While Zurich Insurance Group’s new chief executive officer believes the insurer is on the right track in terms of growth and profit, the organizational structure remains too complicated, he suggested during an investor conference yesterday.

“Zurich is world famous for [a] complex organization—for having…triple, even four layers of matrix” on its organizational map, Mario Greco said, during his first earnings conference as a Zurich executive with analysts. “I definitely have in mind that the organization has to be simple, and has to promote accountability and ownership of results,” Greco said, responding to an analyst who suggested in posing the question that the present structure had some disjointed features.

Greco said he is discussing ways to simplify and streamline the organization with the board and with Zurich colleagues. “When we will have a decision…, we will communicate and you will know it,” he said.

The answer to the analyst’s question was one of the few hints Greco about changes that might be ahead. In remarks prior to the question-and-answer session, the new CEO discussed his priorities and activities to date since joining the company. He also promised to develop—and provide full details of—the go-forward strategic plan in November.

For now, he said that first-quarter results—an overall operating profit of $1.1 billion and net income of $875 million—were a clear “step in the right direction” for a group which had suffered a steep profit decline last year. The decline was mainly driven by operating losses in the General Insurance segment in the second half of 2015, and Greco said that building back confidence is a key goal.

He said his first priority has been “to develop a deeper understanding of challenges and opportunities” ahead for Zurich by meeting with key business leaders and employees internally, and with brokers and customers. His initial assessment in these early days, he said, is that the book of business is “fundamentally sound.” In addition, “reserves are adequate, capital is strong and the brand is really strong,” he said.

“Confidence is vital to our success and can only be achieved through transparency, through clear communication, and by delivering on the group’s strategic objectives,” he continued, laying out his second order of business. “Today’s results… provide early evidence that measures that we started last year are improving the performance of General Insurance. Also the continued progress in Global Life [insurance] and Farmers is visible and supporting the group results,” he said.

With further improvements expected throughout the year, and most particularly in the second half, Greco said his third priority is positioning Zurich for the future. “That begins with shaping a clear and simple group strategy for the next years, and a strategy that will differentiate us among our competitors in the eyes of the customers,” he said, promising to provide full details on Zurich’s Investor Day, scheduled for Nov. 17.

Greco provided few other hints of things to come, although when an analyst asked about whether he might consider changing the mix of business to be heavier on the personal lines, he did not discount the possibility.

Prefacing his answer by stressing that he was sharing very early thoughts, Greco said, “I do think having a bigger share of retail business would be helpful. The question is more [about] how to do it …

“I am keen to find ways to grow more on the SMEs and the retail components of our book… But I’m not yet there where I have planned programs and I can discuss them with any of you,” he said.

Asked once again about organizational structure, this time by an analyst who noted a recent change in leadership at Zurich’s operations in Germany, Greco said that while the change preceded his first day at Zurich, he fully supports it. (The change involved combining life and nonlife divisions under one CEO, who was formerly head of the German life business, according to an online translation of a German press release from late February.)

“In Germany, Zurich used to have three different CEOs. This has been unified under one country CEO. This allowed [us] not just to simplify…but also to unify functions and priorities in the market,” Greco said, noting that similar moves are underway in Italy and “will likely continue in other countries.”

“It is a trend. It makes sense. It is how the market is organized itself and it fits well with the customer organization and mindset,” he said.

Confidence Building Results

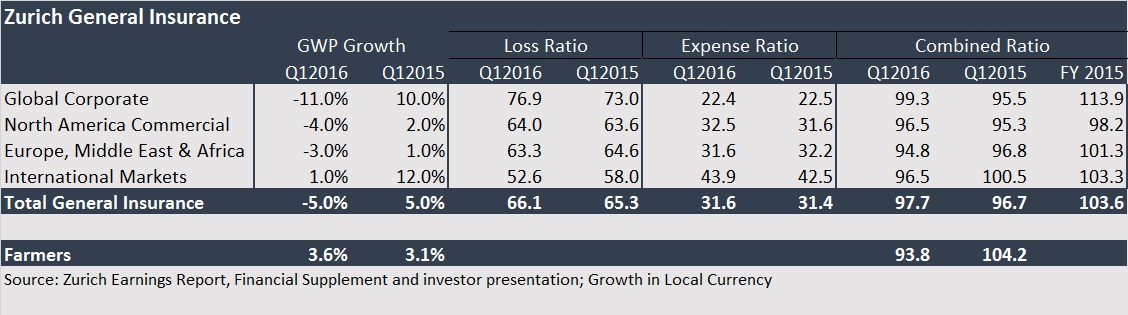

One of the highlights of the first-quarter 2016 earnings report was a General Insurance combined ratio of 97.7. “That’s better than we’ve seen for almost 12 months now,” said Chief Financial Officer George Quinn on a video posted on Zurich’s website, highlighting an improved loss ratio as a key driver.

While the result was actually just about a point higher than the first-quarter combined ratio in 2015, it was a clear improvement over the full year 2015 result of 103.6. Executives pointed to a tiered approach to underwriting, with double-digit rate hikes applied to the worst performing tiers producing significantly reduced retentions for the least desirable business.

Favorable prior-year development of just under 1 point for Global Corporate and just over 1 point for North America Commercial also explained part of the improvement.

Still analysts questioned Quinn about the adequacy of reserves—a nagging problem for Zurich in the past, particularly in last year’s third quarter. The analysts also raised questions about expense ratios that might not come down—even amid cost cutting actions announced last year—because premiums are declining at the same time. And they asked about the premium declines specifically.

Quinn noted that the 5 percent drop in premiums for the General Insurance book was within expectations, referring to previous guidance a premium volume decline in the mid-single-digit range. There has been no change in cost savings targets—or a goal of $1 billion in savings annually by 2018, he added. “Under Mario’s leadership, we’re looking again at efficiency and expenses. It’s an increased focus for us,” he said, noting that being more efficient means “creating more room to invest for the future.”

Greco reinforced the idea that top-line declines are not necessarily unwelcome. “One of most important corrections taken at the end of last year, and I’m fully supportive of that, was abandoning strategy called Amalfi [SIC], which was a growth strategy, and going back to the older principle of underwriting discipline and underwriting focus. So, you underwrite for profit. You don’t underwrite for size, for premiums.

“This is what we’re doing [and] we will keep doing that. And the growth [rate] will just be a consequence of it. And if it is negative, be it.

“There is no way in which we can solve an expense ratio issue by growing the size. If expense ratio worsens, we will take more actions on costs but we will not derogate to underwriting discipline,” he said.

As for loss reserves, Quinn said he is comfortable with reserve adequacy, focusing some of his comments on the previously troublesome U.S. book. Issues emerged last year emerged in the liability portion of the book, particularly the auto liability segment, he said, noting, however, that workers compensation represents 25 percent of the premium volume. For workers comp, doing peer comparisons of metrics like IBNR (incurred-but-not-reported reserves) to incurred losses or implied 10-year to ultimate loss ratios, demonstrates to him that Zurich is more conservative than peer group. “If we moved to peer group or industry levels, that would imply a reasonably significant release,” he said.

The executives also reported results for the Farmer Exchanges, noting that while premiums grew by 4 percent, the combined ratio deteriorated—a combination of losses from hailstorms and unfavorable trends in auto insurance industrywide.

Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America

Zurich CEO: El Niño May Mean Fewer Hurricanes, Insurance Losses in North America  Design the Team Before You Design the Solution: Commercial Trucking Case Study

Design the Team Before You Design the Solution: Commercial Trucking Case Study  Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty

Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t