When insurance coverage lawsuits brought by businesses seeking coverage for COVID-related interruptions surpassed the 700 mark last week, the natural question to ask was: Is that a lot?

That’s exactly the question that Chris Cheatham, the CEO and co-founder of InsurTech RiskGenius, asked during a webinar he hosted last week, addressing the question to Tom Baker, the William Maul Measey Professor at the University of Pennsylvania, who presented the figure.

Baker, an expert in insurance law and policy, showed an analysis of the numbers of business interruption coverage suits following past catastrophe events between 2009 and 2020—in particular, Hurricanes Ike, Irma and Harvey and Superstorm Sandy and COVID-19. Comparing the current level of COVID-19 cases in federal courts to the business interruption coverage suits filed after those natural catastrophes, he observed, “They exceed the norm by two or three times all the nat cats.”

“It’s a big deal,” he said, displaying line graphs with case spikes that rose to less than 100 for Hurricane Ike a year after the third-quarter 2008 event, and to roughly 150 a year later. For Sandy, Irma and Harvey, case filings were less than 100n similar time frames.

The University of Pennsylvania has been tracking insurance coverage litigation on a COVID Coverage Litigation Tracker (CCLT) powered by Lex Machina, machine learning-focused legal analytics software that harvests information from PACER, the federal docket system. A webinar slide based on recent CCLT output indicated a figure of 694 total COVID-19 business interruption insurance coverage lawsuits, but Baker said that he had seen a list of 69 new cases on the day of the webinar—July 21. While that number likely had some duplicates (owing to an overly inclusive search he uses to tap the Lex Machina tool), Baker confidently projected that the BI cases had eclipsed 700 at that point—more than Ike, Sandy, Irma and Harvey together.

Although Baker could not specifically respond to a question from Cheatham about how the COVID BI case numbers compare with those brought in the wake of Hurricane Katrina (because Lex Machina only goes back to 2009), he speculated that while the Katrina-driven suit numbers would be bigger than those for the other storms, “it wouldn’t be anything like COVID-19.”

“And it’s not slowing down,” Baker added, referring to the continual trend in COVID BI coverage suit filings.

Cheatham, who has been using the University of Pennsylvania tracker to put together analyses of his own, agreed with the assessment. “It’s almost five-times,” he said, comparing the COVID case counts to those following each of the storms individually. Providing one obvious reason for the disparity, Cheatham noted that while a hurricane hits just one area—a single state or multiple states—COVID-19 shut down almost everything for a period of time. “That was a countrywide shutdown essentially, except for some remote locations, where businesses just across the board were shut down,” Cheatham said, turning to Baker to supply other reasons that COVID is a much bigger BI event in terms of the claims being filed than the storms.

Baker offered that the nature of the coverage disputes is different. For hurricanes, coverage disputes centered around questions like what share of the loss the insurance company should pick up vs. the federal flood program. “And then also, what was the value of the damage?” In contrast, “for COVID-19, the insurance industry has decided that it’s just not paying absent an affirmative coverage [grant] in the policy.” He added: “I think things move to litigation faster and also with a greater propensity because there’s not that belief that, ‘Hey, we can come to some agreement.’ When the answer is, ‘No, your claim is denied,’ the next step is litigation.”

Why Pennsylvania Filings Are Higher Than New York

Cheatham and Bryan Wilson, MIT Fellow, have been working on their own analysis of trends in COVID litigation for a series of articles Cheatham is authoring exclusively for Carrier Management, titled “COVIDigation Nation.” In the accompanying article, “COVIDigation: Why So Many Cases? Are More Coming?“—the first of the series—he uses Penn Law’s COVID Coverage Litigation Tracker to conclude that 69 percent of COVID insurance coverage lawsuits have been filed in just nine states. While big states known for high litigation rates generally are among them, like California and Illinois, Cheatham’s analysis shows another factor is the correlation between COVID infection rates and the number of insurance coverage lawsuits filed.

