Although the pandemic may appear more distant in the rearview mirror, its lasting impact on the personal auto insurance industry may be larger than initially expected.

Executive Summary

Given the persistence of high loss costs, a return to underwriting profitability for the auto segment in 2023 appears highly unlikely, writes AM Best Associate Director David Blades. In fact, for 2023, AM Best is currently forecasting a 106 combined ratio for the U.S. personal auto segment, he notes in the article that describes the headwinds carriers are facing. In spite of the challenges, inflationary trends eventually will plateau, and in the meantime, more sophisticated pricing algorithms, along with good risk selection and disciplined underwriting, should help carriers chip away at unfavorable results, he writes.Private passenger automobile insurance is the largest segment of the U.S. property/casualty insurance industry, accounting for almost 70 percent of the personal lines segment and a third of U.S. P/C net premium written. It is a critical line of business for many insurance companies.

Historically, the personal automobile line’s underwriting results have been stable, nearing breakeven in most years. However, personal auto insurers reported stronger-than-usual performance in 2018-2019, and results remained favorable in 2020 as the pandemic surged, unemployment spiked to the highest levels in years and miles driven plummeted. Because of the drastic drop in miles driven during the early months of the pandemic, personal auto insurers returned approximately $14 billion in premiums to policyholders.

Unfortunately, it has been an uphill road ever since.

Auto insurers recorded an underwriting loss of more than $4.1 billion in 2021, with a rapidly worsening loss ratio through the first six months of 2022. AM Best’s private passenger auto composite shows an additional $10 billion in underwriting losses through the first nine months of 2022. Although bottom-line results for 2022 have not yet been finalized, indications are that they won’t be pretty: AM Best has estimated a combined ratio of 110.1 for 2022—a two-year deterioration of nearly 18 percentage points.

