While events like Hurricane Ida and a Texas winter freeze demonstrate wide-reaching impacts of climate change to all but ardent deniers, even insurers and reinsurers may not fully appreciate all the risks, a new report suggests.

Among the underappreciated facts about climate change: Along some parts of the U.S. Eastern seaboard, events that used to be thought of as 1-in-100-year hurricanes will have a 40-plus percent chance of occurring sometime between 2031 and 2050, according to the report, “The Journey To Net Zero: An Insurer’s Guide to Navigating Climate Risks and Opportunities.”

Climate change risk consists of three broad interrelated categories of risk—physical, transition and liability risks—authors of the report published by global advisory Willis Towers Watson and investment management firm Wellington Management reveal.

The risks are not only interrelated—with acute physical risks (hurricanes and floods) and chronic ones (like droughts and rainfall) fueling transition and liability risks, such as carbon emissions regulations and legal actions brought about by those suffering loss or damage from climate change. They are also cumulative, the report points out, providing an eye-opening example of probabilistic math that some may miss even when focusing solely on the physical risk component.

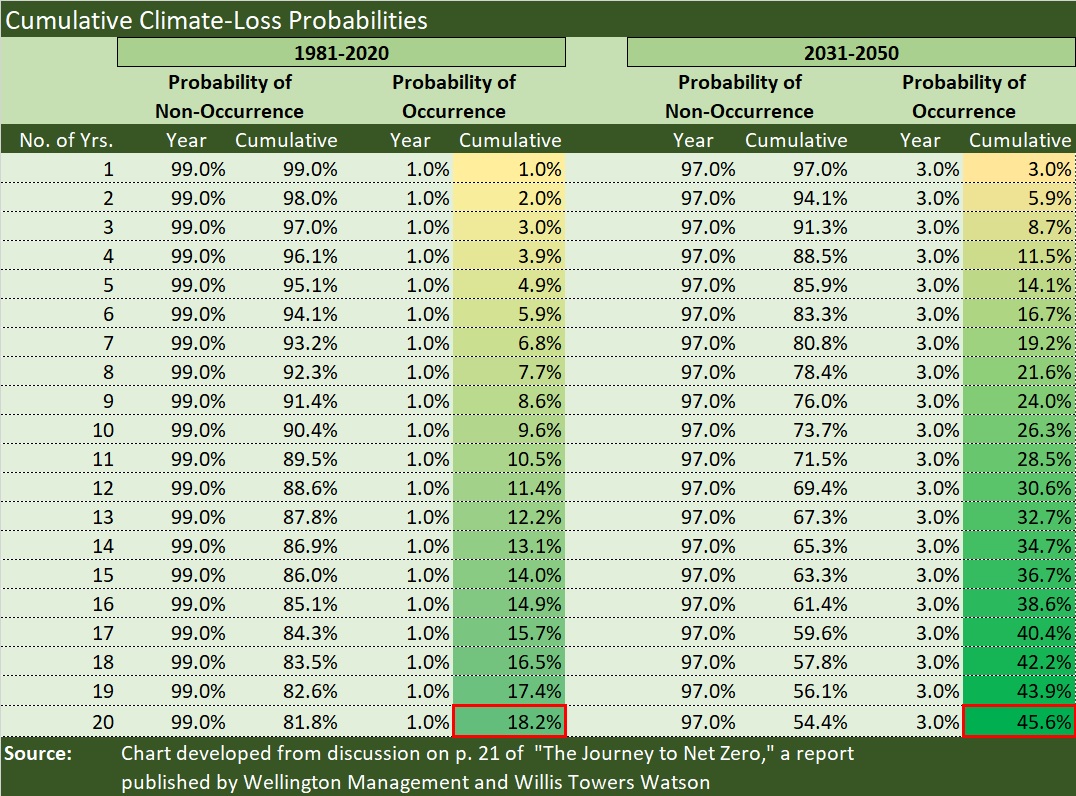

First ignoring the impact of climate change, the authors describe how to calculate the probability that a 1-in-100-year event will occur over at some time during a 20-year period.

By definition, 1-in-100 year weather events have a 1 percent probability of occurring in a single year.

In other words, the probability of such an event not occurring in a single year is 99 percent.

Assuming that event occurrence is independent from one year to the next, then over 20 years, the probability that a 1-in-100-year event will not occur is 81.8 percent (.99 x .99 x .99…x .99, where .99 is multiplied 20 times and the result expressed as a percentage).

That means the chance that such an event will occur during that two-decade span is 18.2 percent (100%-81.8%), the report says.

But it turns out that the probability of weather events that used to be thought of as “1-in-100-year” weather events is rising.

