During a quarterly earnings call, the leader of RenaissanceRe discussed drivers of company’s third straight double-digit operating ROE result, its resilience to inflation and recession risk, and also gave an assessment of vendor catastrophe models.

“Our scientists and engineers at RenRe Risk Sciences believe that the commercially available models do not properly reflect climate change as an evolving phenomenon,” said Kevin O’Donnell, president and chief executive officer.

“For some perils, while vendors may have adjusted their views to reflect recent experience, we believe that they have not robustly captured the physics of climate change.”

“From a risk management perspective, this means that the vendor model outputs are likely to underestimate the risk that insurers and reinsurers are managing. This could cause companies to expose more capital than intended, and their returns for managing cat risk will be lower than expected.” “Consequently, investors may question whether the entire insurance industry truly understands the potential impact of climate risk, whether it is being correctly incorporated in the industry’s evaluation of risk and most critically, whether it is appropriately reflected in rates.”

O’Donnell delivered the remarks after summing up the impacts of inflation and recession on RenRe, and the industry generally—offering a description the midyear market dynamics that the shrunk the supply of property-catastrophe reinsurance along the way. In short, investor nervousness about property-cat business is partly attributable to recurring model miss, he suggested.

First, addressing the impacts of inflation, he said that RenRe has materially increased rates to compensate rising loss cost impacts, and noted the positive impacts of inflation-driven interest rate increases on investment portfolios will likely “persist longer than elevated inflation.”

Turning to growing fears about recession, O’Donnell first noted the limited amount of discretion that policyholders have in buying coverage—most must purchase homeowners and many commercial coverages. “By extension, most insurance carriers require reinsurance to maintain their portfolios,” he said, noting that recession also decreases risk tolerances. “So demand for volatility protection goes up,” he said.

Recession and inflation together reduce the supply of capital while increasing its costs, he added. “Consequently, reinsurance rates typically rise while simultaneously becoming more competitive versus other forms of risk capital” in that economic scenario.

“As a result of these supply-demand dynamics, over the course of the next year, we expect increasing demand for our products,” he said referring to both property-cat and RenRe’s casualty and specialty business. “In addition, rates should continue to face upward pressure—in some cases materially,” he said, reporting that similar dynamics already played out during midyear renewals, “with property cat demand increasing by about $5 billion against constrained supply, leading to substantially higher rates.”

“The constrained supply of reinsurance is being driven by investor concerns over reinsurance generally as a class, and property-cat specifically,” he asserted.

Later, specifically calling out what he said is “one of the major factors behind the market’s perception of property-cat risk,” O’Donnell pointed to the “the poor historic performance of cat models.”

“In no small part, this is due to an overreliance on vendor models that inadequately capture the growing influence of climate change,” he said.

O’Donnell discussed RenRe’s investments in considerable modeling resources, noting that the RenRe Risk Sciences team ensures that its proprietary models reflect the “most up to date data-informed science,” making them better predictors of the impact of climate change on loss costs.

“We have deep roots as a writer of property-catastrophe reinsurance, and remain committed to this risk as a core component of our underwriting strategy,” he said. “This is due to our competitive advantage in understanding property-cat risk and our conviction that we will be paid for the volatility over time.”

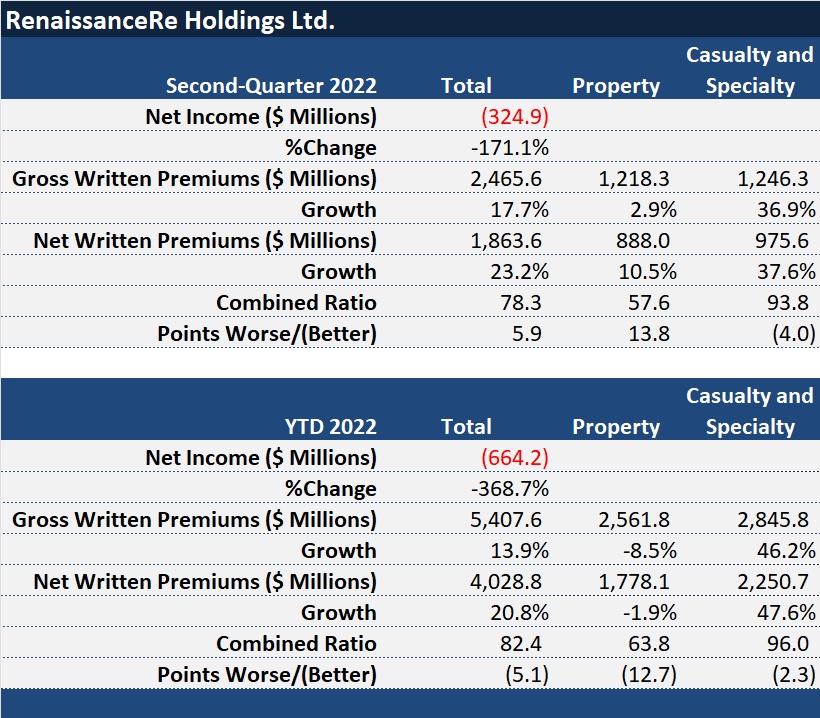

Results Snapshot

While RenRe’s gross premiums for property grew just 2.9 percent in the second quarter, and 10.5 percent on a net basis, the real growth story for the quarter was in casualty and specialty, where both gross and net premiums jumped nearly 40 percent.

Within the specialty book, O’Donnell spoke about opportunities to grow RenRe’s cyber and mortgage portfolios, while maintaining an overall casualty and specialty combined ratio in the mid-90s.

In dollars, underwriting profit for casualty and specialty amounted to $52 million in the quarter.

In the property book, O’Donnell noted that RenRe has been reducing its exposure to Florida over the last five years, continuing at midyear with the reinsurer currently only providing material support to six Florida domestic insurers.

RenRe still has exposure to Florida hurricane risk, however, through regional and nationwide property-cat programs and through RenRe’s other property book, he noted.

Overall, property turned in a $264 million underwriting profit for the quarter, posting a 57.6 combined ratio.

Net investment income of $107.2 million and fee income of $30.7 million were additional drivers of profit.

Still, RenRe recorded a bottom line net loss of nearly $325 million for the quarter, with $654 million of net realized and unrealized losses on investments driving the decline.

Without the impact of investment losses, operating income was $238 million, translating to an annualized operating return on average equity of 18.4 percent.

Most American Workers Are Checked Out, and Like ‘The Office,’ Their Bosses Are the Last to Know

Most American Workers Are Checked Out, and Like ‘The Office,’ Their Bosses Are the Last to Know  How We Did It: How a 150-Year-Old Mutual Transformed Culture to Drive AI

How We Did It: How a 150-Year-Old Mutual Transformed Culture to Drive AI  East Coast Cities More Dangerous for Drivers According to New Allstate Report

East Coast Cities More Dangerous for Drivers According to New Allstate Report  Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?

Ranking: Who Are the Insurance Industry’s AI Talent, Maturity Leaders?