The onset and continuation of the COVID-19 pandemic made everyone—property/casualty insurers included—respond quickly and reevaluate their priorities. Now, as global premiums rebound, insurers are taking a fresh look at their technology goals and how to achieve them.

Disruptions Driving Resilience

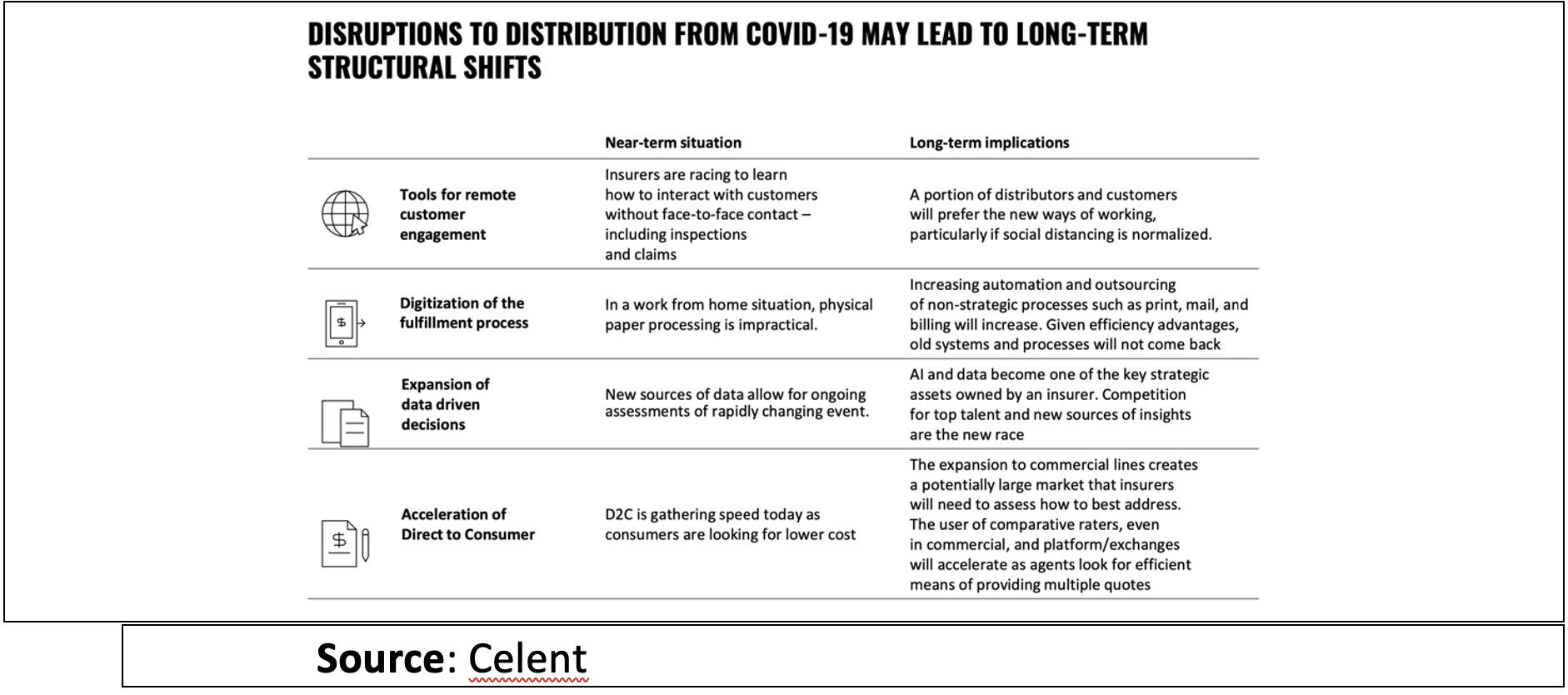

Near- and long-term shifts that the pandemic accelerated and which may become permanent include the shift to remote work, on-demand everything, artificial intelligence and the growth of customization. Celent’s “Top Technology Priorities for P&C Insurers in 2021“report took a detailed look at how these drivers are influencing technology priorities within the field.