Working with Woodwell Climate Research Center, which used scientific models and climate data, Wellington Management found that events that were 1 percent events from 1981-2000 could be 3 percent probability events in the 20-year period starting in 2031. A map of the U.S. displayed in the report, with areas color-coded to represent varying single-year probabilities for extreme hurricanes at different location, shows the tips of Florida and Texas colored blue—corresponding to the 1 percent probabilities typically assumed. But the Southern-most coasts of Alabama and Mississippi and the Eastern shores of North Carolina are colored bright red, corresponding to single-year event probabilities of between 3.0 and 3.4 percent for those places within 2031-2050 time frame.

Repeating the cumulative probability math discussed for a 1-percent single-year probability with 3 percent assumed instead works out to a 45.6 percent cumulative probability over the 20-year span. And assuming 3.4 percent per year gives a 20-year cumulative probability of nearly 50 percent.

In other words, “certain already vulnerable regions will face a 40-60 percent chance of experiencing a devastating hurricane between 2031 and 2050,” the report says.

“The continued mischaracterization of rare climate events as one-time occurrences rather than as part of a changing pattern may be the reason why climate change often remains abstract, hampering protective behavior, policy change and asset repricing,” the authors wrote in the report.

But that analysis is just one page of a 37-page report that focuses more on interrelated risks of transition risks and liability risks than on physical risks by themselves. “The increasing volatility of loss-causing climate-related events, along with growing financial risks to assets in investment portfolios, present a dual threat,” the report says.

“To better understand the multi-dimensional nature of climate risk and how it impacts different parts of the business, the insurance industry needs to up its game and be more strategic,” said Adhiraj Maitra, one of the report co-authors and director at Willis Towers Watson, in a media statement about the report. “This means taking a whole balance sheet view of the risks and opportunities,” he said, introducing the idea that insurers and reinsurers have to develop scenarios of temperature change over a given time horizons, considering optimistic and pessimistic assumptions about worldwide paths (orderly vs. disorderly) to reaching climate goals.

Each category of risk can impact both sides of the balance sheet—and should influence strategic business decisions about product development, capital management, investments, acquisitions and divestitures, the report stresses, going on to outline an strategic approach to climate risk and resilience that starts with understanding baseline enterprise risk and then developing climate scenarios that insurers and reinsurers can integrate into their risk models.

In the section of the report that deals with scenario building, Willis Towers Watson and Wellington Management review details of some of the climate scenarios that have been published by regulatory, academic and industry-led organizations. For example, the Intergovernmental Panel on Climate Change, created by United Nations, in its most optimistic scenario assumes 1.5°C additional warming by 2100 relative to pre-industrial levels and CO2 emissions reaching net zero (emissions produced equal emissions removed) by mid-century. A “middle-of-the-road scenario” assumes 3°C more warming by 2100 and global emissions peaking by mid-century, while a truly pessimistic one assumes no mitigation and more warming.

“Even if the world stopped producing carbon emissions today, projections indicate the temperatures will still rise 1.5°C by 2100,” the report asserts.

The report also summarizes current regulatory approaches in different parts of the world with respect to scenario building and climate risk disclosure.

Gaining a clearer understanding of climate risks and building scenarios are just two of the eight key challenges that insurers need to address if they are to better appreciate the severity and more accurately reprice these risks, and ultimately play a larger role in helping society mitigate the effects of climate change, according to the report. Other items on the to-do list outlined in the report include stress testing asset portfolios, developing climate-aware investment strategies, and—importantly—holistically integrating asset and liability strategies.

There is a lot to consider as insurers and reinsurers work to develop their own views of risk in line with their baseline underwriting and investment portfolios, and to translate climate risks under different scenarios into adjustment factors for models they use today. At one point, for example, the report talks about indirect climate risks for insurers invested in industries like auto manufacturing, semi-conductors, construction, or other industries that heavily rely on water. Water scarcity could mean higher operating expense, lower output, and ultimately a drag on GDP growth.

Another indirect risk relates to migration, the report says. Wellington’s climate research team believes that “climate migrants will abandon vulnerable rural area for urban ones,” driving economic consequences. Some countries could see sovereign debt downgraded as a result of climate risks, and higher borrowing costs could ultimate lead to further impacts—unemployment, inflation, social unrest.

Throughout the report, the researchers also describe ways in which insurers can identify opportunities related to climate change—for example, overweighting assets that contribute to the low-carbon transition (renewable energy, large-scale battery storage, water management, electric network utilities).

An early section of the report also reviews climate adaption projects already underway, such as land creation at the Manila Airport in the Philippines, the development of sponge cities in China begun over a decade ago, and the economic and societal benefits of increased mangrove forest cover.

The report concludes with more than a dozen questions to think about. Among them are:

- Who is responsible for assessing and managing climate-related risks?

- Does the board have explicit oversight?

- What are you doing to mitigate your emissions?

- What products or services do you or could you offer to benefit the transition to a low-carbon economy?

Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz