Property cat reinsurance: “More.”

Professional liability insurance: Not so much.

The president and chief executive officer of W.R. Berkley Corp., Robert Berkley, Jr., shared his company’s appetite for short-tail and long-tail coverages during an earnings conference call on Monday—flagging property catastrophe reinsurance as an area it’s leaning into, and D&O as an area where its easing up.

The decision to seize an opportunity in property-cat reinsurance is a big deal at W.R. Berkley, given the fact that this is an activity that takes place only about two in 15 years at the specialty insurance and reinsurance company, according to Berkley’s estimation.

“In 2002 [or 2003], we did enter into what I would define as some short term quota shares with a couple of facilities in London. And we wrote a fair amount of business for a very defined period of time,” Berkley said, recalling one of those rare occurrences. “It proved to be very lucrative for the shareholders. And shortly thereafter, as it became a less attractive market, we faded into the background,” he said.

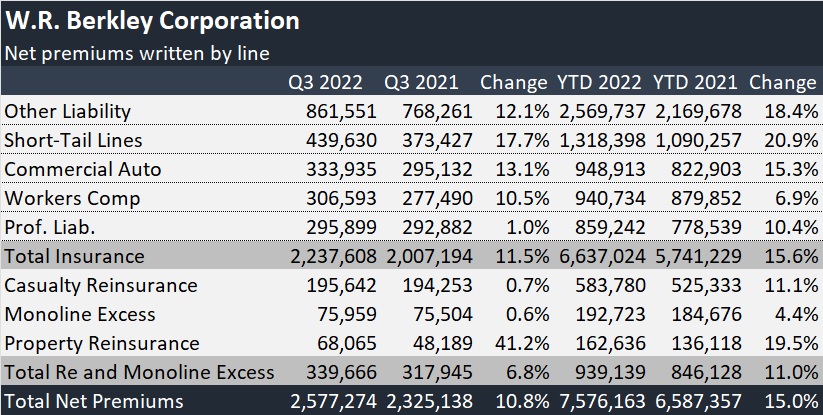

Overall, gross premiums grew to a quarterly record level of $3.1 billion, with net premiums up similarly to $2.6 billion. A by-line breakdown of changes in net premium written gives a clear indication of the company’s view of where there are market opportunities.

“If we are growing at a healthy rate, it means that we think there’s margin there and we are leaning into it. When you look at the various product lines, certainly short tail lines, in particular property as of late, is demonstrating more opportunity.”

“In addition to that, when you look at the reinsurance space, we are seeing a similar opportunity and it’s likely you’ll see us leaning into that even more.”

“On the other hand, you have professional liability, with particularly public D&O standing out as a product line that has become increasingly competitive,” he said.

The line-by-line premium chart reveals professional liability premiums growing only 1 percent, and casualty reinsurance growing by an even smaller percentage, while property reinsurance premiums jumped 41 percent, while still remaining a small portion—less than 3 percent— of the overall book of business.

Reiterating a message that he delivered on past calls about the workers comp line, Berkley said, “We’ve been surprised by the level of competition,” clarifying that the double-digit growth figure shown in the Berkley table is a function of payroll growth.

Applauding the discipline of the company’s professional liability underwriters, Berkley explained that a second factor lowering premium growth for those lines is slowing demand—as IPO and SPAC activity cools down.

“At some point, I expect that plus 1 [percent growth for professional liability] is going to turn into a negative number. And that’s OK. We take one day at a time,” he said. “It’s still a cyclical market, and… people are becoming more competitive. We accept that reality,” he said, noting that while the company was growing D&O business at a very rapid pace at this time last year, Berkley’s underwriting discipline is evident in this quarter’s low growth figure.

Even Retro Could Be In Appetite

Commenting on overall market conditions, Berkley said that “the specialty space, and in particular, the E&S space remains very attractive. [But] if it is a piece of business that falls within the appetite of the standard market, particularly a national carrier and some regional carriers, it is shocking to us how competitive some participants are willing to be.”

Responding to a question about how much property reinsurance business the company has its sights on for Jan. 1, 2023, Berkley said only, “More.”

“For an extended period of time…, the reinsurance marketplace has kind of gotten led around by the nose by the insurance marketplace. And there’s enough pain out there that has been building for an extended period of time. It would appear as though that the reinsurance marketplace maybe has gotten the courage and the discipline that has been a long time coming”

W. Robert Berkley, Jr.

Explaining why the market is ripe for this action now, Berkley gave his perspective on recent history and the current market. “For an extended period of time…, the reinsurance marketplace has kind of gotten led around by the nose by the insurance marketplace. And there’s enough pain out there that has been building for an extended period of time. It would appear as though that the reinsurance marketplace maybe has gotten the courage and the discipline that has been a long time coming.”

The executive said , “We have been making plans and positioning ourselves as you would expect, … to be able to participate in a meaningful way” in the property-cat reinsurance market if pricing rises to what the company views as adequate rate levels.

“But we’re only going to do that if we think you are getting paid enough. We are not in that product line day in and day out, riding the cycle up and down. We are going to participate, call it on average, when we think everything lines up—the planets and stars line up for, call it two years out of every 15 years. And it is certainly very possible that 2023 could be one of those two years,” he said.

“But if we don’t like it, if it doesn’t get hard enough, we’re not going to stick our toe in the water, let alone a foot.”

Still Berkley wouldn’t be coaxed by analysts who repeatedly asked him to quantify what a “meaningful” participation might be. “When the day’s all done, we have a fair amount of headroom to the extent we see the opportunity presenting itself,” he offered, suggesting a sliding scale participation shifting with healthy levels of anticipated risk adjusted returns.

