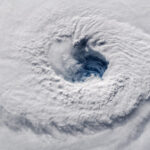

Climate change is making hurricanes bigger and stronger, and it may soon push them farther north. Yet Canada’s homeowners, businesses and insurers underestimate that escalating risk, according to one of the world’s leading reinsurance firms.

Overall, the northern nation has proved to be among the world’s most climate-resilient countries, having so far escaped the worst effects of the natural weather disasters whipped up by global warming, according to a report by Swiss Re AG. That has included hurricanes. Although they’ve become increasingly ferocious, they often dissipate before reaching Canada.

But as ocean surfaces warm, the frequency, duration and intensity of storms increase. That’s extending their range and making Canada, where just one or two tropical cyclones make landfall each year, more vulnerable, according to the Zurich-based company, which provides reinsurance to 15% of the country’s insurance industry.

“You have an increased likelihood of hurricanes making landfall further north and eventually making landfalls at higher latitudes than what we’ve ever seen before,” Monica Ningen, head of Swiss RE Canada, said in an interview.

The U.S. National Oceanic and Atmospheric Administration is predicting another overactive hurricane season this year, though not as bad as last year, when named storms caused more than 400 deaths and $40 billion in damage and losses in North America.Like many countries, Canada has a “protection gap” regarding hurricanes, Ningen said. Since 2003, more than a third of such storm-related losses weren’t covered by insurance. If the storms worsen in Canada, so will the gap.

Although homeowners in the Atlantic provinces currently pay about C$1 billion ($826 million) a year in insurance premiums, covering all types of disasters, “any major hurricane hitting that region could be multiples of that,” she said.

Swiss Re is particularly concerned that many insurers have stopped paying attention to Atlantic Multidecadal Oscillation (AMO), a phenomenon in which ocean temperatures fluctuate as much as 4 degrees Celsius (7.2 degrees Fahrenheit) every 25 to 40 years. These changes have a major impact on the frequency of hurricanes in the Atlantic, and the current warm phase isn’t expected to end any time soon, Ningen said.

Climate Resilience

Canada ranks fifth in climate-change resiliency among 48 countries studied in the Swiss Re report. If global temperatures stay on their current trajectory and rise more than 2 degrees Celsius (3.6 degrees Fahrenheit) by 2050, that could shave 14 percentage points from the world’s GDP, according to the study. The economic impact on Canada, by contrast, would probably be half as bad.

Still, Jerome Haegeli, chief economist at Swiss Re, warned that those costs “are likely nonlinear, meaning inaction today will have more costs in the future.”

Swiss Re Net Income Weighed Down by Pandemic, Texas Freeze

Canada has so far gotten off lightly when it comes to hurricane damage. A record 30 named storms formed over the Atlantic last year. Eleven made landfall in the U.S. but only one — Teddy — came ashore in Canada as a much weaker post-tropical cyclone.

On Thursday, the Canadian Hurricane Center said that despite forecasts of more Atlantic storms for this year, the number expected to reach Canada is likely to be unchanged.

The last official hurricane-size storm to hit Canada was Igor in 2010. The most destructive was Juan in 2003, which caused more than C$300 million in damage and C$91 million in insured losses in central Nova Scotia and Prince Edward Island.

Expensive Claims

To appreciate what may lie ahead for Canada if Swiss Re’s worries prove justified, it helps to understand just how expensive hurricanes can be.

Hurricane Andrew caused $15.5 billion in insured losses when it barreled through Florida in 1992, rendering a dozen insurance companies insolvent. Had the same storm struck 25 years later, insured losses would have been $50 billion to $60 billion because of increased development and population growth in the region, Swiss Re estimates.

By comparison, Canada’s most expensive natural disaster to date was the 2016 Fort McMurray wildfire that resulted in about $3.6 billion in insured losses.

Hurricane Dorian, one of the most powerful Atlantic storms in history, roared through the Bahamas as a Category 5 storm in 2019, but had weakened to Category 1 by the time it hit Canada, resulting in just C$186 million in damage in the country.

“You only get so many close calls before our luck is going to run out,” Ningen said.

A 2021 report by the Property and Casualty Insurance Compensation Corp., that examined the Canadian insurance sector’s financial “tipping point” found that a disaster causing more than C$35 billion in claims would result in a systemic failure of the sector.

Even with the greater frequency of hurricanes, that doomsday scenario is far more likely to result from a major earthquake in Vancouver or the Montreal-Ottawa corridor, said PACICC Chief Executive Officer Alister Campbell. Canadian insurers have been loading up on reinsurance — insurance for insurers — by 71% in the last eight years, to about C$29.5 billion, largely to protect themselves against a catastrophic quake. That insurance also covers other natural disasters, including storms.

For that reason, Campbell says the industry is well-protected. “It is very hard to see a storm causing failure in Canada,” Campbell said, because “it is very hard to imagine any insurer being exposed to storm loss as great as their quake loss would be.”

Preparing for the worst doesn’t come cheap, especially at a time when homeowners ought to be trying to exceed minimum building standards, yet material costs are skyrocketing, Ningen said. The biggest risk may be that adequate protection becomes too expensive for many individuals and businesses.

“That is the biggest challenge,” she said. “We need to adapt before the risks get unaffordable.”

–With assistance from Brian K. Sullivan.

Supply Chain Insurance Is ‘Must-Have’ Cover During Geopolitical Tensions: GlobalData

Supply Chain Insurance Is ‘Must-Have’ Cover During Geopolitical Tensions: GlobalData  A Matter of Trust

A Matter of Trust  Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty

Liberty Mutual Introduces Its Newest Brand Character: Liberty Biberty  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t