulator and rating agency requirements. At year-end 2020, industry written premium-to-surplus was approximately 0.7; 15 years earlier, in 2005, the ratio was 1.0. As a result, other things equal, each dollar of underwriting profit has a 30 percent lower effect on return on capital due to lower leverage.

Additionally, the investment earnings contribution to returns has substantially diminished due to lower asset leverage (invested assets/surplus = 2.2-times in 2021 versus 2.6 in 2005) and falling investment yields as the industry portfolio yield was under 2.2 percent at year-end 2020—a 240-basis point decline from 2005.

Sharp declines in the risk-free interest rate over time have also substantially lowered the equity cost of capital over time, and profitability does benefit currently from lower corporate income tax rates (21 percent vs. 35 percent previously).

Still, current market fundamentals suggest that approximately a 95 combined ratio is necessary to generate a 9 percent return on surplus.

Significant further underwriting improvement is needed to reach this underwriting profit level. The market combined ratio could approach the 95 range in 2022-2023, as past rate increases flow through earned premiums, and barring excessive losses from catastrophes or other unforeseen events. But a number of uncertain factors reduce the chance for consistent long-term favorable underwriting margins, including:

• Competitive forces and rate hike fatigue. Growing signs of a 2022 tapering in pricing momentum lead to questions about the longer-term potential for rate changes to stay ahead of loss trends. At some point in a hardening market phase, policyholders adapt to higher rates through changes in buying practices or self-insuring.

Emergence of several well-capitalized specialty lines startup companies may have a broader impact on price competition going forward as their premium base expands.

• Inflation risks. Socio-economic changes and public policy actions relating to the coronavirus pandemic led to the revival of inflation in 2021, with the consumer price index (CPI) rising 7 percent for the year, a level unseen since the early 1980s.

A growing chance that inflation remains above past norms beyond 2022 poses risks of larger pricing errors for P/C insurers. Shifts in claims trends are currently most apparent in property and auto lines. However, the larger threat of persistent high inflation is in long-tail casualty lines, where reserve deficiencies may take several years to emerge.

• Litigation costs and jumbo verdicts. Prior to the pandemic, multiple liability insurance product segments, including commercial auto and professional liability, were challenged by claims severity driven by evolving sources of litigation activity and substantially higher settlements and jury verdicts or “social inflation.” While the pandemic induced a pause in this trend due to court closures and other factors, future spikes in litigation actions and severity are likely.

Particular risks for heightened litigation would derive from a pronounced economic or stock market downturn, or potential for litigation in emerging areas, including cyber threats or ESG risks.

• Automobile insurance weakness. The sharp slowdown in 2020 driving activity—and claims frequency—led to record underwriting results in the personal auto market that were far from fully offset by premium rebate and discounting efforts.

A return toward prior driving norms and claims frequency, along with adverse loss cost changes tied in part to supply chain risks on physical damage claims, led to a sharp turnaround in 2021 results—back to a calendar-year underwriting loss.

Problematic claims trends and potential for a lagging price reaction to poorer results could inhibit auto insurance performance for the next two to three years.

• Workers compensation deterioration. The largest individual commercial lines product segment has been a bellwether for underwriting profitability, with average combined ratios in the low 90s for five consecutive years and large reserve redundancies.

Workers compensation is a market outlier also as the one segment with several years of flat-to-declining premium rates. Premiums will increase from higher payroll exposures. But pricing deterioration will inevitably lead to weaker results, with an accelerated decline potentially driven by rising medical inflation amidst a general inflation surge and the potential for higher claims losses as a tight labor market leads to a less trained and experienced workforce.

• Equity market performance. Industry surplus increased by 30 percent since year-end 2018, fueled by steady operating earnings and large investment gains on equity and alternative investments. The average annual return on the S&P 500 was approximately 26 percent for the last three years, which approaches levels last reached in the late 1990s market boom.

Investment performance is more likely to taper going forward, as monetary policy tightens and considerable economic uncertainty remains, reducing the volume of investment gains and the pace of surplus growth.

Deepest Drilling Study Ever Provides Insight into Deadly Japan 2011 Tsunami

Deepest Drilling Study Ever Provides Insight into Deadly Japan 2011 Tsunami  AI Pushes Underwriting Beyond Risk Selection to Prevention

AI Pushes Underwriting Beyond Risk Selection to Prevention  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  Raised on Breaches, Digital Natives Think Differently About Cyber Risk

Raised on Breaches, Digital Natives Think Differently About Cyber Risk