Shoppers in the U.S. aren’t ready to accept higher auto insurance rates, choosing to shop around for the best deal and coverage, a new report finds.

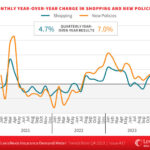

U.S. consumer auto insurance shopping activity registered as “Hot” on the LexisNexis Insurance Demand Meter, as quarterly year-over-year shopping grew 2.9 percent for Q1 2024 (slowing slightly from last quarter’s 4.7 percent increase year-over-year).

As a result, insurers continue to adjust strategies to retain customers for long-term growth.

The quarterly year-over-year growth for new policies was “Sizzling,” up 8.7 percent for Q1 2024 (and up again from +7.0 percent last quarter).

Quarterly year-over-year new policy growth increased, trending up for the seventh consecutive quarter and 20th straight month, meaning consumers continue to switch carriers at an increasing rate when they shop. the report found.

Even as March saw a slightly lower shopping growth rate from the previous year – possibly attributable to fewer workdays and more weekends than in 2023 – 42 percent of insured households shopped in the last 12 months.

When comparing all years back to 2021, consumers most likely to be retained by their existing insurance company – or those who have been loyal for 10+ consecutive years – comprised less than 20 percent of the shopper pool.

Through Q1 2024, this cohort has grown to 24 percent of total shoppers.

In Q1 2024, the growth in new drivers largely offset the number of leavers. This bucks the trends observed in 2022 and 2023 where a record number of consumers left the market in response to higher premiums.

In Q1 2024, shoppers aged 66-year-old and over looked for insurance at the highest clip, according to LexisNexis, with higher premiums helping incentivize those on fixed incomes to shop.

Tax season delivered a shopping boost as more uninsured consumers re-entered the market despite purchase rates remaining lower than historical averages for the uninsured population.

Despite healthy shopping patterns for Q1 overall, March was the outlier with shopping growth falling slightly negative.

“As we have seen more shopping in recent months from consumers who have traditionally been longer-tenured and more loyal, insurers with an appetite for growth may still have an opportunity to capitalize as these consumers seek to lower their premiums,” said Adam Pichon, senior vice president, global analytics, LexisNexis Risk Solutions. “Insurers may also want to consider implementing stronger retention strategies as they seek to return to rate adequacy and profitability, including more proactive and selective monitoring of their renewal books to help identity and retain those loyal policyholders.”

Though shopping has remained high through the first three months of 2024, it has not outpaced shopping growth from Q4 2023.

“Fewer large rate increases are being implemented by many insurers, but will traditionally loyal consumers now continue to shop, having realized there may be opportunities to save in the future? If so, this could present yet another shift in the shopping paradigm insurers must consider,” said Pichon. “Those insurers with a measured approach to acquiring the right new business and retaining their most profitable business stand poised to gain market share as the industry overall continues to climb back to profitability.”

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  Two Trailers Containing $1.3M in Stolen Copper Wire Recovered in Illinois

Two Trailers Containing $1.3M in Stolen Copper Wire Recovered in Illinois  Secondary Perils Responsible for Virtually All 2025 Nat-Cat Insured Losses in North America: Swiss Re

Secondary Perils Responsible for Virtually All 2025 Nat-Cat Insured Losses in North America: Swiss Re  California Theft Crew Busted, Responsible for $1.3M in Stolen Vehicles

California Theft Crew Busted, Responsible for $1.3M in Stolen Vehicles