The pandemic’s initial impact delayed major initiatives for insurers, such as transformation programs and legacy system replacements. These activities rebounded as 2020 progressed and will likely help drive resilience in 2021. Spending on technologies related to customer experience, data/analytics/AI, digitization and ecosystem transformation also slowed in response to the pandemic, but P/C insurers are now set to increase investments in these areas.

P/C insurers are emphasizing technologies that help innovate along their traditional value chain and that respond to needs highlighted through the pandemic. Priority goes to technologies that: offer protection from cyber threats; focus on efficiency in software delivery (driving cloud adoption, use of open source software and deployments of agile technologies); and digitize channels (to grow sales, engage customers, advance productivity and deploy data/AI techniques that enhance underwriting).

Strategic Investments

Growth and process optimization are the most influential business goals when it comes to driving technology investment plans. COVID-19 likely accounts for this, as insurers look to grow some of the reduced exposure units (e.g., workers employed, miles driven), while emphasizing digital technologies that will continue to optimize additional processes. These were among the findings of Celent’s “North American Property/Casualty Priorities and Pressures: 2021 Annual CIO Survey Results“ report, based on a December 2020 survey of P/C insurance company CIOs and other technology executives.

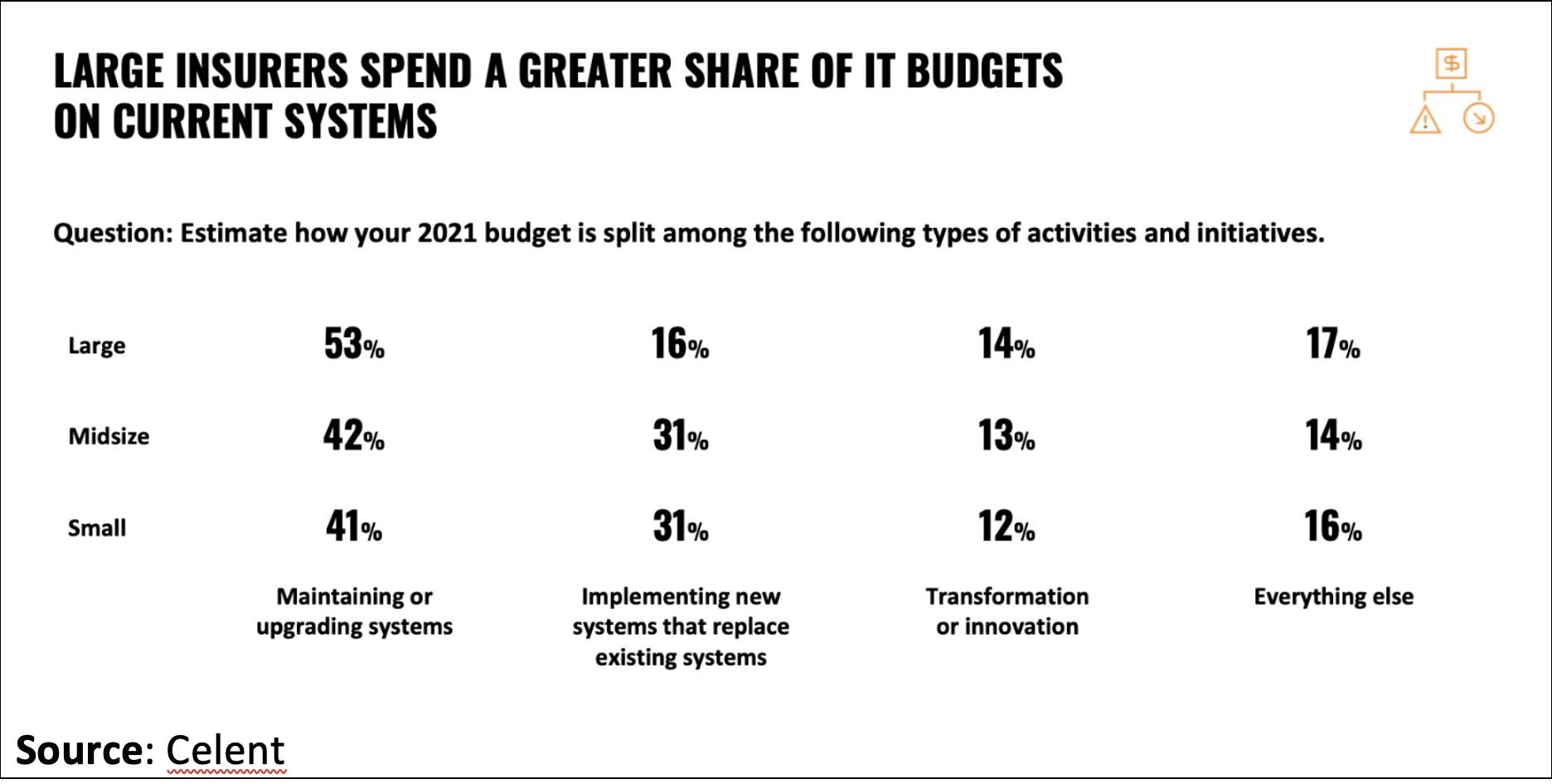

As CIOs recalibrate their budgets, they’re funding a wide array of new and existing technologies. To achieve top business priorities, they’re investing in core systems. About half of CIOs surveyed have plans to replace Big 3 core systems (policy admin, core claims, rating systems) in 2021. Many are budgeting to enhance customer experience, all while data and analytics initiatives continue to mature.

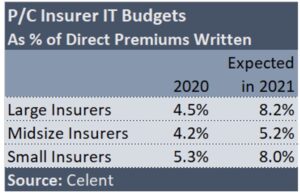

IT budgets in 2020, measured as a percentage of direct premium written, were broadly consistent with prior years, averaging 4.5 percent for large insurers, 4.2 percent for midsize insurers and 5.3 percent for small insurers. A large year-over-year increase in IT budgets is expected in 2021, with averages growing to 8.2 percent, 5.2 percent and 8.0 percent, respectively. These increases may be attributed to the core systems replacement plans or to the impact of COVID-19: playing catch-up with cancelled or delayed projects from 2020 or the need to enhance digital functionality and automation as part of the “new normal.”

