Despite the reversal seen in the U.S. equity market and rising inflation and interest rates, P/C insurers performed well in 2022, according to the latest report on the long-term impairment rates of AM Best-rated, U.S.-domiciled insurance companies states.

The Best’s Special Report, titled, “Best’s Impairment Rate and Rating Transition Study — 1977 to 2022” added just two property/casualty insurance companies to the list of impaired insurers in 2022, FedNat Insurance Company and Americas Insurance Company. In the previous year, 10 carriers were identified as impaired by AM Best.

Rising loss costs, catastrophe frequency and social inflation were the main concerns for P/C insurers, even as pricing momentum and investment income remained favorable.

“Despite a moderate decline in surplus driven by significant unrealized losses in asset holdings, the majority of P/C companies maintain strong risk-adjusted capitalization,” the report stated.

The study, aimed at estimating the risk of impairment of U.S. insurers, covers 45 one-year periods from Dec. 31, 1977, to Dec. 31, 2022, and includes U.S. insurers that had at least one Financial Strength Rating (FSR) or one corresponding Long-Term Issuer Credit Rating (ICR) during the study period.

Two categories of impairment were noted:

Gross impairments encompass the broadest definition of impairment and include companies that AM Best has ceased rating by the time of impairment. According to the credit rating company, “Gross impairments reduce cohorts of insurance carriers by withdrawn ratings, thus further boosting impairment rates.”

Net impairments represent gross impairments, but insurers that became impaired after rating withdrawal were not counted, and cohorts of insurers are not reduced for withdrawn ratings.

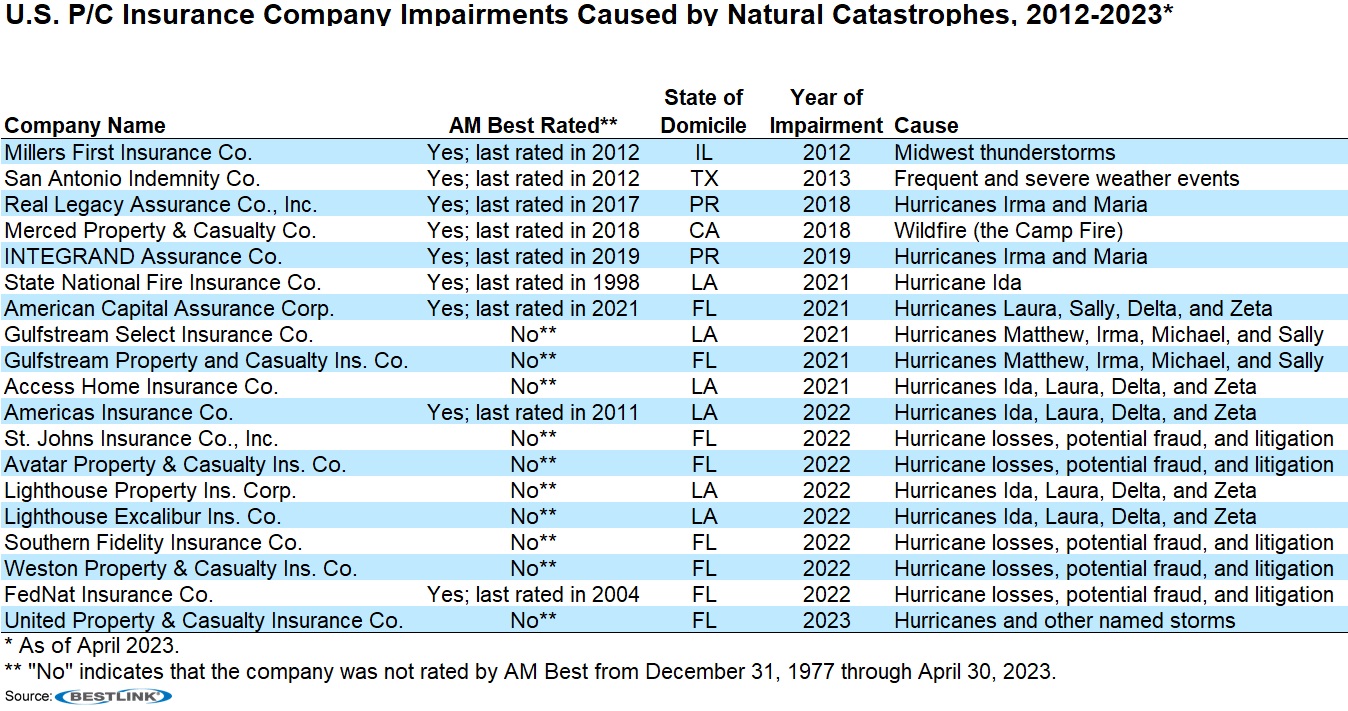

Hurricane losses, a high number of litigated claims, and suspected roof replacement fraud caused one insurer, domiciled in Florida, to become impaired. A Louisiana-domiciled company became impaired following multiple hurricane-related losses (from Ida, Laura, Delta and Zeta).

Fourteen companies, either domiciled in Florida or Louisiana, including AM Best-rated and non-AM Best-rated companies, have become impaired due to natural catastrophes since the start of 2021. The increase in frequency and severity of catastrophe events, especially secondary perils, according to the report, has placed a significant amount of pressure on insurers in recent years.

AM Best points out that some findings in the study tend to be intuitive. For example, a given rating in one year, such as “a-,” tends to be a good predictor of a similar rating in the following year. In addition, a financially weak company is more likely than a financially strong company to become impaired. And for companies with higher initial ratings, the time to impairment tends to be longer.

“It took an average of 17.0 years for FICs [financially impaired companies] that were initially rated “A++/A+” to become financially impaired, but only an average of 11.4 years for FICs rated “B/B-.” It took an average 9.9 years for the FICs initially rated “D” to become financially impaired.

A weak financial status and the frequency of more extreme weather has contributed to increased impairments in the U.S. P/C industry.

In 2022, Hurricane Ian, a Category 4 hurricane that caused significant damage to the southeast, was the costliest US natural catastrophe event. In addition, Winter Storm Elliott also caused sizeable losses.

The analysis found that among the 19 weather-related impairments, including both AM Best-rated and non-AM Best-rated companies, only two became impaired in 2012 and 2013; the rest became impaired in the past six years.

Fourteen companies became impaired in the past 28 months, mainly due to Hurricane Matthew in 2016; Hurricanes Harvey, Irma, and Maria in 2017; Hurricane Michael in 2018; Hurricanes Laura, Sally, Delta, and Zeta in 2020; and Hurricane Ida in 2021.

Of the 5,323 companies that had an AM Best rated during the 1977-2022 period, 752 became financially impaired.

The rate of increase in impairment rates is most significant in the early years. In addition, the impairment of a large group can affect annual impairment counts significantly.

As ratings decline, the percentage of companies maintaining the same rating over a one-year period also declines, according to AM Best’s analysis. As an example, 87.1 percent of the companies with an “A-” rating were still rated “A-” one year later, but only 77.9 percent of companies with a “B++” rating were still rated “B++” one year later.

Since December 31, 1977, 516 impaired insurers were included in the net impairment pool, as opposed to 752 impaired insurance carriers in the gross impairment pool.

AM Best designates an insurer as a financially impaired company (FIC) upon the public placement

of the company, via public court order or other international equivalent, into conservation, rehabilitation or insolvent liquidation

Florida Saw Biggest Auto Premium Decline: Report

Florida Saw Biggest Auto Premium Decline: Report  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?