Today’s insurers want to be there for their customers—literally.

With sensors of various kinds in policyholders’ cars, homes and personal devices, “exposure data tracking” is rapidly becoming a competitive imperative in personal lines underwriting and rating.

Executive Summary

“Exposure data tracking” is rapidly becoming a competitive imperative in personal lines underwriting and rating as sensors are embedded in policyholders’ cars, homes and personal devices. Experts speaking at the 2017 Ratemaking and Product Management Workshop of the Casualty Actuarial Society explained the ramifications of the risk shifts.That was the message from two speakers on technological changes at the 2017 Ratemaking and Product Management Workshop of the Casualty Actuarial Society (CAS), March 28 in San Diego.

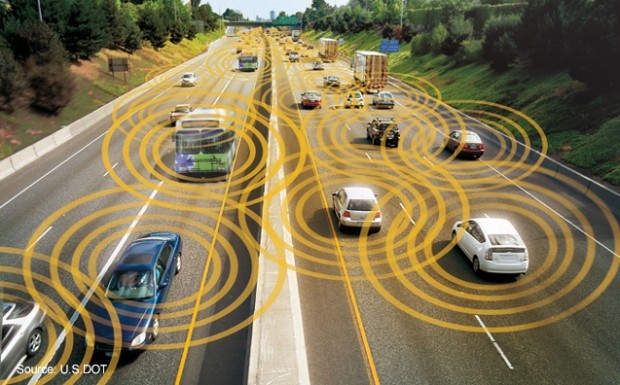

Vehicle sensors that plug into car portals don’t just track speed, braking and turning, said Sheri Scott, a principal and consulting actuary with Milliman. “They can even determine what kind of traffic and weather you’re driving in,” she said.

With access to such extensive data in real time, auto insurers can now monitor the risk posed by a vehicle without relying on information provided by applicants and insureds about their driving habits, territory and garaging.

Exposure data tracking is the latest evolution of a change in personal auto insurance underwriting and marketing from direct call and Internet marketing to the development of advanced rating variables. And it’s all a prelude to the introduction of automated vehicles that will drive themselves largely—or entirely—on their own.

Scott said that major U.S. automakers will be marketing fully autonomous vehicles by 2020, and the early indications are that autonomous vehicles will have fewer accidents than cars driven by humans. She told attendees that an autonomous auto tested by Google accounted for 0.7 accidents per million miles driven compared to a typical average of 2.0 accidents per million miles involving drivers in the U.S.

Exposure tracking and the advent of autonomous vehicles are shifting personal auto insurance risk exposure from dependence on driver skills, estimated distances driven and garage location to the precise determination of vehicle locations, driving habits, driving distances and traffic conditions, all determined through the collection of trip data gathered in real time.

Yet even these underwriting considerations will soon be supplemented, if not supplanted, by the loss experience of automated vehicles and their manufacturers.

This transformation will not be without risks of its own, Scott said. In particular, she cited disruption of networked communications as a hazard, especially as vehicle occupants become dependent on automated control and less practiced at taking control of a vehicle.

“If some kind of communication goes down, there could be a very serious occurrence,” she said.

Connected Homes

As individuals become accustomed to having their driving habits monitored electronically, they also find themselves returning home to dwellings with sensors to detect what’s happening within and outside the house.

Thomas Smith, founder and president of Senteri, a firm focused on smart-home solutions for P/C carriers, told attendees that the Internet of Things now amounts to more “everyday objects” than cellphones connected to the Internet and collecting data.

Even with that, the IoT is still in its infancy, with a little more than 10 percent of homes in the U.S. equipped with “smart” thermostats, lighting, door locks, and smoke and CO2 detectors, plus monitors for security, heat and water use. However, such devices have become standard features of newly constructed homes.

Major carriers, including American Family, Liberty Mutual and State Farm have developed service packages for automated home monitoring with an eye toward attracting new business, improving retention, reducing losses and accumulating data as an asset for underwriting and ratemaking.

“The early movers are those carriers with the most resources,” Smith said. “This indicates to the rest of the industry what’s possible.

“You can almost have any sensor to detect any peril. It’s coming to be within the grasp of ordinary people.”

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz  The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age

The $400,000 Chief of Staff Is the CEO’s Secret Weapon in the AI Age