Negative ratings actions and financial challenges are forcing carriers to explore reinsurance options offering needed capital, according to a report released last month by Gallagher Re’s Strategic and Financial Analytics team.

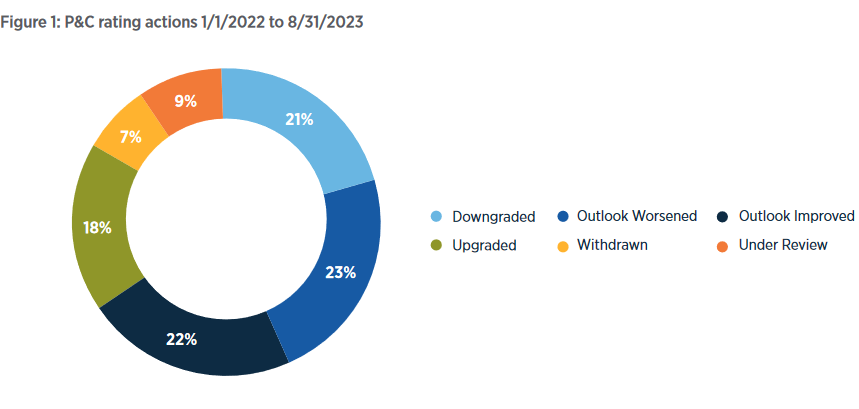

Downgrades of U.S. property/casualty (re)insurers jumped significantly in the first eight months of 2023, compared to the calendar year 2022, continuing an upward trend from 2021, according to Gallagher Re’s analysis of ratings actions by AM Best.

Negative rating actions (including outlook changes) outnumbered positive actions, “as AM Best placed more scrutiny on performance metrics, due to a number of factors, including an increase in costly secondary perils; inflation; and volatility in investment market,” the report noted.

Between January 2022 and the end of August 2023, there were 282 rating actions, with 109 carriers experiencing 60 rating downgrades and 64 negative outlook changes (15 experienced both), Gallagher Re’s analysis found. There were 77 carriers with a focus on personal lines, and 32 with a focus on commercial lines.

A number of factors have contributed to the uptick in carrier rating downgrades. An increase in the frequency of secondary perils leading to costs outpacing the rate of inflation, as well as social and economic inflationary pressures leading to higher claims costs and reserve increased.

“Net losses were exacerbated by changes in reinsurance availability, while volatility in investment markets further contributed to the pressure on insurers’ balance sheets,” the report added.

Common themes among the companies with negative ratings included a drop in surplus of over 20 percent, worsening underwriting performance and combined ratios on average rising to over 117 percent (deteriorating further to 120 percent in 2023).

The P&C sector experienced heightened weather-loss volatility and the effects of inflation, exacerbating loss costs. “This was especially true within personal lines, where there were higher attritional losses due to the costs of parts, materials, and labor remaining high,” the report noted.

Analysis of the 60 companies that experienced a ratings downgrade during the 20-month period, Gallagher Re found that 16 (27 percent) experienced a drop in surplus of over 40 percent, and 36 (60 percent) experienced a drop in surplus of over 20 percent percent as of Q2 2023.

Data revealed that of the 38 companies with a personal lines focus, 11 (29 percent) experienced a drop in surplus of over 40 percent, and 26 (68 percent) a drop over 20 percent as of Q2 2023.

Of the 15 companies with a commercial lines focus, 4 (27 percent) experienced a drop in surplus over 40 percent as of Q2 2023, the analysis showed.

Most carriers reported an operating ratio greater than 100 percent, because investment income was not sufficient to offset underwriting losses, the report found.

Between January 2022 and August 2023 Gallagher Re found that operating performance results as of Q2 2023 were challenged by “the confluence of increased underwriting losses and volatility in investment results, increasing the probability of negative rating actions.”

Of the carriers that experienced a negative downgrade, 45 percent also reported adverse claims development greater than 10 percent, a common contributor to negative ratings actions.

Adverse development was found to be more severe in commercial lines, likely due to rising loss cost severity as a result of litigation and economic inflation and the uncertainty over loss reserve adequacy, especially long tail casualty lines, the report stated.

Gallagher Re also analyzed ratings actions undertaken in the last four months of 2023.

An additional 13 companies were downgraded in this period, while 26 companies had their outlook worsened, the data showed.

On a positive noted, 39 companies experienced improvements in their outlook.

The favorable outlook changes are the result of positive actions taken by company management, rather than an improvement in market conditions, the analysis found.

AM Best plans to maintain a “negative” outlook for personal lines going into 2024 due to a deterioration in personal auto, impacting both underwriting results and surplus, ongoing rate adequacy challenges, elevated reinsurance costs and potential reinsurance capacity constraints, and increased claim severity and property claim settlement times.

Commercial lines have been given a stable outlook by A.M. Best, despite negative outlooks on commercial auto, general liability, professional liability and title markets.

Commercial property, private mortgage insurers, surety, medical professional liability, and workers’ comp have stable outlooks, while only the excess and surplus lines market has a positive outlook.

To avoid negative rating actions, carriers need to ensure “pricing adequately covers loss-cost trends and underwriting is not sacrificed for opportunistic premium growth,” the report stated.

A strong enterprise risk management process and modeling can assist carriers, as well.

Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses

Beyond the Weather News Bulletins: How Insurers Can Improve NatCat Responses  AI Pushes Underwriting Beyond Risk Selection to Prevention

AI Pushes Underwriting Beyond Risk Selection to Prevention  Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak

Wendy’s, Chipotle Not Affected by Cyclosporiasis Outbreak  Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent

Insurer Interest in AI Exclusions Growing as Risk Becomes Omnipresent