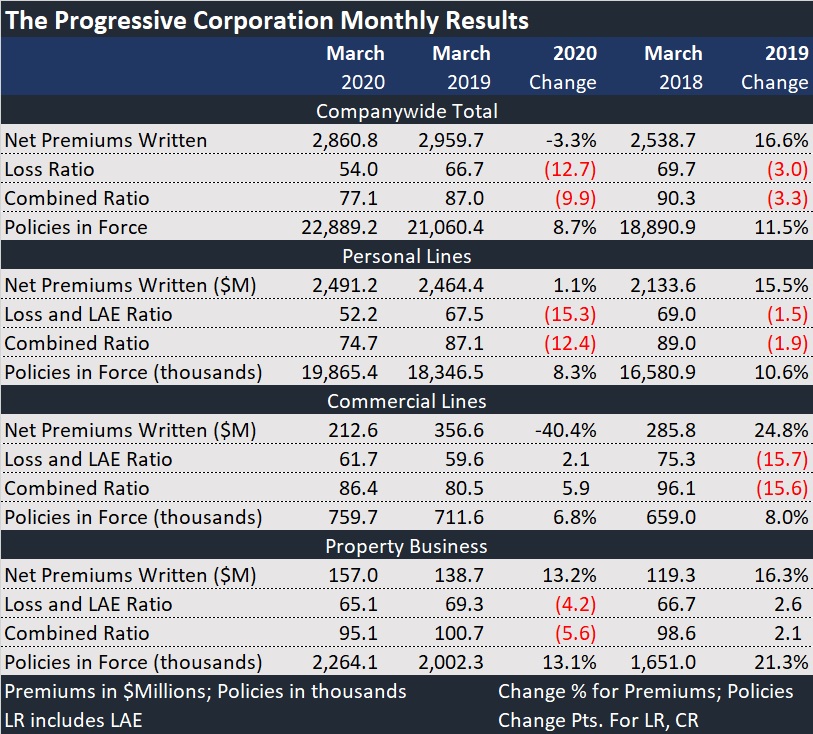

Progressive Corporation released a monthly earnings report for March 2020 yesterday, providing some early signs of the premium and loss ratio impacts of COVID-19 shelter-at-home restrictions for property/casualty insurers.

The numbers show premium drops occurring in advance of customer discounts that will be credited to personal auto customers in March, as new personal auto policy applications plummeted, as did commercial vehicle premiums for transportation networking company businesses that are directly related to miles driven.

The March numbers also reveal a loss reserve boost of $103 million recorded “to reflect the impact that COVID-19 restrictions had on…estimates of ultimate costs to settle claims,” according to a footnote of the report. In spite of the reserve increase, Progressive’s March calendar-year loss ratio dropped almost 13 points to 54.0 from 66.7 in March 2019.

Overall, Progressive reported a 3 percent drop in net premiums to $2.9 billion. While personal lines premiums rose 1 percent to $2.5 billion, the jump is significantly lower than the 16 percent increase in premiums that Progressive reported in March 2019.

Explaining how COVID-19 restrictions impacted the premium figures in a commentary released with the numbers, Progressive noted that new applications for the last three weeks of March—after social distancing rules and shelter-at-home restrictions went in effect—fell 23 percent compared to the same three-week period last year. In contrast, during the first week of March, new applications were up over 2 percent—prior to the restrictions. Still, policies in force were 8.3 percent higher at the end of March 2020 than they were at month-end March 2019 and down only slightly from the end of February 2020 as increases in renewal applications offset decreases in new business applications, Progressive said.

Separately, last week, Progressive announced that personal auto customers with policies in force on April 30 will be credited 20 percent of their April premiums in May, and that those with a policy in force as of May 31 will be credited 20 percent of their May premiums in June, with the two credits amounting to roughly a $1 billion giveback. Neither of the actions impacted the March numbers.

Commercial lines premiums for March 2020 were $144 million lower than for March 2019, representing a 40 percent drop. According to a footnote to the report, net premiums in the commercial lines transportation network company businesses were reduced by $110.5 million, reflecting a decline in miles actually driven during the month “and a revised estimate of the miles to be driven” for the rest of the policy term, “which is the basis for determining the premiums written” on these policies.

Across all lines (including property), the companywide loss and loss adjustment expense ratio of 54.0 for March 2020 was 16.3 points lower than the ratio reported on a year-to-date basis through February 2020 (70.3). Progressive attributed the drop to lower auto accident frequency experienced as a result of the COVID-19 restrictions but said the impact was partially offset by the $103 million reserve boost.

Separately, Andy Cohen, the chief operating officer of Snapsheet, an InsurTech that provides virtual claims management processing technology, gave a wider perspective than a single company’s results, telling Claims Journal (CM‘s sister publication) that March auto claim counts may be the lowest in 50 years for P/C insurers. His firm is seeing 40-50 percent drops in claims volume for personal auto and a 30-40 percent reduction for commercial auto.

At Progressive, across all lines, the companywide combined ratio was 77.1 for March, roughly 10 points lower than March 2019. The company noted that an allowance for doubtful accounts added 2.4 points to the expense ratio. The allowance was added after an evaluation of premiums receivable, the company said, noting the potential impacts of billing leniencies put in place during the month and a program to not cancel or non-renew due to non-payment.

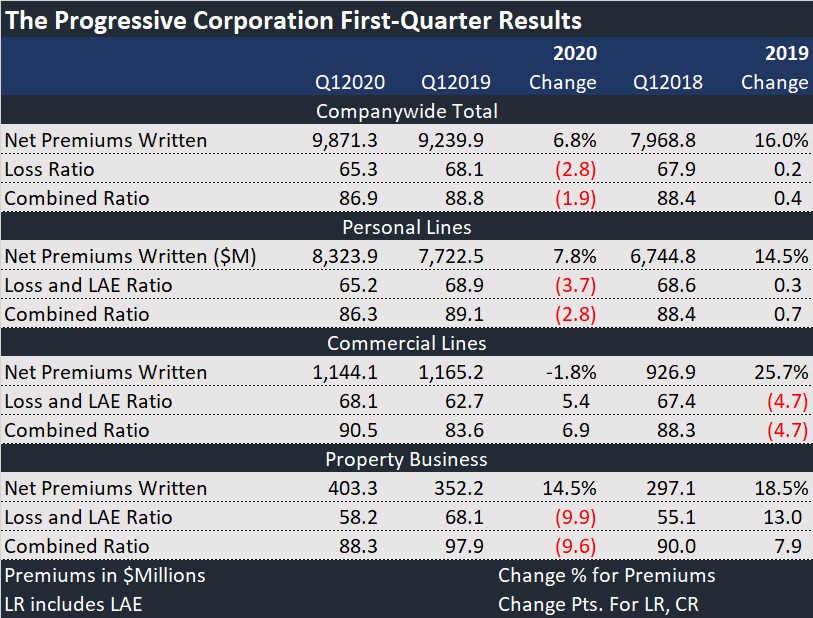

Progressive also reported first-quarter results, showing premium growth of 7 percent overall and a combined ratio of 87, roughly two points better than first-quarter 2019.

Design the Team Before You Design the Solution: Commercial Trucking Case Study

Design the Team Before You Design the Solution: Commercial Trucking Case Study  Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?

Are We Measuring the Value of Claims AI or Simply Measuring Its Activity?  Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz

Another M&A Deal: AXIS Acquiring DUAL NA XS Liability Biz  The Hartford To Acquire Equitable’s Employee Benefits Biz

The Hartford To Acquire Equitable’s Employee Benefits Biz