The U.S. excess and surplus lines market reported double-digit growth for the fifth straight year in 2022,with second-ranked Berkshire Hathaway pushing the total growth figure for the E&S market up over 20 percent, a new report shows.

In its report, “U.S. Excess and Surplus Lines Market Review,” Fitch Ratings also reported that the sector overall delivered better underwriting results than the broader P/C market for the first time since 2015.

Fitch expects better growth and underwriting results for 2023 as well, the report says, noting that growth is likely the result of admitted markets’ “shedding of unprofitable, volatile business.”

“The E&S market is expected to report its second-consecutive direct underwriting profit in 2023 given high demand and a favorable pricing environment,” said Fitch Senior Director Douglas Pawlowski. “This comes at a time where the inflationary environment continues to make it difficult to properly insure to value in property lines as well as project ultimate losses in longer-tailed casualty lines.”

The Rankings

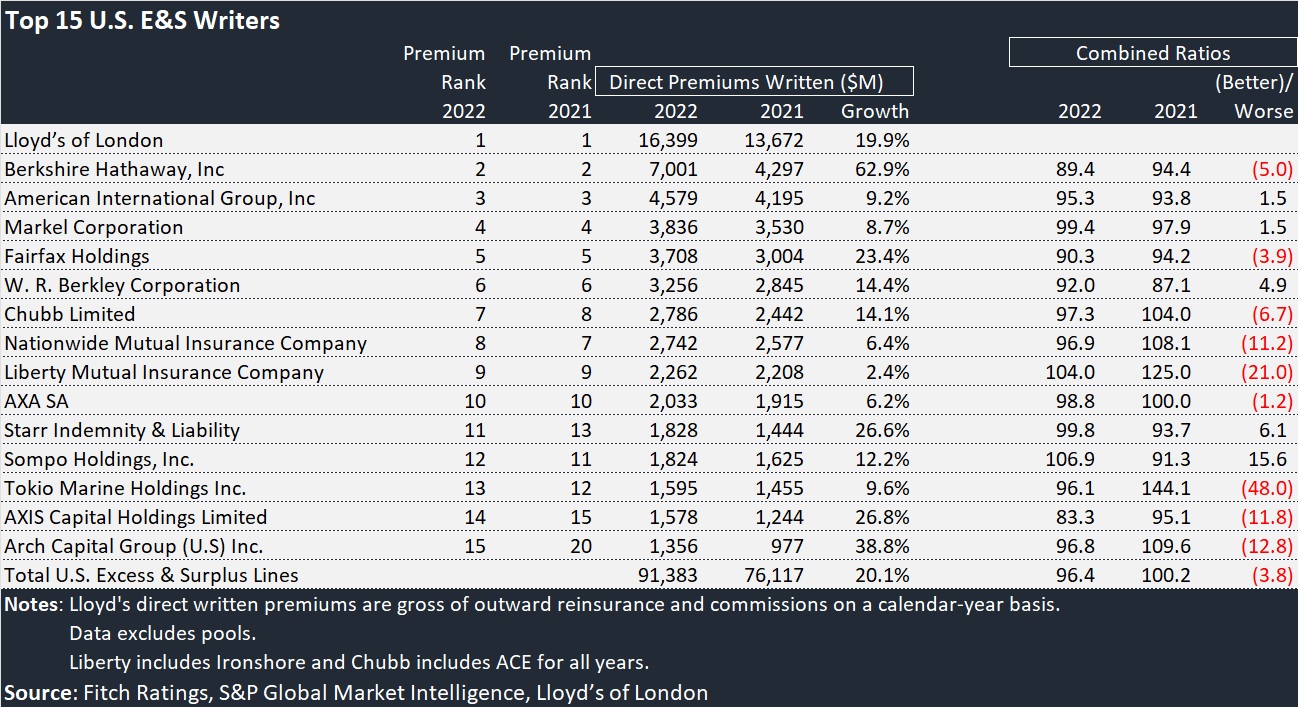

In 2022, Fitch reported that 67 insurance groups wrote greater than $200 million of E&S premiums. Charts included in the report show direct written E&S premiums for the years 2018-2022 for the top 26 players (including Lloyd’s). Premiums and rankings for 2021 and 2022 for the top 15 are excerpted below.

