The once reliable cycle consisting of a short but severe post-catastrophe hard market followed by a gradual easing of insurance prices is officially a thing of the past, a major broker said in a recent commentary.

The fundamental question of whether such cycles continue to be the main economic force driving our industry has been answered, said Joseph Peiser, head of Broking for Willis Towers Watson North America, introducing the findings of Willis Towers Watson’s 2018 Insurance Marketplace Realities— Spring Update report in a video commentary.

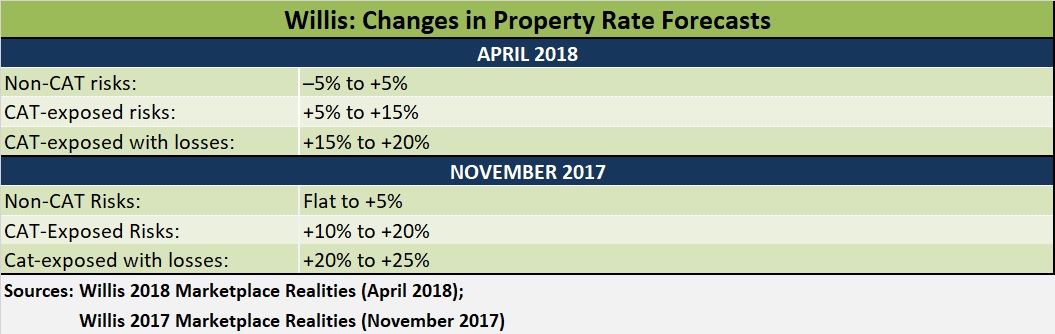

Among the key findings: Commercial property insurance rate increases are easing off the initial spikes that followed record natural catastrophe losses last year. Despite the storms and fires of 2017, even rates for buyers in cat-exposed areas that experienced losses have come down since WTW’s November forecast.

Not only are the property rate increases already beginning to moderate, but WTW is also witnessing decreases again becoming possible for better risks.

A “resilient, capital-rich industry passed the test of 2017,” Peiser said in the video. “The swiftness with which the industry recapitalized was something of a marvel, especially to those of us who have lived through past insurance cycles and seen plenty of chaos, carrier failures, pricing upheavals and the creation of new insurance startups,” the accompanying report noted.

Insurers “can’t rely on the old market cycle to produce long-term gains. They’ll have to increase their income by providing better, more valuable products—and do so more efficiently,” Peiser said.

In the short run, there will be price hikes in property, but not nearly as much as previously thought, Peiser noted. “In the long run, we see an insurance market that will continue to attract fluid and plentiful capital, which will ultimately limit price increases,” he said.

Beyond Property

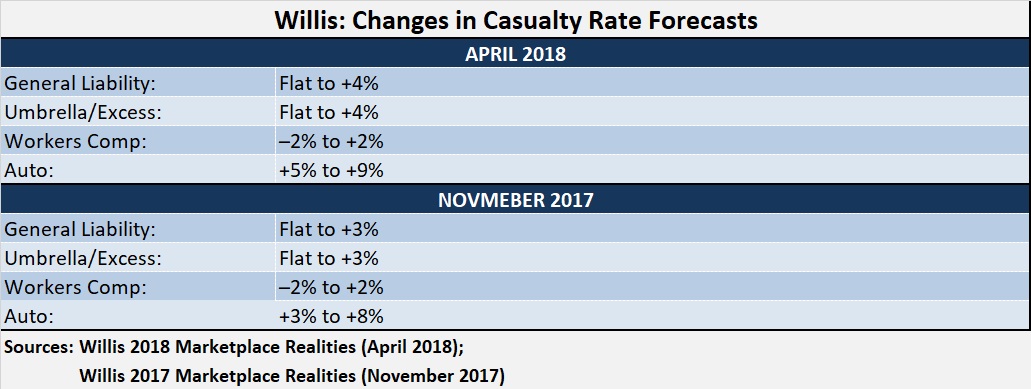

While many thought that the property catastrophes would also have an effect in the casualty market, WTW has not seen widespread increases in general liability and excess casualty rates to date either. Buyers will experience incremental upward pressure in these lines, with the April forecast reflecting a slight uptick from the price predictions offered last fall.

Steeper increases are in store for auto liability. Ongoing market challenges exist for auto, and two years of steady price increases have not kept pace with loss trends and adverse developments, WTW said, upping the forecast to rate hikes of 5-9 percent in the April report compared to 3-8 percent in November. “And some buyers may even see double-digit increases.”

While cyber has proven almost event-proof, as well, the report does note that one line is seeing a market turn: environmental. In fact, “the environmental insurance market is experiencing its first hardening in over a decade.”

A key factor impacting environmental has been loss-driven reductions in underwriting appetites for indoor air quality risks and known conditions. Market reactions to the retrenchment of one large player in the pollution legal liability market—AIG—are also changing.