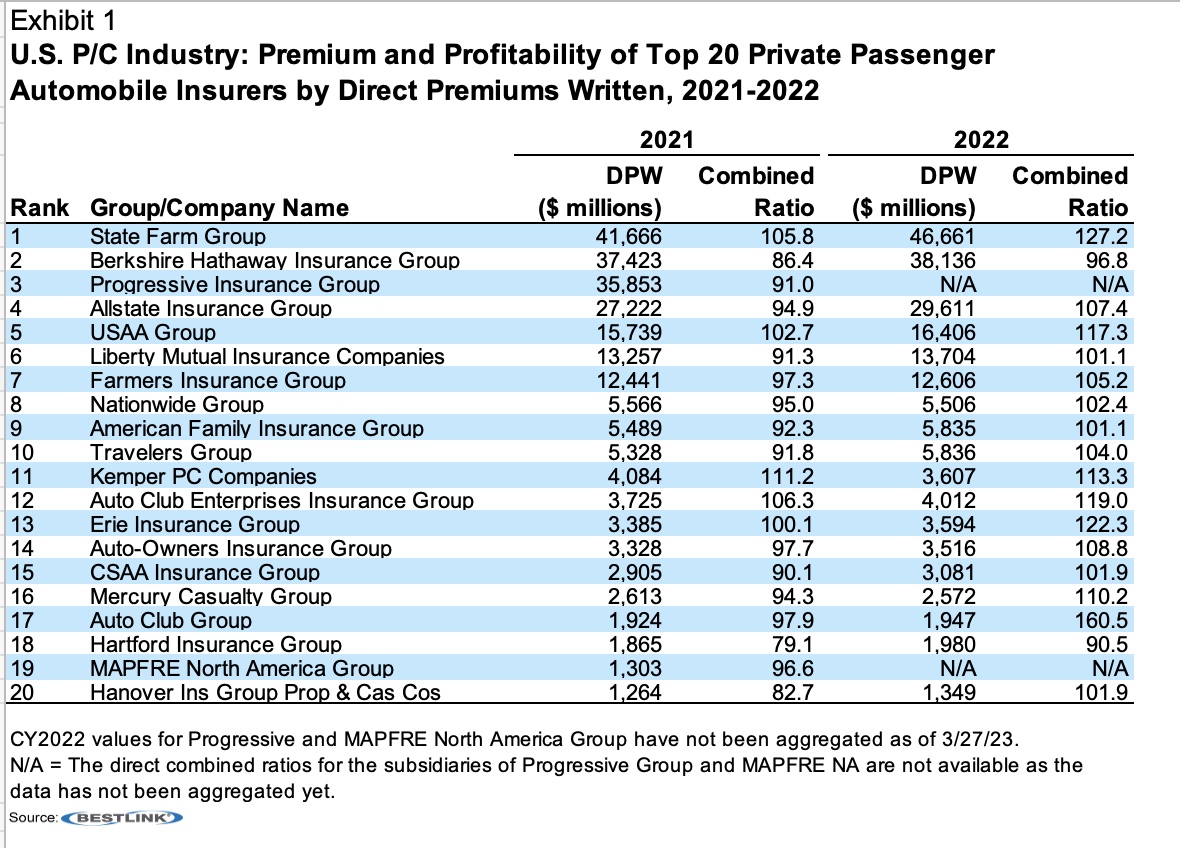

These results are dragging the entire P/C segment’s performance metrics down. Preliminary results for 2022 show a steep decline in underwriting results for the entire segment—a $26 billion loss, for which the personal auto lines of business are primarily responsible. Early results of the leading private passenger auto insurers also indicate a dramatic downturn in 2022 on a direct basis (prior to the effects of reinsurance ceding). AM Best has aggregated 2022 direct premiums written (DPW) for 18 of the top 20 insurers of 2021 (Exhibit 1). DPW for those companies increased modestly, by 5.6 percent, but that increase was outpaced by a greater increase in losses. In 2021, only five of the top 20 auto writers produced direct combined ratios above the breakeven measure of 100.0. In contrast, 16 of the 18 companies for which 2022 combined ratios have been calculated thus far have ratios above 100.0.

Deteriorating Loss Severity a Key Hurdle

One of the main factors accounting for the deterioration in the results of auto insurers is the rise in loss severity, attributable to a higher rate of fatalities. One reported trend during the pandemic was vehicles traveling at higher speeds on mostly empty roads in 2020. After vehicles started returning to U.S. roadways, accidents occurring at these elevated speeds have on average been more serious, causing greater damage and driving up claim values for third-party liability and auto physical damage. Recent National Highway Traffic Safety Administration (NHTSA) statistics show that 31,785 people died in traffic crashes in the first nine months of 2022, compared with 27,019 during the same period of 2018. In April last year, Cambridge Mobile Telematics reported that, although speeding levels are well below the highs of 2020, it is still elevated compared with pre-pandemic years.

In 2021, the number of fatalities jumped by 11 percent over the previous year. Additionally, the average cost per private passenger auto claim rose by 14 percent, reaching almost $10,000 per claim. (Related research: “Numerous Pressures Create Tough Terrain for Personal Auto Insurers,” AM Best, Nov. 11, 2022) Distracted driving and poorer driving habits post-pandemic have played meaningful roles in the deteriorating auto results. NHTSA statistics show that roughly 14 percent of injuries in traffic accident crashes are due to distracted driving. This issue is proving difficult to rectify despite measures taken by the NHTSA and others to reverse recent negative trends. Whether the distractions are from talking with passengers, talking or texting on cellphones, adjusting vehicle controls, eating, or other activities, they generally fall into one of three categories, as noted by the Insurance Information Institute:

- Visual—drivers taking their eyes off the road.

- Manual—drivers taking their hands off steering wheels.

- Cognitive—drivers taking their minds off driving when behind the wheel.

Rising medical costs are also an issue that insurers are grappling with. Third-party auto claim costs have been on the rise over the past few years due to many factors, including social inflation, nuclear settlements and rising medical costs. These costs, coupled with escalating prices of motor vehicle parts and equipment—up by 15 percent year over year in the first half of 2022, according to the U.S. Bureau of Labor Statistics—have also contributed to the poor personal auto results.

Many insurers continue to raise rates in pursuit of improved premium adequacy to offset rising loss cost severity, but their efforts have not yet succeeded, especially as the rate approval process in many states for this highly regulated line is very restrictive. Most approved rate changes have been for less than companies’ actuarial indications, resulting in the need for additional rate filings. Furthermore, the backlog in rate approvals in 2022, particularly in California, didn’t start to clear up until later in the year.

With auto results declining in 2022, returning to a favorable—or even a breakeven—combined ratio will take time given the need for improvement in several areas, such as adverse loss severity and rate adequacy. AM Best is forecasting a combined ratio of 106 for 2023. If current inflationary pressures persist through the year, higher vehicle repair costs are unlikely to improve materially. Ongoing supply chain challenges and recessionary fears will also remain headwinds for auto insurers if they are to realize an improvement in performance.

The U.S. nonstandard auto insurance industry, a subsector of personal auto, has also been beset by losses, based on AM Best’s aggregation of results for the predominant nonstandard auto-focused insurers. Through the first three quarters of 2022, the segment incurred an underwriting loss of almost $1.2 billion due to many of the same market issues the standard personal auto writers are contending with. This substantial underwriting loss follows $1.3 billion in underwriting losses in 2021.