IT budgets in 2020, measured as a percentage of direct premium written, were broadly consistent with prior years, averaging 4.5 percent for large insurers, 4.2 percent for midsize insurers and 5.3 percent for small insurers. A large year-over-year increase in IT budgets is expected in 2021, with averages growing to 8.2 percent, 5.2 percent and 8.0 percent, respectively. These increases may be attributed to the core systems replacement plans or to the impact of COVID-19: playing catch-up with cancelled or delayed projects from 2020 or the need to enhance digital functionality and automation as part of the “new normal.”

For the back office, cyber defenses remain the top priority for 2021. Cybersecurity budgets in 2020, as a percentage of total 2020 IT budgets, averaged 4.9 percent for large insurers, 7.3 percent for midsize insurers and 3.6 percent for small insurers.

Imperative Technologies for 2021

What shape will these investments and priorities take in 2021?

P/C insurers will be focusing on five main themes, each with particular technology imperatives.

- Customer experience transformation

Sustainable growth through differentiated offerings depends on transforming the customer experience—whether the customers are policyholders or agents. Essential to this approach: a new, customer-centric framework that’s cross-functional and anchored in both the process and the emotional journey. A customer-first mentality requires removing the obstacles that customers face while delivering convenience, speed and personalization.

P/C insurers will:

- Expand digital services and building out ecosystem platforms, drawing on offerings from more than 1,550 InsurTech and more than 2,700 fintech companies. Insurers are moving beyond pure indemnification models to providing customers with a broad set of digital services and relying on new emerging technologies to enable the delivery of these services at scale.

- Embrace collaboration tools (for use with policyholders, staff and agency partners). Accelerated usage, which supported work from home, is set to continue. Tools include video communications, consumer messaging applications, chatbots and virtual assistants, as well as social and collaboration management tools.

- Update UX design in portals, mobile apps and websites to match closely the mental models of users.

