In an initial test of its new innovation assessment scores, AM Best found that only 1 percent of rated property/casualty insurers merit scores high enough to categorize them as innovation leaders, according to a recent report.

The special report, “AM Best Incorporates Innovation Into Its Rating Process,” shows similarly low levels of leaders among life and annuity insurers while finding that global reinsurers and health insurers have the highest levels of innovation.

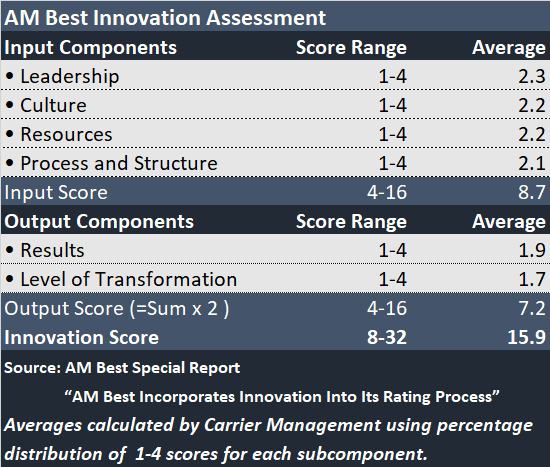

Insurance organizations with scores of 28 or better—out of a maximum of 32—are categorized as innovation leaders in A.M. Best’s scoring model.

- The assessment has two main components—and input score and an output score.

- There are four subcomponents of the input score—assessments of innovation leadership, culture, resources and process—each of which receive a score of 1 through 4 (higher is better), for a maximum input score of 16.

- The output score has two components—one measuring results and the other, the level of transformation—with each also graded on a 1-4 scale. The output score, however, is given double weight in the overall scoring assessment, making the maximum output total 16.

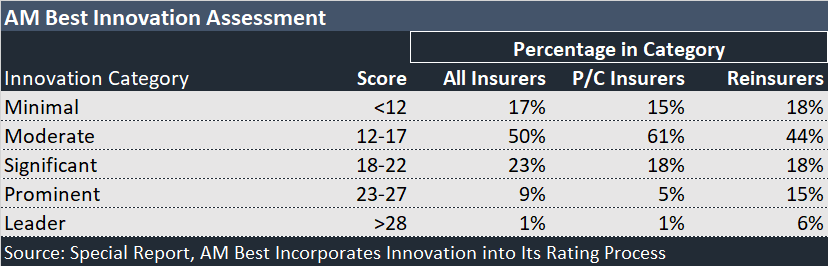

AM Best categorizes insurers and reinsurers receiving overall scores less than 12 in the “minimal innovation” category. The next lowest category is “moderate,” which indicates those insurance organizations with total scores in the 12-17. According to the report, 50 percent of all insurers and 61 percent of P/C insurers fall in the moderate category.

On the other hand, 21 percent of reinsurers wound up in the two highest categories—prominent and leader—with scores of 23 or better. Six percent of reinsurers are actually categorized as leaders in Best’s initial assessment.

Explaining the presence of more innovation leaders among reinsurers, health insurers and auto insurers, the report noted “the relative simplicity of their underwriting and claims demands” —and suggested that this simplicity allows for more scalability and replication of successful innovation initiatives. Specifically for the reinsurers, the report notes that ceding companies manage much of the complexity of the underwriting and claims functions

Other factors moving global reinsurers farther along in innovation efforts include a more open regulatory environment, more recent startups (with fewer legacy systems and less “entrenched operating norms” allowing more innovative cultures), and the need to respond to nontraditional competitors from the capital markets through partnerships.

InsurTechs factor into reinsurer innovation as well, with reinsurers buying or partnering with InsurTech startup intermediaries to attract desired business “more quickly and at much lower ceding commissions than current arrangements with reinsurance brokers…and ceding companies.”

