Although it wasn’t the headline of a commercial insurance broker’s market pricing report last week, the report’s observation that “commercial auto liability coverage rates are starting to flatten” is telling.

Robert Meyers, senior vice president and Property & Casualty Leader for USI Insurance Services, shared the insight about an insurance product line that had projected price hikes of anywhere from 5-10 percent at midyear (for fleets with good loss history) in the executive summary of the firm’s “2022 Commercial Property & Casualty Market Outlook.”

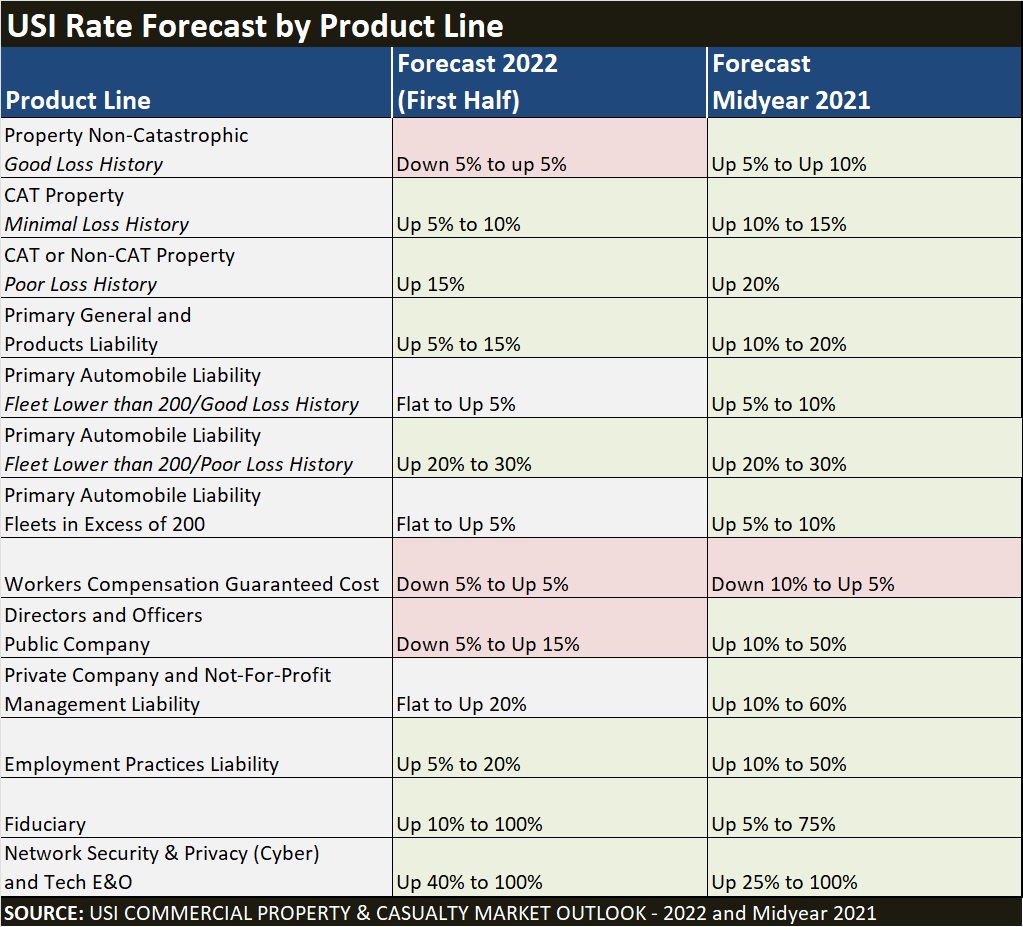

The trend for commercial auto pricing exemplifies a general trend for many of the 31 commercial insurance product lines analyzed throughout the report—a trend of increased capacity helping to improve the insurance pricing situation from the insurance buyer’s perspective.

In fact, 14 of 31 different product line categories tracked by USI now have a flat rate change as a possible outcome for buyers in 2022, compared to just seven based on a similar type of forecast published in June.

First-half 2022 and midyear 2021 forecasts for a dozen product lines tracked by USI are shown below.

“Commercial automobile liability coverage rates are starting to flatten out, due to the reappearance of insurers that have been dormant, along with the entrance of new telematics and usage-based insurers,” the 2022 report says.

“Insurers are exceptionally competitive and are heavily pursuing accounts that deploy the use of technology and intensely focus on safety. ”

Still, however, underwriters continue to heavily scrutinize these risks, and insurance prices for fleets with less than 200 vehicles and poor loss histories haven’t changed from midyear. Those are still seeing rate hikes in the 20-30 percent range, according to the report.

The report notes that commercial auto fleets with adverse risk profiles, while still experiencing higher pricing, “can secure more favorable terms because of increased deductibles, self-insured retentions (SIR), and alternative program structures”.