Still, there are a few questions that Cheatham needed Baker’s help to answer—like why Pennsylvania, registering 10.5 percent of the coverage lawsuits as of mid-July, and Florida, with 8.3 percent, were outpacing New York’s 7.0 percent?

Part of the reason is that New York isn’t viewed as a particularly policyholder-friendly jurisdiction, Baker said, explaining a slower pace of filings in the Empire state. Beyond that, he said that plaintiffs firms actively seeking to consolidate cases in other states may explain some of the other outliers.

“There is an effort right now in the federal courts to have what is called an MDL, which is multidistrict litigation—a procedure in the federal courts that’s very widely used in products liability cases but has, to my knowledge, never been used before in insurance cases,” Baker said. He explained that what an MDL does is that it transfers all of the cases of a particular category to one federal court for proceedings leading up to but not including trial. (The cases go back to the court where they originated for the trial.)

“There are three teams of lawyers who have filed three competing efforts to consolidate these cases in Pennsylvania, Florida and Illinois,” Baker said, noting that the three cohorts have adopted different strategies. “The Pennsylvania lawyers’ strategy has been, ‘Hey, we’re going to file the most cases and this case should be consolidated in the Eastern District of Pennsylvania because that’s the center of gravity from cases.'” While Florida lawyers are using a similar strategy, a high-powered coverage lawyer on the Illinois team of higher-profile national lawyers is simply relying on their reputations rather than flooding the dockets. “The strategy that they’re taking is, ‘Listen, we’re just really amazing lawyers and you should do it in Chicago’—and Chicago is in the middle of the country,” Baker said.

(Editor’s Note: The judicial MDL panel was scheduled to hear arguments on a request to transfer and consolidate federal court business interruption coverage suits related to the COVID-19 pandemic on Thursday, July 30.)

Years Not Months

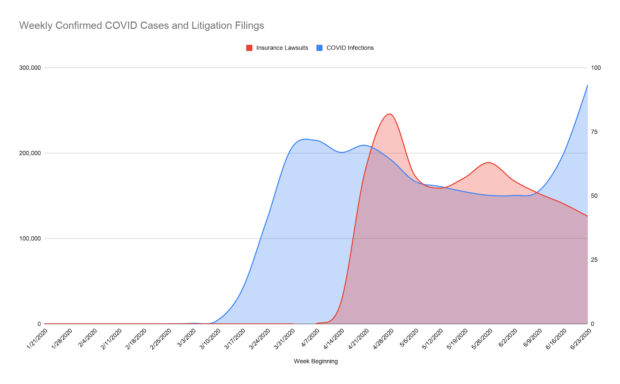

In his COVIDigation analysis, Cheatham also tracks the timing of case filings, finding a roughly one-month lag between spikes in COVID infections and new high watermarks for litigation filings. Viewing a jump in infections during the week of June 23 based on the New York Times COVID-19 dataset, Cheatham suggested there could be a surge in insurance litigation near the end of July. (See related article by Cheatham, “COVIDigation: Why So Many Cases? Are More Coming?“)

Baker, going back to his analysis of hurricane landfalls and BI coverage litigation, suggests an even longer loss development tail for insurers to worry about. “The peak doesn’t come until one year” out, Baker said, pointing to a bar graph showing case counts at intervals of six months, one to two years, two to three years and over three years out for the storm events. While most showed case spikes in the one-to-two-year bucket, for Ike, the spike came in two to three years, and there were still Sandy BI lawsuits being filed after three years. “To the extent that COVID-19 cases follow that pattern, which it’s too soon to tell because we’re not even six months out really, then that suggests that there’s a lot more lawsuits to come,” Baker concluded.

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums

Why Multifamily Owners’ Safety Investments Aren’t Showing Up in Their Premiums  The Car Remembers What Happened; Human Beings Can’t

The Car Remembers What Happened; Human Beings Can’t