- Improve customer identity management. In a recent Celent poll, 55 percent of insurers stated that they use a customer identity and access management (CIAM) solution—one of multiple methods of authenticating customers. Insurers can use a CIAM to manage customer user identities, offering those customers a secure and seamless login experience for the company’s websites, applications and other online services.

- Data-driven everything

Identifying profitable niches, managing risk and improving service are all ways of gaining a competitive advantage through data. P/C carriers must evaluate data sources and methods of analyzing and automating that data in order to push competitive boundaries.

Predictive analytics, incorporating artificial intelligence (AI) and machine learning (ML), provides the robust data capture that’s required for functions such as underwriting and claims, fraud monitoring, customer strategies, and customer service. With permanent statements on record existing for each link in the claims data supply chain, touchless claims may be processed in as little as 5-10 minutes.

Integrated fraud and risk management platforms orchestrate variables—including image data monitoring, biometrics, predictive analytics, a rules engine, AI/ML and robotic process automation (RPA)—to improve and secure customer experiences across transactions. At this time of heightened awareness of cyber risk, when more than a third (38 percent) of P/C CIOs have experienced a cyber attack within the past three years, P/C insurers will also be prioritizing cyber risk management capabilities.

- Digital and emerging technologies

Digitalization automates complex tasks, which can then be mastered, reproduced and distributed at no cost. Insurers can get there by embracing emerging technologies that shift the focus from “event driven” to “active” digital propositions. This may be reflected by shifting the focus of customer experiences from periodic to continuous or shifting pricing from tiered to utility/behavior-based.

To make these shifts possible, insurers will reuse existing technology for a heavier middle tier that incorporates APIs, orchestration, rules and monitoring. Underwriting platforms and desktops will leverage data and digital to underwrite more effectively. As distribution channels expand, direct-to-consumer offerings are likely to increase (including for commercial lines) and insurers will offer new digital advice models and self-service technologies to meet customers’ needs. The back-end needs (including broker and social media support) will also be prioritized to make customer interactions more effective and less costly. Finally, digital enablement will see growing services for connected cars and homes, creating data-driven value for insurers.

- Innovation and execution

Insurers looking for innovation must embrace fundamental changes (to business models, products and services) in order to provide value to customers. Digital transformation agendas are evolving to focus on how to use data and AI to become smarter organizations. APIs, cloud and microservices are at the forefront of how insurers can sustainably scale their digital ecosystem.

Innovation in the insurance industry is both disruptive (by digital native players) and incremental (by traditional insurers). Much of the push for innovation is coming from internal cultures of innovation. This is also the era of acceleration in insurer-InsurTech startup partnerships. In North America, areas of interest for partnerships are claims, risk transfer/reinsurance, sales and marketing, and servicing/operations.

- Legacy and ecosystem transformation

Now is the time for insurers to move beyond modernization. Wide-ranging transformation is necessary, including interactions with customers, counterparties and regulators.