The giant commercial carrier is entering a third year of nonrenewals, the April report notes. And while the November 2017 WTW report noted that other insurers were competing on pricing for displaced AIG business, the April report says competitors have become more cautious “based on their assessment of this portfolio’s performance for the first two years since AIG’s exit.”

Putting all the factors together, WTW now expects site pollution liability increases in the 10-20 percent range, up from a range of flat-to-down 10 percent cited in the decreases that were cited in the prior report.

In the cyber insurance market, even though global ransomware and extortion claims propelled costs skyward, new capacity continues to keep the marketplace largely competitive, according to the latest WTW market report. The range of rate changes in the pricing forecast here remains –3 percent to +5 percent for organizations without claims or recent incident. The report notes, however, that underwriters “are growing increasingly sophisticated in their underwriting.”

Cyber “insurers have tightened pricing and increased self-insured retentions and deductibles for companies that have not addressed vulnerabilities. Where organizations have demonstrated increased levels of security and internal policy controls, underwriters have offered premium decreases.”

The cyber section of the WTW report also notes that some recent large-scale outages have prompted underwriters to use a cautious approach in offering system failure and contingent business interruption coverages. Buyers “should be prepared to demonstrate their resilience,” the report suggests.

Other lines with noteworthy commentary and changes:

• Employment practices liability insurance: While EPLI’s range of rate changes remains at low single-digit increases or flat overall, the April report makes special note of media and entertainment clients, expected to break away from other risks with 15-30 percent EPLI increases, a consequence of the surge of sexual harassment allegations facing them in the wake of the #metoo movement. In general, for all clients, “corporate culture will be more important than ever in the underwriting process. Expect increased scrutiny of internal policies and procedures regarding sexual harassment and gender-bias claims,” the report advises insurance buyers.

There are other issues on the horizon in the EPLI line, according to the report, which also notes potential future activity from the plaintiffs bar in two areas that could impact both insureds and their carriers: conflicts over online hiring practices and biometrics. While only three states have enacted biometric privacy legislation, the Illinois law, which requires employers to provide notice and obtain written consent before collecting biometric data, has prompted a surge of class action claims filed against employers.

• For D&O, ranges of rates moved upward a bit, with a previous expectation that 2018 rates could decline as much as 7 percent moving to a range of -5 percent to +5 percent. For public company excess layers, WTW expected declines ranging from 5-15 percent when the forecast was published in November last year. The April update moves the range to down 10 percent on the low end but indicates possible increases up to 5 percent on the high end.

“Leading insurers are exhibiting market discipline” across the D&O subsectors, the report suggests. Rates will continue to firm—less soft, but not hard—except where still-ample competition sees this firming as an opportunity to displace a competitor,” the report says.

• Health care professional: The April update makes special mention of rising claims frequency and severity in the long-term care and senior living facilities sectors. The claims are putting tremendous upward pressure on this line of business, and some carriers have exited the market due to adverse underwriting performance, the report notes, forecasting insurance price hikes in the 5-20 percent range.

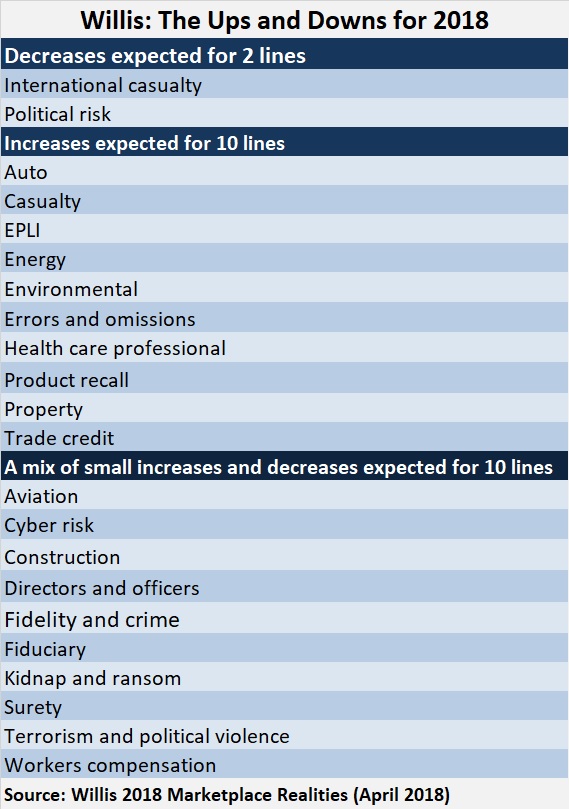

In all, tallying up the expected ups and downs, though ranges of price increases have come down, WTW only flags two lines with price decreases expected—international casualty and political risk—with increases still expected in 10 other lines, such as auto, environmental and health care professional, and a mix of smaller price changes in remaining lines.

Source: Willis Towers Watson

AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  Will AI Be the End of Insurance Agents?

Will AI Be the End of Insurance Agents?  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?