A rising tide carries all boats. That rings true currently in commercial insurance. Carriers have broadly brushed aside concerns about geopolitics, inflation and natural catastrophes and reported positive 2022 underwriting results. Leaders talk optimistically of the pivot to growth and the viability of “writing the market” at present terms.

Executive Summary

Although rates are hard, combined ratios and returns on required capital are still underwhelming. Here, Tony Buckle and John Carolin, partners at UWX, and Mehmet Ogut, director, Deloitte Consulting, examine the conundrum—and a related disconnect between underwriters and actuaries as well. They suggest that underwriting discipline actually isn’t improving. There are growing losses in the market, while attention is being drawn to top-line growth. Underwriters need to look at exposures and take actions to tighten coverage, proactively aligning with reserving actuaries to ensure agreement on how such changes impact ultimate loss ratio calculations.And yet…after five years of substantial price increases across commercial insurance, combined ratios in the low to mid-90s feels underwhelming. Q1 results too are a mixed bag. Why is all that payback from insurance buyers not translating into significantly better combined ratios and returns on required capital for insurers?

At one level, the answer is that the market is playing catch-up. It is now clear that across the market, risks were technically underpriced at the nadir of the soft market in 2017. It is also clear that the market had underestimated—even missed—how underlying exposures were changing, and not just in natural catastrophe insurance. For example, the market failed to recognize how litigation funding was transforming the public D&O landscape.

It is increasingly evident that both underwriters and reserving actuaries significantly underestimated the ultimate loss ratios of the business they were accepting, relying on historic loss picks that did not reflect the new reality.

Underwhelming Combined Ratios

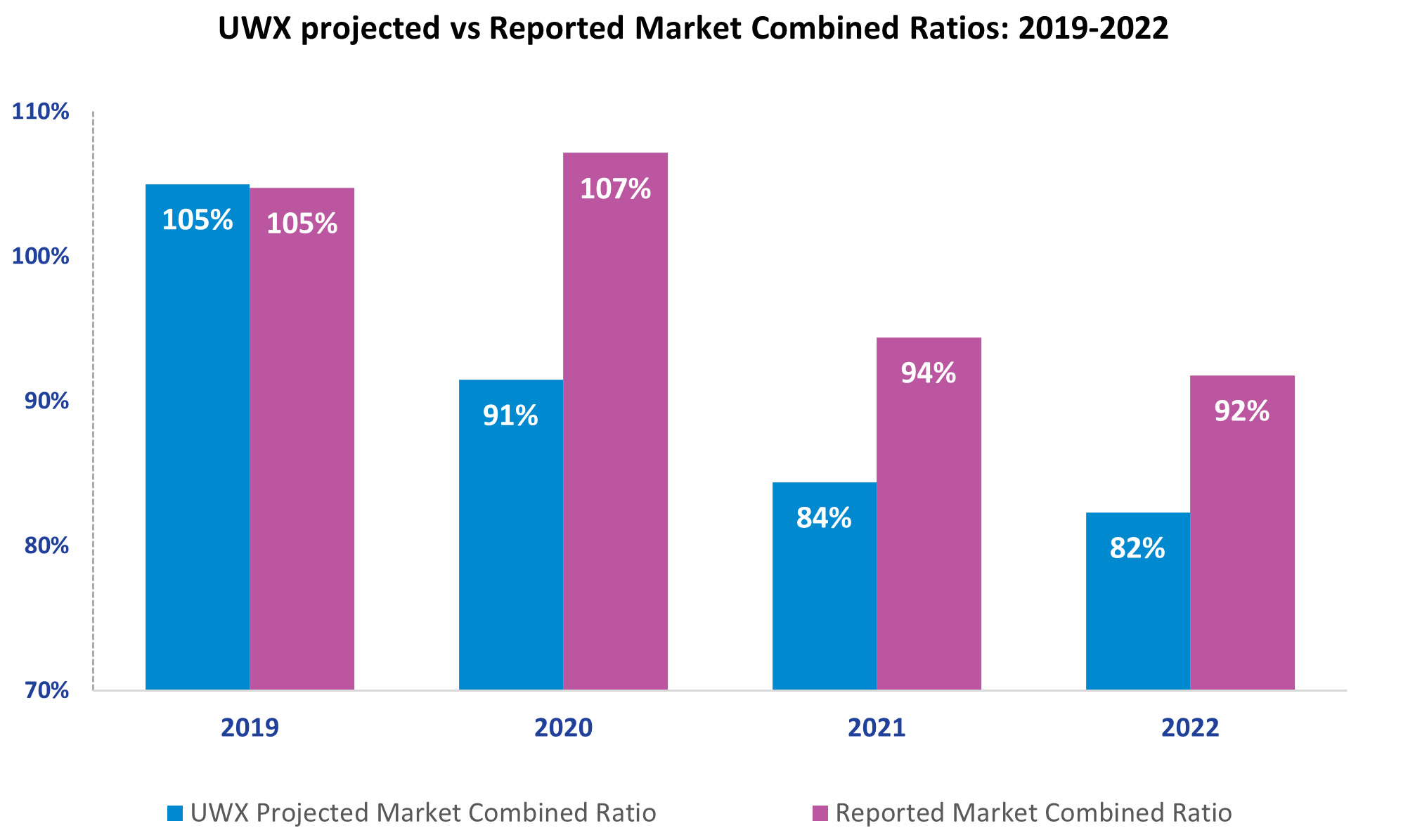

Reported combined ratios are underwhelming when one considers the significant changes to terms and conditions being negotiated. A good way of looking at it is to do this thought experiment: If we assume 2019 was a normal year in terms of loss burden and then factor in the price changes pushed through since then, CORs should be in the mid to low 80s, but they are coming in much higher. (See accompanying chart).