Premium Isn’t Profit

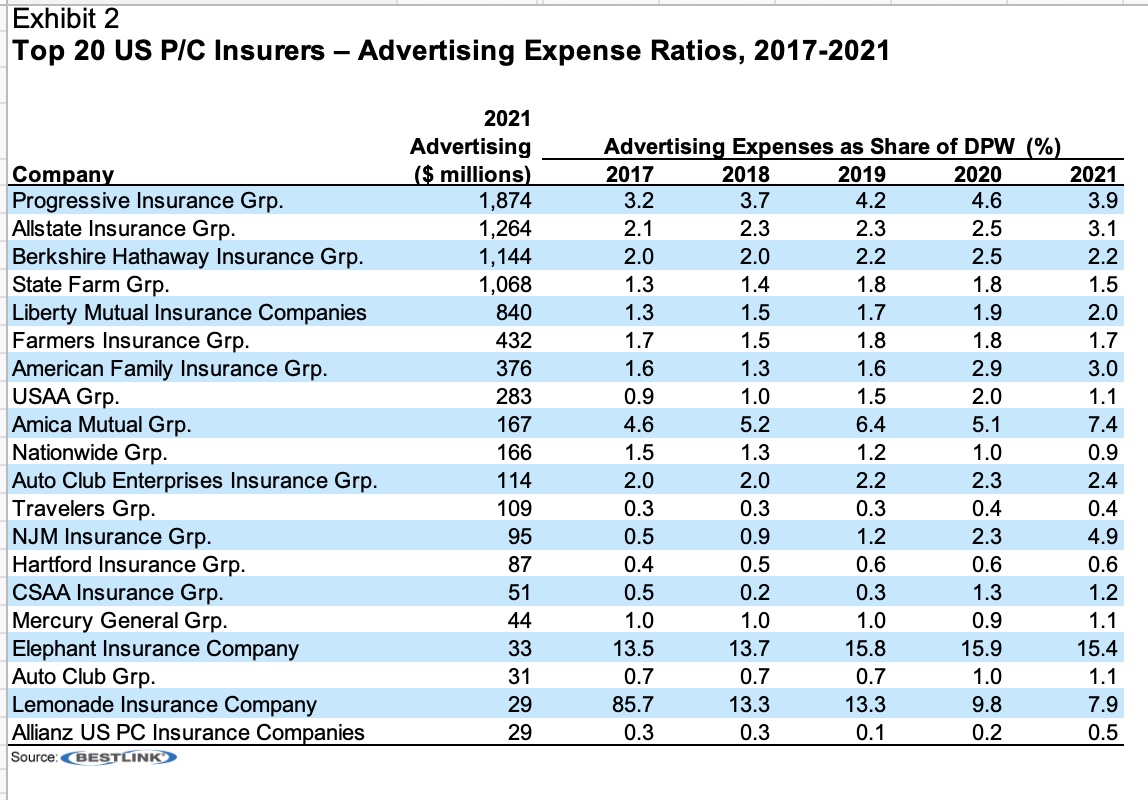

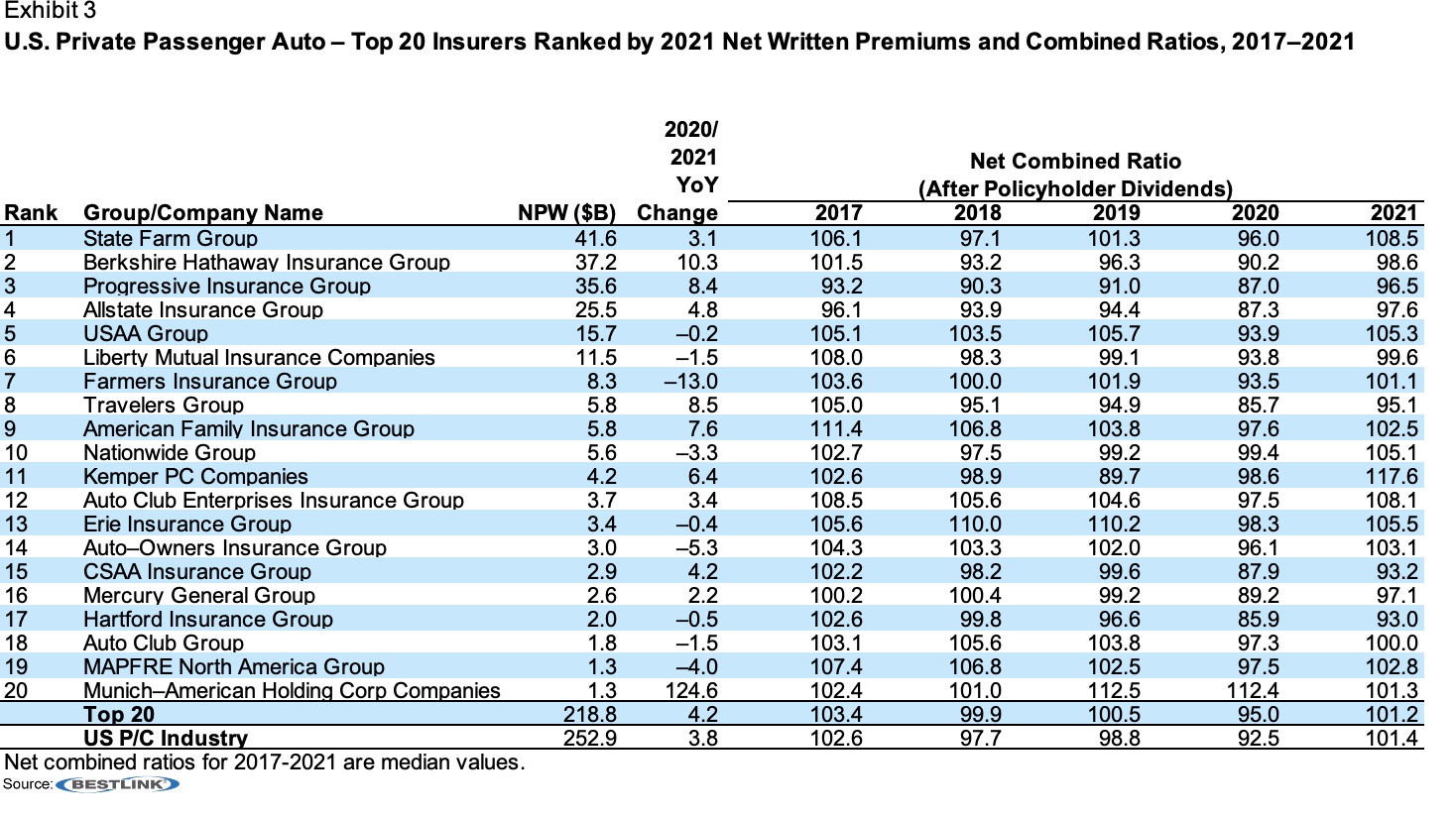

The personal auto segment is well known for its advertising, especially by the top writers (Exhibit 2). The importance of branding in gaining and preserving market share is highlighted by nine of the top 10 insurers also ranking among the top 10 in annual advertising expenses. However, premium volume does not guarantee profitable results, as 12 of the top 20 companies ranked by 2021 private passenger auto net premiums written posted combined ratios of over 100 in 2022 (Exhibit 3). The considerably negative impact of inflationary pressures on personal lines loss trends led to insurers cutting the financial resources allocated to advertising in 2022 to help their underwriting expense load. Again, the regulatory environment, particularly in key states such as California and New York, makes raising rate increases to address price adequacy and lessen the pressure on profitability more difficult.

Reasons for Optimism

At the same time, personal auto carriers remain ahead of the curve in terms of pricing sophistication and have likely built on their competitive advantages. The personal auto line has led the charge in the insurance industry in digitization. For many years, the industry has made a push to leverage technology, including claims, underwriting and distribution. Most companies also have updated their legacy systems. These innovative efforts have led to greater efficiencies and enhanced customer experience.

The growing use of telematics and usage-based insurance may help address loss frequency, as insurers can measure driving behavior or implement additional product innovations such as per-mile insurance. However, this is unlikely to have a meaningful impact over the near term.

