Reverse competition is a major problem in insurance lines like title insurance, credit insurance, and lender-placed insurance—one that is not easy to correct.

Executive Summary

Opinion: If lenders paid for title insurance policies instead of borrowers, then the problems of reverse competition in the line would end, consumer advocate J. Robert Hunter believes.Following up on the first part of this opinion piece, in which he explained the factors that allow insurers to reward third parties for steering buyers in lines like title insurance, credit insurance and lender-placed insurance, Hunter proposes some fixes, including warnings to consumers from regulators.

News of potential abuses in these lines is not new. A GAO report on problems in title insurance was published in 2007, and the New York Department of Financial Services started looking into seemingly improper inducement expenses in 2012. But the spotlight was shown on alleged abuses again recently when The New York Times published an article about title insurer spending on entertainment for real estate executives, and the NYDFS proposed regulations that would have expanded a list of banned marketing expenses to include even those incurred in situations where there is no direct quid pro quo for business in the state.

More recently, the industry has fought back in the Empire state, causing a delay in the proposed effective date of the regulations. On Jan. 16, the state Senate passed a bill proposing to put the “quid pro quo” language into the law (weakening the regulation), and the Assembly was still considering it at the date of this writing.

The beneficiaries of reverse competition—insurers, lenders, lawyers, car dealers, real estate professionals, etc.—will fight to protect the status quo, making the politics of quashing this anti-consumer form of competition are extremely challenging. Consider the current brinksmanship going on in New York, where modest regulations to eliminate the most egregious abuses led to state legislative efforts to walk back the regulations after a $400,000 industry lobbying campaign. (The lobbying figure was reported in the New York Times article, “New York’s Hidden Home Buyer Closing Costs: Luxury Boxes and Mint Mojitos,” Jan. 29. 2018 by Shane Goldmacher.)

But lawmakers and regulators have a duty to overcome these heavy lobbying efforts. To some degree, these lines may fall in the crack between banking and insurance regulators who have not coordinated the regulation of these crossover policies sufficiently. Further, reverse competition activities involve hard costs–like the expenses paid as kickbacks or outsized commissions for force-placed home insurance –that can be shown on insurers’ books and get presented as factors that drive up the expense component of rates. However, these expenses are not “used and useful” for the purpose of delivering the insurance policy to the policyholder. They are akin to bribes paid to get the business and should be disallowed in the premium charged to customers.

Similarly, the title underwriter that rented out Citi Field for the purpose of luring real estate officials to steer title insurance business their way can show a real expense. But that expense is of no value to the homeowner who, in New York, pays over 6 percent of premium to cover parties such as that, as well as golf outings, ski trips, and strip club visits. These expenses (or bribes) must be disallowed from rates charged to consumers.

Editor’s Note: Maria T. Vullo, Superintendent of the New York State Department of Financial Services, discussed a variety of entertainment expenses in testimony for a public hearing on Jan. 12, 2018. These items were uncovered during a 2012 investigation by the department. During a Dec. 10, 2013 hearing, a DFS attorney questioned representatives of title insurers about attorney marketing expenses that included meals, tickets to the Super Bowl and visits to Blush, a gentleman’s club.

The author testified at the same hearing that the amount of improper expenses from 2008-2012 amounted to more than 6 percent of title premium.

The author’s reference to renting out Citi Field refers to information presented more recently in a Jan. 29, 2018 New York Times article, “New York’s Hidden Home Buyer Closing Costs: Luxury Boxes and Mint Mojitos” by Shane Goldmacher.

States should hold hearings in the reverse competition lines of insurance to determine if the rates are excessive. At the hearings, states should require sufficient detail on the expenses related to kickbacks, improper commission arrangements, sham captive reinsurance arrangements, parties for intermediaries, luxury boxes at sporting events and such, that they can act to exclude these expenses from rates in the state.

If a state does not act to squeeze the lavish marketing costs out of premiums, regulators are effectively allowing excessive rate for these risks in violation of the laws of most states. For instance, given that the current loss ratio for title insurance is about 5 percent, it is clear that title insurance premiums are wildly excessive. (Data for 2016 shows a loss and loss adjustment expense ratio of 5 on earned premiums of $13.9 billion; in 2015 the ratio was 5.2 on $12.8 billion of earned premiums. Source: Title Industry Statistical Analysis by Family and Company (2016 and 2015), American Land Title Association)

Lower, but still extreme, degrees of excessiveness can be shown for the other lines plagued by reverse competition. So, if conscience doesn’t impel action, state law must.

“To some degree, these lines may fall in the crack between banking and insurance regulators who have not coordinated the regulation of these crossover policies sufficiently.