Why is there such a disparity?

Clearly COVID-19 plays a role, particularly in 2020, as does inflation (both social and consumer price), although inflation assumptions vary significantly across the market while the performance gap does not. Something else is going on here.

A fruitful place to look is how the changes being made by underwriters at the front end of the business are being translated into reserving loss picks at the back end of the business.

Underwriting vs. Reserving Actuaries

This is fundamentally about how different functions think. Underwriting breaks down into three core components: the evaluation of exposure, the definition of coverage and the negotiation of an appropriate price for risk transfer. They come in that order. You cannot, for example, define a coverage without first defining the exposure. So, when CUOs reunderwrite their portfolios, they think exposure, then coverage and then price.

Reserving actuaries, on the other hand, think evidence and explanation. Bruised perhaps by their experiences during the soft market and wary of overestimating the positive impact of front-end changes, reserving actuaries prioritize objectivity. Their natural bias is toward elements they can quantify. As a result, the changes the reserving team value most are not changes to exposure or terms and conditions but to pure price. These are objective. Changes elsewhere are subjective, with haircuts applied accordingly.

Both positions are thoroughly logical. But put them together and there’s a rub.

Reunderwriting Portfolios

How can this apparent conundrum be resolved?

While there is no magic wand, here are three points to consider when reunderwriting portfolios.

First, no amount of market hardening is going to make a poor exposure a good one. Risk selection remains paramount, and market hubris about there being “no such thing as a bad exposure, only inadequate price” should be consigned to history.

That said, underwriters still need to quantify exposure changes. This is easier when exposures are discrete and cohorts of claims (and associated premium) can be excluded. But typically, exposure reunderwriting is about refining the choice of exposures taken on in a population rather than ringfencing the population as a whole. So, the focus is on quantifying the differences between risks retained and risks discarded. Availing of multiple third-party sources of data for this exercise can be very useful. For example, in marine, fleet quality can be scored, and those scores can be back-tested against the insurer’s own experience. The seemingly subjective risk selection is converted into a quantified, objective portfolio change.

Second, the industry needs to rethink how it quantifies changes to wordings. This is the most difficult aspect of reunderwriting to quantify accurately, but it’s not impossible. It is important to be specific. Exclusions and writebacks are essentially changes to exposure, and therefore follow the logic outlined above, while changes to deductibles and sublimits are typically expressed numerically, and therefore can be modeled quantitatively. For example, emphasis changes between “all reasonable endeavors” and “best endeavors” used in construction contract language have been interpreted quite differently by the courts and imply different levels of volatility, so statistically they would mean different projected levels of loss. If insurers do not have in-house resources for such analysis, they should leverage their reinsurance relationships for their insights wherever possible.

Third, tread carefully around price. Prices are quantitative, so at first glance they appear objective. However, price is a derivative of exposure and coverage, not the other way around. If the underlying risk has been thoroughly reunderwritten and reframed, comparing year-on-year price is comparing “apples and oranges.” Furthermore, a prioritization of price change can inadvertently encourage suboptimal behavior. If metrics emphasize year-on-year rate improvement, in our experience, this can undermine good risk selection and the thorough reunderwriting of the portfolio. It is just too tempting to retain some risks where (KPI enhancing) headline rate improvements can be achieved, particularly if those readily quantifiable rate improvements are fully recognized in the ultimate loss pick.

Internal Agreement Needed

In all these dimensions, it is important to drive internal agreement. There must be a priori alignment between underwriting and actuarial as to how changes will be assessed and recognized in the loss pick. Good external data and insight can support this (and indeed, pay for itself in the process). Conversely, underwriters need to resist the temptation to force through changes unless they demonstrably impact the loss ratio. Such moves just add complexity and opaqueness, not what risk managers need when they themselves are having to justify premium increases to their stakeholders.

In conclusion, as firms seek to maximize the value from underwriting in today’s market, it is vital they have a clear and consistent view on the value of different components of remediation. Only then can the true impact of underwriting actions on performance be recognized. And accuracy here matters. Companies may be saved by strong coordination between underwriting and reserving in a soft market. But profitable growth depends on strong coordination when the market is hard.

Five AI Trends Reshaping Insurance in 2026

Five AI Trends Reshaping Insurance in 2026  AIG, Chubb Can’t Use ‘Bump-Up’ Provision in D&O Policy to Avoid Coverage

AIG, Chubb Can’t Use ‘Bump-Up’ Provision in D&O Policy to Avoid Coverage  What Analysts Are Saying About the 2026 P/C Insurance Market

What Analysts Are Saying About the 2026 P/C Insurance Market  Allianz Built an AI Agent to Train Claims Professionals in Virtual Reality

Allianz Built an AI Agent to Train Claims Professionals in Virtual Reality