“Do I think that we are going to become a leading property cat underwriter overnight? No, I do not. At the same time, do I think it could become a more meaningful part of what we do in the short run? Yes, I do but that doesn’t mean that it’s going to become more than half of what we do,” he said, also forecasting that the change in W.R. Berkley’s property reinsurance premiums “would be noticeable relative to its size today and its contribution today.”

While it’s too early to decide exactly the extent of Berkley’s participation, “we do have the colleagues and the expertise all lined up, the distribution knows that we are here, that we want to see what’s out there and we will participate again to the extent that it makes sense,” he said, at one point, suggesting that “even certain types of retro [retrocessional cover] are things that we are paying close attention to… potentially as a meaningful seller.”

He stressed repeatedly that the company’s participation is dependent on the margin that it sees in property cat business. “Typically, the vast majority of the time during a cycle, we do not believe the margin is there, which is why we control it very tightly.”

Reserves and Ian

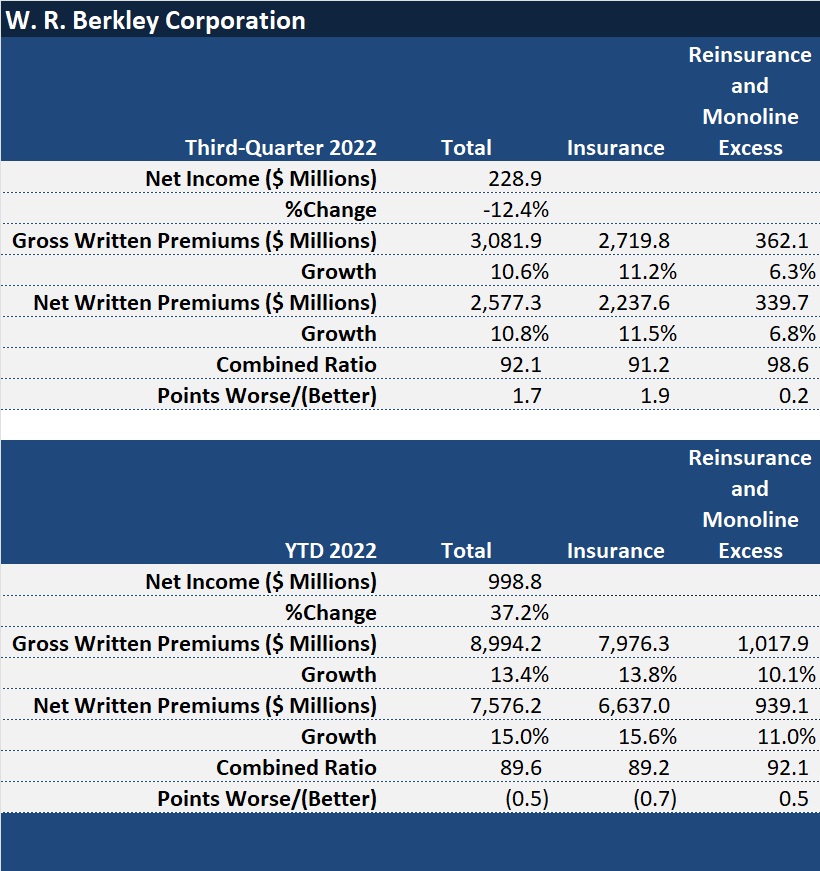

During the quarter, W.R Berkley’s net income declined 12 percent to $228.9 million. For the first nine months, income rose 37 percent to just under $1 billion.

The third-quarter combined ratio deteriorated 1.7 points, with prior-year loss reserves developing unfavorably by 1.6 loss ratio points in the current quarter, according to Chief Financial Officer Rich Baio.

Because a $30 million-plus reserve charge is unusual for the company, the CEO addressed several questions from analysts about it, describing it as being “entirely related to two…isolated and unique events stemming from COVID.”

“To the best of our knowledge and as clearly as we can see it, we do not envision this being an ongoing issue,” Berkley said.

Baio also reported that pretax catastrophe losses were $94 million in the quarter, representing 3.9 loss ratio points, compared with $74 million, or 3.5 loss ratio points in last year’s third quarter. He said the main driver of cat losses in the quarter was Hurricane Ian, but didn’t give a figure for Ian losses alone.

One analyst asked Berkley to share his view of overall industry loss estimates for Hurricane Ian, noting that two schools of thought are emerging—one saying they’re too high, and the other too low. Berkley said the range is probably fair, but not the allocation of losses to line of business that models are suggesting.

“It’s not that we take any particular great issue with the numbers—that $50 to $70 [billion]. As bookends, that’s probably not a bad range,” he said, putting his best own guess “toward the lower end.”

“This is going to prove to be a very, very significant flood issue, which obviously will impact the loss for many on the homeowner’s side….I think the auto loss is likely to prove to be far more severe than maybe the models would’ve initially suggested,” he said.

Mapfre Acquiring Tuio Stake; Bolsters Commitment to AI, Digital Innovation

Mapfre Acquiring Tuio Stake; Bolsters Commitment to AI, Digital Innovation  Fitch Warns AI Market Correction Emerging as Major Global Credit Risk

Fitch Warns AI Market Correction Emerging as Major Global Credit Risk  Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?  Workplaces Dialing Down ‘Tokenmaxxing’ as Focus Returns to ROI

Workplaces Dialing Down ‘Tokenmaxxing’ as Focus Returns to ROI