The word of the hour was “repositioning” during the earnings conference call for AXIS Capital last week, with the company reporting its bottom line in the black in 2021, following a net loss in 2020.

“We begin 2022 as a stronger company than we were just a year ago,” said Chief Executive Officer Albert Benchimol. “In 2021, AXIS advanced its efforts to reposition the portfolio, manage down volatility and drive profitable growth while capitalizing on a favorable market,” he said.

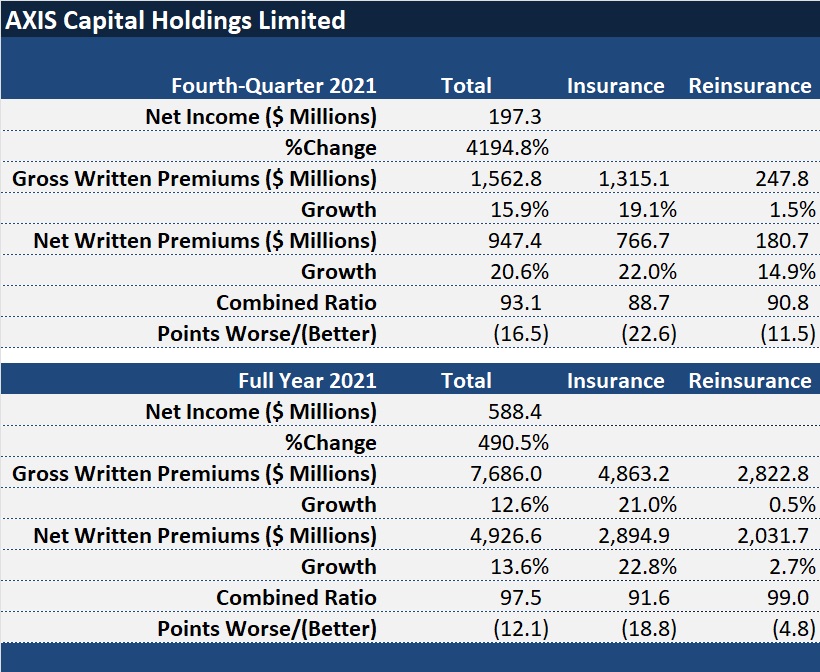

Benchimol attributed the company’s ability to record $588.4 million in net income for 2021 (compared to a $150.4 million net loss in 2020) and 12.1-point improvement in the full-year combined ratio to a “proactive reshaping of the portfolio, reduction of limits and modification of attachment points,” coupled with top-line growth in selected lines that the company believes are adequately priced.

The repositioning is seeing the hybrid insurance and reinsurance company tilt in the direction of insurance.

“We’re confident that the business is on pace to establish its place among the top carriers in the specialty insurance sector,” Benchimol said during his introductory remarks.

On the other hand, Benchimol’s discussion of actions taken during the 1/1/2022 renewals gave conference call listeners a sense of what’s going on in the reinsurance side of the house. In spite of the fact that reinsurance segment combined ratio came in below 100 for 2021 (99.0 to be exact), during the first renewal period of 2022, Benchimol reported that AXIS “took decisive action and reduced our reinsurance property and property-cat premiums by 45 percent.”

2021 milestones for the company described by Benchimol and Chief Financial Officer Peter Vogt included:

- A 10-point reduction in the company’s current accident year ex-cat combined ratio to 88.7—the best since 2007.

- A catastrophe loss ratio that remained flat in 2021, in spite of the industry experiencing a $100 billion-plus cat year.

- Gross specialty insurance premiums rising 21 percent to $4.9 billion in 2021, or up 50 percent since 2017.

- A specialty insurance combined ratio of 91.6 in 2021—the best since 2010.

- A reinsurance current year ex-cat combined ratio of 86.3 in 2021—the best since 2012.

Benchimol said specialty now makes up 63 percent of AXIS Capital’s writings overall, and that by capitalizing on an “already well-established presence in some of the most attractive P/C markets today,” the proportion will rise to 70 percent in short order.

He also offered the company’s view of market conditions in the insurance and reinsurance sectors.

On the insurance side, he said that AXIS Capital’s average rate increase was 14 percent for both the full year and the final quarter, nearly identical to increases the company saw in 2020. “This represents the 17th consecutive quarter of rate increases and the seventh consecutive quarter of double-digit increases,” he said.

“The question on everyone’s lips is how long will it last. Looking forward, we expect that after many years of unsatisfactory performance, the industry will sustain a rational approach to pricing. And there are enough uncertainties and pressures on loss costs and profitability as well as higher reinsurance costs to bear, that we expect disciplined pricing through 2022 and potentially into 2023,” he said.

Albert Benchimol, AXIS Capital

Benchimol’s take on which lines were seeing the biggest rate hikes was generally in line with broker commentary offered late last year. The highest leaps came in cyber, which averaged 50 percent jumps for the year and 80 percent for the quarter, he said, noting that other professional lines saw average rate increases in the mid-teens. Liability, primary casualty and excess casualty are averaging increases in the high-single-digits for the quarter and the low-double-digits for the year, he said. And he said property rate increases were roughly 10 percent for the quarter and the year.

Turning to the reinsurance market, Benchimol agreed with the general consensus that prices are up about 10 percent on property-catastrophe reinsurance, but he stressed that pricing is not uniform. “Lower layers of reinsurance towers and aggregate treaties where supply was more constrained exhibited the strongest pricing increases, especially if they were loss impacted,” he said, putting increases for loss-impacted treaties in the 25-50 percent range.

“Our general view of the reinsurance market is that while it’s still running overall behind primary pricing, the market is heading in the right direction but must continue to do so to adequately compensate reinsurers for the risk and volatility they assume.”

That assessment prompted a later question from an analyst who asked whether reinsurance rate improvements are being offset by higher ceding commissions across the market. “The higher [level of] ceding commissions really relates to the fact that the primaries are delivering good rate and good books of business, and I think reinsurers, including ourselves, when we evaluate those,…look at the total return that’s available to us,” he said, reporting that even AXIS accepted some deals where the business was attractive even though ceding commission went up.

But that wasn’t true across the board. “In many cases, honestly, we felt that the demands for ceding commission increases were too much, and we backed away,” he added.

“Everybody has an appetite and they’ll figure out what they want to do. But one of the things that we are recognizing…is that the reinsurance average rate increases are running behind overall the primary industry. And I think that probably has to do with the fact that there is much greater ease of entry and exits in the reinsurance market than there is in the specialty insurance market.”

Asked about the company’s appetite for cyber insurance business, Benchimol said AXIS Capital has reduced its exposure by about 40 percent since last June. “We’ve made some meaningful changes to our underwriting guidelines,” he added, referring to requirements about cyber hygiene in addition to reducing limits.

The CEO said that price increases are having a beneficial impact on cyber results.

“The truth is that the cyber book we’re writing today is actually making an underwriting profit…It’s not like this is runaway loss costs that are draining the profitability of our company. It’s making an underwriting profit. We just don’t think it’s making this sufficient underwriting profit for the volatility and the capital requirements,” he said.

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention

The Price of Loyalty: How Higher Premiums Are Reshaping Carrier Retention  Rising Pro Boxer Killed While Riding Bicycle in Bizarre Texas Crash

Rising Pro Boxer Killed While Riding Bicycle in Bizarre Texas Crash  Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses

Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses  Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It

Let’s Talk About Insurance Distribution Before ChatGPT Disrupts It