All E&S top market leaders experienced premium growth.

In the U.S., the E&S market competition is concentrated, with Lloyds of London being the largest underwriter (18 percent market share) and Berkshire Hathaway Inc. (8 percent) and American International Group (5 percent) rounding out the top three.

Berkshire Hathaway cemented its market share with its acquisition of Alleghany Group Inc., at the time the 11th largest E&S writer. The acquisition enabled Berkshire Hathaway to grow its E&S premiums by 63 percent in 2022. The company is expected to continue its expansion in the E&S market in the future, based on its multiple specialty underwriting platforms and the industry’s largest capital base.

Berkshire surpassed both AIG and Markel in 2020 to command the spot below Lloyd’s, according to figures in the Fitch report.

AIG reported modest average growth of 6.5 percent between 2018 and 2022.

Together, the top three E&S writers “account for nearly one-third of the total industry DWP, while the top 15 writers accounted for nearly two-thirds of total DWP,” the report stated.

Because of the success, the market is seeing new competitors, with both admitted and non-admitted capabilities, originating from Bermuda or the Lloyd’s markets, the report added.

Recent acquisition activity in the E&S market remains focused within specialty managing general agents and other distribution sources to gain access to new books of business, Fitch stated.

Growth of a Market: Nearing $100 Billion

While historically the E&S market accounted for a steady 5 percent of the total P/C market, its growth took off in 2018, and the market now accounts for nearly 9 percent of the total U.S. P/C insurance industry.

For the past 12 years, E&S direct written premiums have increased with direct statutory premiums written reaching $91 billion in 2022.

Total E&S premium grew by 20 percent in 2022, considerably higher than the 10 percent growth of the entire P/C industry. Excluding Berkshire Hathaway’s unusual jump spurred by the Alleghany acquisition, premium growth for the sector was about 17.5 percent.

The market reported a direct combined ratio of 96 in 2022, an improvement from breakeven results of the prior year.

The best 2022 combined ratios were reported by some of the smallest insurers on the E&S premium leaderboard—Kinsale, posting a 75.6 combined ratio, and American Financial Group, coming in at 82.5, both ranked below the top 20 in terms for premium volume. AXIS Capital, ranked 14th in terms of premium volume, and Travelers, ranked 24th, posted the third and fourth best E&S combined ratios last year, according to Fitch, while Berkshire’s 89.4 was the fifth-best underwriting result.

Line by Line

While both property and casualty lines reported underwriting profits in 2022—reversing a two-year trend of elevated property losses —the E&S market topped P/C’s underwriting results with a combined ratio almost 5 points better (96.4 for E&S vs. 101.1 for the industry overall).

On the property side, Fitch reported that allied, commercial multiple peril, homeowners and fire paved the way for the sizable 13-percentage point improvement in the property combined ratio.

Casualty lines improved slightly by less than one point, led by the other liability-claims made line.

Admitted carriers have dealt with challenges over the past several years, given rising loss costs due to inflation coupled with above-average catastrophe losses. With fewer constraints in regulation, pricing and policy form language, harder-to-place and volatile accounts moved to the E&S market.

According to the rating agency, the flexibility of the E&S market fosters innovative and tailored underwriting for unique or complex exposures.

While most E&S lines reported improved year-over-year results, two outliers were other liability-occurrence and commercial auto.

Over the long term, E&S property lines are expected to outperform casualty segments, although catastrophe exposures remain a concern, Fitch analysts said.

The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  California Utility’s Idle Transmission Tower Caused Deadly ’25 Eaton Fire

California Utility’s Idle Transmission Tower Caused Deadly ’25 Eaton Fire  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  Design the Team Before You Design the Solution: Commercial Trucking Case Study

Design the Team Before You Design the Solution: Commercial Trucking Case Study