J. Robert Hunter

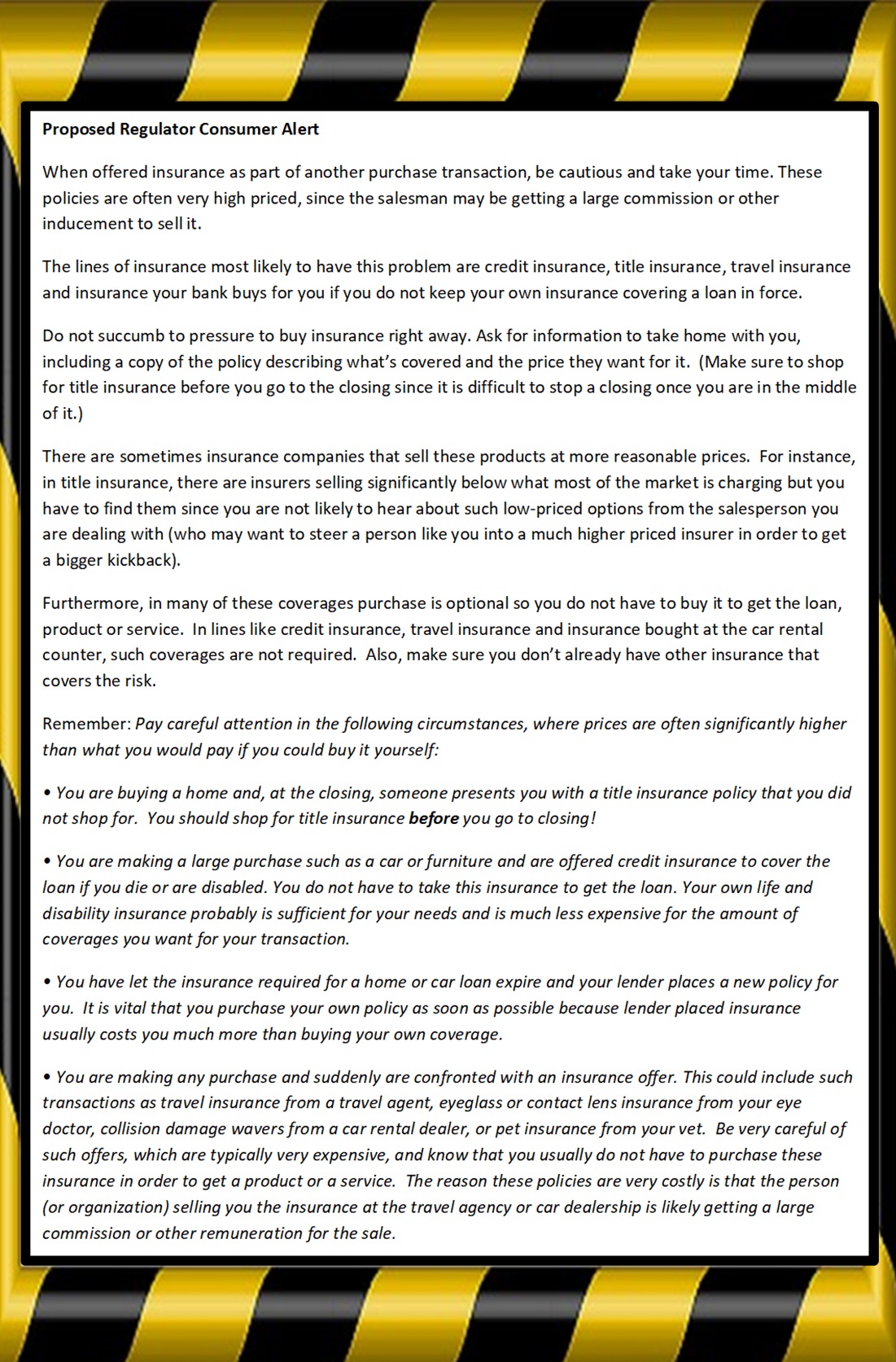

Regulators should also warn consumers of the dangers they face when purchasing insurance in a reverse competition line. An example of the sort of warning they might consider is found in the sidebar to this article. (The sidebar is presented below the text of this article and available at a separate link.)

State legislators should consider action to end reverse competition. For example, they should consider actions such as:

- In title insurance, consider modeling the state system after Iowa’s low-cost system.

- In title insurance, consider requiring lenders to buy their own title insurance rather than requiring the consumers to individually buy it for them. They would then purchase much more efficient group policies and would pass along the much lower costs to consumers in the loan arrangements.

- In force placed-insurance, require lenders to, when a policy is being canceled or nonrenewed for non-payment of premium, keep the policy that the consumer chose in force rather than force-placing a policy with a new carrier that the lender chooses. Alternatively, allow lenders to only place policies that have the same or lower total premium as the replaced coverage.

- In credit insurance, establish minimum loss ratios for credit insurance and enforce those standards. Although higher standards are easily justifiable as reasonable, the rock-bottom minimum loss ratios of 60 for credit life and disability and 75 for credit unemployment and credit property insurance should be enforced. Consumers also should not be required, at the lender’s choice, of paying credit insurance premium for coverage beyond that necessary to protect the lender’s interest.

Competition shouldn’t harm consumers, it should help them. But reverse competition is a perverse form of competition that has yet to be adequately addressed by the nation’s insurance regulators. It must be!

AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  Global Wildfire Surge Hits U.S, Propelled by Rising Temperatures

Global Wildfire Surge Hits U.S, Propelled by Rising Temperatures