InsurTechs: Disrupters Need to Show ‘Results’

While relationships with InsurTechs helped to boost overall scores for reinsurers and personal auto carriers, AM Best said that InsurTechs themselves lag on one particular component of its innovation scores—an assessment of measurable “results”—the second piece of the output score.

“These companies generally had high scores across the four input components, along with higher transformation scores.”

Scores for “level of transformation” seek to measure whether a company’s innovation initiatives are unique, industry-leading or ground-breaking ones that create value, improve customers experience and create superior business models. “Preliminary testing identified some market disrupters,” Best said, referring to InsurTech startups.

With output scores for “results,” AM Best analysts attempt to capture whether innovation initiatives produce competitive advantages and measurable tangible impact. InsurTech results scores were “generally at the lower end and didn’t provide rating enhancement,” the report says.“Actualizing innovativeness takes time. A high degree of innovativeness is not a rating positive until a company can achieve concrete results, such as greater market share or better competitive position,” the report continued.

Industry Results

Across the insurance industry, the report notes that AM Best’s initial innovation scores were in line with what was expected when the rating agency set out to develop the scoring formula. The challenges inherent in producing measurable results are not limited to a specific type of insurance entity, the report said, noting that industrywide average scores for the output components were generally lower than input scores across the board. The gap between input and output scores, however, does shrink as insurers and reinsurers become better innovators. In fact, for leaders, the average output score of 14.6 (out of a maximum 16) is only 0.7 points below the average input score of 15.3. On the other end of the spectrum, insurers evidencing minimal innovation had output scores average 4.1, or 1.1 points lower than the average input score of 5.2.

The report also notes that the rated entities reviewed for the report generally had the best marks for the leadership piece of the input score, with 5 percent of companies in P/C, life, health and reinsurance sectors overall garnering the highest grades (the 4s) and 11 percent getting the lowest grades (the 1s). The culture subcomponent of the input score had the second-best results with 3 percent of companies getting high grades (of 4) and 14 percent getting the lowest grades (the 1s). Explaining why cultures aren’t changing as fast as leadership mindsets, the report notes that the industry’s mission of risk management and mitigation makes it “conservative by design.”

In assessing culture, AM Best analysts consider whether companies have specific incentives in place for innovative employees and how companies handle—and gain knowledge—from innovation failures. While some companies don’t have failures because they lack innovation projects to begin with, AM Best analysts noted that many other companies were “unable or unwilling” to talk about past failures, leading to lower culture scores.

Credit Ratings and Innovation Assessments

In an earlier article they wrote for Carrier Management, AM Best representatives noted that few, if any, movements in overall financial strength ratings are expected from innovation assessment scores.

Although innovation is now an explicit component of the Business Profile building block of an AM Best rating (which also looks at market position, product/geographic concentration, pricing sophistication and other business characteristics), AM Best will take into account the company’s innovativeness relative to its particular circumstances as part of the credit rating exercise. (So, for example, a company with “significant” levels of innovation specializing in a line of business where innovation is “moderate,” could receive credit for positive innovation impact.)

The innovation assessment score by itself, however, is an absolute assessment. In other words, all companies are subject to the same evaluation criteria (described throughout this article), regardless of line of business, location or market position. (See also, Scoring and Assessing Innovation,” on AM Best’s website for a full discussion of the evaluation criteria)

Still, AM Best has said in the past that there will likely be a natural correlation between the absolute innovation assessment scores and favorable business profile assessments. In fact, this is borne out in the report, which also shows companies with best operating performance having better innovation scores—and, in fact, that the highest overall financial strength ratings line up with higher levels of innovation.

The report shows that insurers and reinsurers with “superior” financial strength ratings have average innovation scores of 19.8, compared to average scores of 9.4 for the weakest insurers financially.

In addition, while only 30 percent of rated companies with “superior” financial strength ratings scored in the “moderate” or “minimal” categories on their innovation scores, 80 percent of the weakest insurers fell in these low categories of innovation scores.

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz  AXA XL to Acquire S-RM

AXA XL to Acquire S-RM