Explosive growth in InsurTech, efforts to engage a more demanding, younger consumer base, and ongoing regulatory concerns have combined to create significant hurdles across insurance. When these challenges are coupled with a looming industrywide talent gap, it becomes clear that insurers must adapt their practices in order to survive.

At the recent Valen Summit, nearly 100 insurance leaders from large and small companies gathered to acknowledge these growing pains and discuss how best to get past the turbulence and usher in a new chapter for the industry. While more than a dozen issues were discussed, a few of the most prominent recurring topics stood far above the rest as industry pain points.

- Insurers must be more effective at identifying their customers.

When discussing a centuries-old industry, it’s odd to consider that there is no consensus when it comes to insurers identifying their customers. An informal poll found that half of insurers identified “agents” as their primary customers, while the other half thinks about the consumer who is paying a bill as their prime target. The inability as an industry to define our customers helps to inform the challenges in insurance.

Today’s consumers have expectations that insurers never had to face. Companies like Google and Amazon have made leaps and bounds to remove friction from the customer experience, from minimalist design to one-click purchasing. Initiatives like Google Home and Alexa are just the beginning.

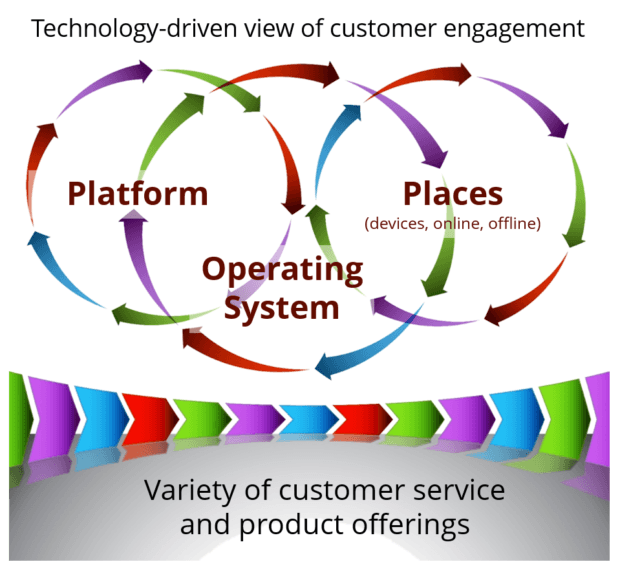

To create a customer experience that competes with a market leader like Amazon, insurers must reconsider their entire approach. Tech companies have created incredible customer experiences through an entirely different way of thinking. They see the world in terms of platforms and operating systems, bringing engaging and interactive experiences for the end user. Then they move into new vertical markets to further serve an existing consumer base. Everything is built with customers’ ease of use in mind.

- While looking forward, don’t forget the regulators.

InsurTech may have the industry rushing forward, but it’s the regulators who ultimately determine which products and services see the light of day. When participants were asked who is proactively taking steps to educate these gatekeepers, the room fell deathly quiet for a moment, before a general sense of doom took over. This was both telling and new.

One of the approaches that resonated the most was designating insurer personnel to build relationships with regulators, creating an ongoing resource for gatekeepers who don’t necessarily see how analytics and big data are applied to insurance products. Another popular approach was to bring product concepts to regulators far in advance of submitting them for approval, attempting to gain buy-in very early in the process and tweaking based on feedback. A final suggestion was to bring the vendors and data scientists offering data insights into the discussion. This drastically mitigates the possibility of confusion or misinterpretation of the information.

- Looking beyond loss ratios.

The final theme that emerged at the Summit was how many insurers had been subject to adverse selection by early adopters of data analytics. It used to be that analytics were a tool for early adopters; today, they are paramount to survival.

Many insurers that participated in our event acknowledged that competitors had aggressively gone after—and won—particularly low-risk portions of their book of business. This left the other insurers exposed to higher-than-anticipated claims, naturally, but also an unsteady feeling of “we need to catch up.”

Most insurers present for the discussion were moving beyond simple loss ratios when measuring their data analytics programs, and instead focused on the entire value they could derive from such solutions. This means creating adverse selection for other companies, staying ahead of market trends and protecting against volatile pricing swings.

Insurers today find themselves under pressure from shareholders, market forces, technology and regulators alike. When leaders from around the industry gathered for a frank discussion, concepts gravitated toward fixing the customer experience, improving relationship longevity, educating regulators to more rapidly develop and deploy products, and incorporating big data across their decision-making processes. Each concern carries its issues, but none is insurmountable. The insurance industry is entering a new era that requires new ways of thinking and modern approaches to maintain a competitive edge.

Retired NASCAR Driver Greg Biffle Wasn’t Piloting Plane Before Deadly Crash

Retired NASCAR Driver Greg Biffle Wasn’t Piloting Plane Before Deadly Crash  Experts Say It’s Difficult to Tie AI to Layoffs

Experts Say It’s Difficult to Tie AI to Layoffs  Flood Risk Misconceptions Drive Underinsurance: Chubb

Flood Risk Misconceptions Drive Underinsurance: Chubb  Lessons From 25 Years Leading Accident & Health at Crum & Forster

Lessons From 25 Years Leading Accident & Health at Crum & Forster