Overall, across more than half of the product lines for which USI provides a pricing analysis in its forecast reports, “an influx of new insurance carriers has helped expand overall insurance market capacity.”

“Legacy markets, which have been deploying capital and surplus to compete for new business in certain lines of coverage, are also increasing capacity,” Meyers noted in the executive summary.

Possible rate decreases are now indicated for five product lines. Not surprisingly, one of those lines is guaranteed cost workers compensation, which has remained soft in recent years. But for workers comp, the most favorable projected rate change for 2022 (from a buyer’s perspective) is a 5 percent decrease, which is less favorable than the buyers’ best-case 10 percent decline that USI professionals forecast in the second half of 2021.

The language of the report doesn’t suggest too many reasons for the lower magnitude of price declines going forward, other than to note that combined ratios reported by the National Council on Compensation Insurance have been ticking up—rising from 85 in 2019 to 87 in 2020, and expected to be still higher when all the numbers are tallied for 2021.

Worker comp is one of only five product categories moving in a less favorable direction for buyers, according to USI’s forecast. Others are cyber (network security), technology E&O, fiduciary and environmental contractors pollution.

For public company D&O, a movement of price changes in the other direction now suggests a best-case forecast of 5 percent rate drop, driven by softening excess layers. The 2022 forecasted price changes in the excess layers range from 10 percent price drops to 10 percent hikes, according to a summary table in the report. For the primary layers, USI forecasts a range of rate changes extending from flat renewals (no change in rates) to increases of 20 percent.

Beyond the emergence of new capacity targeting excess layers of coverage for public company D&O, USI attributes improvements in the pricing forecast for buyers to a significant decrease in federal securities class actions in 2021.

Along with the rate comparisons, the report provides added information from USI practice leaders for individual lines. Among the insights are these:

• For property, USI expects opportunities for carrier profitability in the first half of 2022, attributing this to rate and deductible adjustments put in place since 2019, especially for lower hazard occupancies and non-catastrophic regions.

“The current environment and opportunity to shrink CAT portfolios will create competition among carriers trying to attain their 2022 premium growth targets. This, combined with a slowing impact of COVID-19 and strong investment opportunities, allows carriers to be aggressive on quality risk with quality data,” the report says, suggesting reasons for improved pricing in terms for buyers of non-cat property insurance

• For environmental, USI notes that the marketplace continues deal with the exits of “two long-time industry giants, AIG and most recently Zurich,” in recent years.

“While the transition to other carriers has gone smoothly, structuring a large amount of capacity is not as easy,” the report says.

“In another trend expected to continue into the foreseeable future, insurers are pulling back coverage for PFAS,” the report says, observing that many carriers are “automatically including broad exclusions for cleanup and third-party coverage.”

• For both the cyber and tech E&O product lines, the report provides separate 2022 forecasts for “optimal” and “less optimal” risks.

With ransomware attacks continuing to challenge cyber insurers in the second half of 2021, USI professionals witnessed carriers tightening terms and availability of some coverages for the “less optimal” buyers that could not demonstrate strong risk controls and overall cyber hygiene. Those buyers are now facing the price hikes of 50 percent or, in the worst case, a doubling of insurance rates.

“We saw a surge in insurers’ probes into information security controls and practices” in the second half of 2021, the USI report says, adding that optimal risks face rate increases of at least 40 percent in 2022 (compared to 25 percent at midyear 2021.

• Fiduciary liability insurance is another product line for which some insureds could see rates double. Here, the report points to the impact of excessive-fee litigation, which drove double-digit percentage premium hikes in the latter part of 2021. Carriers are also pushing for significantly higher retentions as they look “to insulate themselves from claims alleging breaches of duty in the management of investment-related and recordkeeping fees,” the report says, forecasting that some leading carriers will seek retentions in excess of $5 million in 2022.

• For employment practices liability, some buyers—those without poor claims history or major changes in exposure due to acquisitions or layoffs—were able to renew their programs with single-digit increases. “Insurers were willing to compete on EPL renewals if the insured’s business conditions were improving, an effective return-to-work transition plan existed, and employment policies were keeping up with newer areas of exposure (e.g., gender identity discrimination, medical marijuana uses, and claims regarding social media use, etc.).

Looking to 2022, USI expects moderate EPL insurance rate increases to continue, and the report said that increased focus on retention structures is likely—especially in certain states, like California.

Another situation to watch: “In the face of resistance to vaccine mandates in the U.S., there may be an increase in retaliation and discrimination claims under the Americans with Disabilities Act and Civil Rights Act of 1964 (specifically, for religious discrimination).”

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Bring It On: AI Strategy Sways Underwriter Choices of Employers

Bring It On: AI Strategy Sways Underwriter Choices of Employers  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment

Key to Customer Loyalty in Claims Journey Mixes AI and Human Judgment