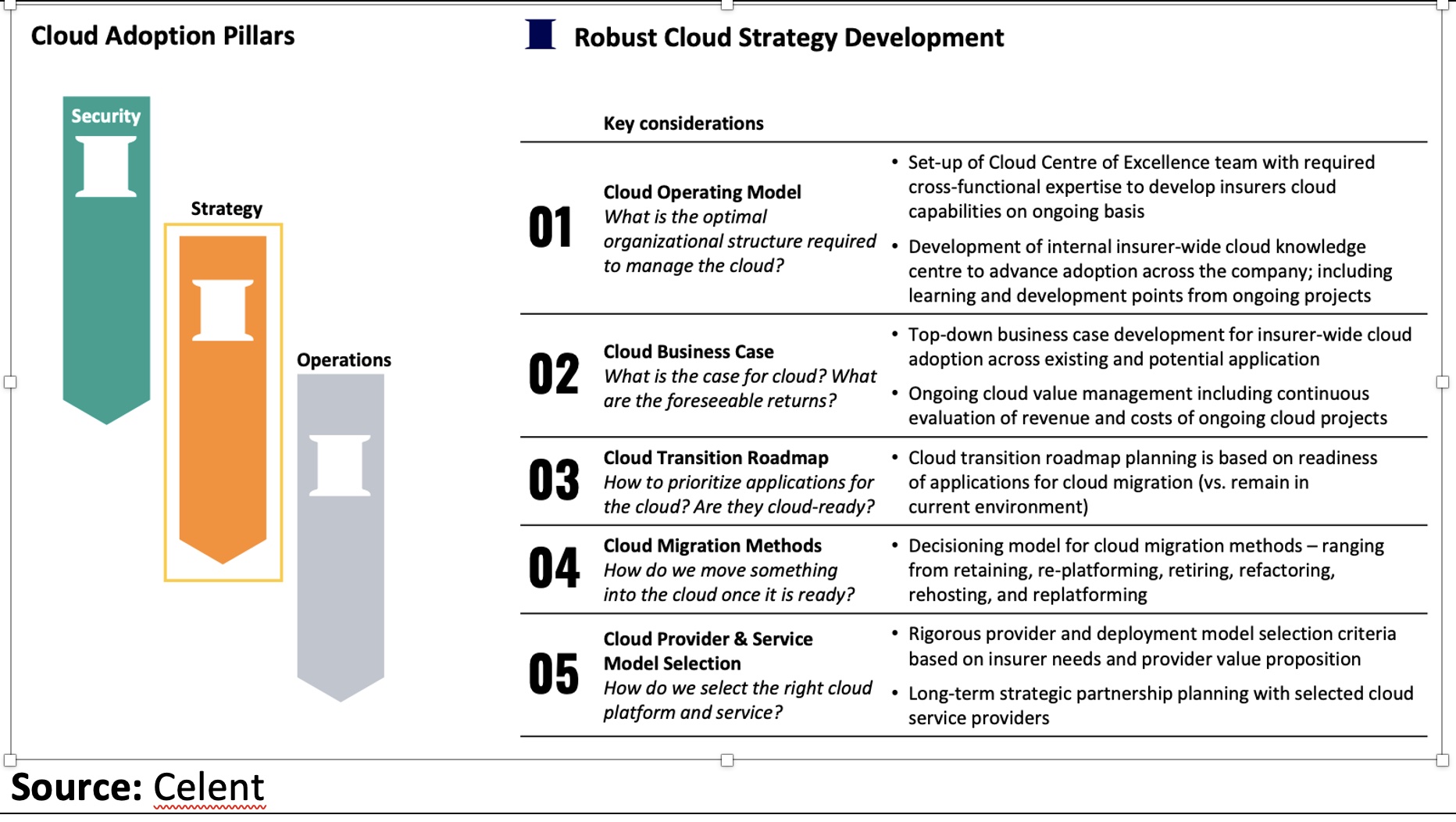

A new architecture is essential. The componentized system common in core insurance systems is giving way to microservices, API and cloud-oriented architecture. As cloud gains momentum, most insurers are moving toward a mix of on-premise, public and private cloud deployments. While scalability/elasticity ranks highly as a perceived driver, for example, many insurers perceive compliance as a strong inhibitor toward cloud migrations.

Varied cloud deployment approaches are available to financial institutions; each model requires careful consideration of the risks and benefits as part of a robust cloud strategy. DevOps is a strong focus for all insurers in 2021, with large and midsize insurers also turning to the cloud extensively for data and analytics. All insurer segments broadly favor cloud-ready or cloud-native packages.

P/C insurers have certainly been resilient in the wake of a tumultuous year. CIOs are investing in a wide array of existing and innovative systems, affirming the central role that technology plays in achieving corporate goals. Insurers that want to meet new advocates, customers, market challenges and risks will be well served by keeping technology enablers at the center of their plans.

AXA XL to Acquire S-RM

AXA XL to Acquire S-RM  The Impact of Subsidization on Commercial Auto Telematics Programs

The Impact of Subsidization on Commercial Auto Telematics Programs  As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act

As Wildfires Destroy and Displace, APCIA Says Congress Must Pass Fix Our Forests Act