Newer vehicles with enhanced safety features account for a growing percentage of vehicles on the road, which may also impact frequency favorably, although their repair costs are higher. With access to needed parts and—just as important—qualified labor limited, the cycle time for repairs has lengthened considerably, resulting in additional loss cost pressures.

Given the persistence of high loss costs, a return to underwriting profitability for the auto segment in 2023 appears highly unlikely. Inflationary trends eventually will plateau, but how long this environment will continue remains highly uncertain. More sophisticated pricing algorithms, along with good risk selection and disciplined underwriting, should help carriers chip away at some of the unfavorable results. Some companies may need to reconsider their risk appetites.

Overall, personal auto insurers remain well capitalized and vigilant in their pursuit of rate adequacy and have benefited from the implementation of advanced technology, which has resulted in greater efficiency.

As the use of technology increases across the broader financial services industry, companies will continue to look for ways to meet higher customer expectations. Those companies that can’t meet rising customer expectations will be at a competitive disadvantage. Fostering innovation in all operational phases will continue to benefit personal auto writers as they focus on achieving adequate rate levels.

Preparing for an AI Native Future

Preparing for an AI Native Future  How Americans Are Using AI at Work: Gallup Poll

How Americans Are Using AI at Work: Gallup Poll  Winter Storm Fern to Cost $4B to $6.7B in Insured Losses: KCC, Verisk

Winter Storm Fern to Cost $4B to $6.7B in Insured Losses: KCC, Verisk  RLI Inks 30th Straight Full-Year Underwriting Profit

RLI Inks 30th Straight Full-Year Underwriting Profit