A proposal making rounds in the U.S. House of Representatives to “establish a Pandemic Risk Reinsurance Program” would involve “shared public and private compensation for business interruption losses resulting from a pandemic or outbreak of communicable disease,” according to a May 11 discussion draft reviewed by Carrier Management.

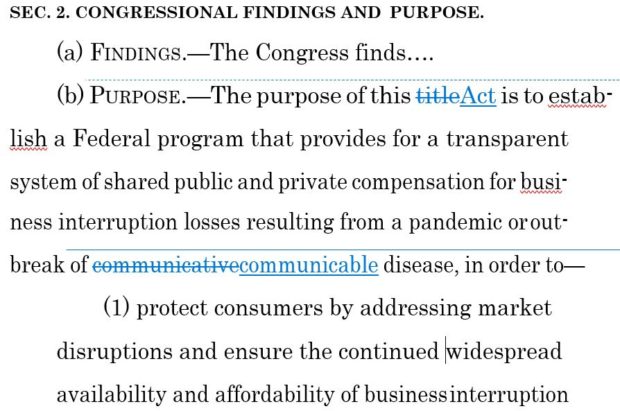

Losses from “a pandemic or outbreak of communicative disease” were covered in an April 3 draft (emphasis added).

The correction of a minor spelling mistake in the more recent version of a discussion draft of the Pandemic Risk Insurance Act of 2020 isn’t the only one we spotted in comparing the two documents.

The biggest change is an increase in the annual aggregate cap on losses to $750 billion from $500 billion

Others changes include:

- The definition of a covered public health emergency. While both drafts define it as an emergency declared under the Public Health Service Act, the earlier draft also requires a major disaster to be declared by the president; the later one requires that it is certified by the secretary of Health and Human Services as a public health emergency.

- The requirement for a participating insurer to pay premiums into a risk reinsurance fund—based on actuarial cost—is gone in the May 11 draft.

- Language relating to event cancellation insurance have been added to definitions of property/casualty insurance and business interruption insurance.

- The later draft adds a provision for terminating the program in seven years.

What hasn’t changed?

In general, both drafts differ from the Terrorism Risk Insurance Act in that insurer participation is voluntary. No losses are paid under the program described in either draft until aggregate industry insured losses exceed a $250 million aggregate trigger. The federal share of losses is 95 percent of insured losses above each insurer’s deductible defined under the program. The insurer deductible is defined as “the value of the participating insurer’s direct earned premiums during the immediately preceding calendar year, multiplied by 5 percent” in both drafts.

In mid-April, Rep. Mike Thompson, D-Calif., introduced a different bill, the Business Interruption Insurance Coverage Act of 2020, requiring insurers who offer business interruption insurance to cover pandemic interruptions and nullifying pre-existing exclusion unless insureds authorize reinstatements of exclusions in writing or fail to pay increased premiums charged for the coverage.

Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz